Economist Intelligence Unit global forecast – Global growth braced for impact

Since the start of 2018 trade policy has become the biggest risk to The Economist Intelligence Unit’s central forecast for global economic growth. The US president, Donald Trump, is shifting his country’s previous qualified support for free trade in a protectionist direction. Trade tensions escalated when the US government threatened China with tariffs on imports worth about US$50 billion a year in April. China responded with its own equivalent list. Discussions between the two countries have thus far failed to solve the dispute. The third round of negotiations on June 2nd‑3rd revealed the divisions in the US trade team, with conflicting messages on the team’s priority—China’s approach to intellectual property and technology transfer or the reduction of the US’s trade deficit with China. On June 15th the US confirmed that US$34 billion‑worth of China’s goods would be subject to additional tariffs of 25%, with the possibility that another US$16 billion‑worth of goods would also be targeted after an extended period of public comment. China responded in kind. On their own, these tariffs are unlikely to be sufficient to trigger a major slowdown in growth. However, we note the risk of neither the US nor China achieving their aims through this round of tariffs and the possibility of the dispute escalating to further rounds of non-tariff barriers of the sort that harm business confidence, investment decisions, diplomatic ties and, ultimately, the performance of the global economy.

Furthermore, on trade, the Trump administration continues to challenge the multilateral system. Initially, when the US announced import tariffs on steel and aluminium in March, Canada, Mexico and the EU were given temporary exemptions. The exemptions were removed by the Trump administration on June 1st, sparking a round of retaliatory tariffs from these traditional US allies. Reaffirming his intentions, Mr Trump deepened divisions in the G7 on June 8th‑9th when he failed to agree to the joint communique in support of a rules-based trading system. Following the withdrawals from the Paris climate accord, the Iran nuclear deal and the Trans-Pacific Partnership, the outcome of the G7 meeting and related trade tensions with key US allies again demonstrate that Mr Trump’s “America First” policies do not align with a multilateral system of global governance.

Some emerging markets are susceptible to higher US interest rates

Emerging markets will also come under some pressure from higher US interest rates and the strength that these provide to the dollar. For example, since April Turkey, Brazil and Argentina have experienced sharp currency depreciation. As global interest rates gradually rise from ultra-low levels, investors are becoming less forgiving of countries with financial, macroeconomic or political vulnerabilities. Turkey is illustrative here, given its structural current-account deficit, necessitating large external financing needs, and the high levels of foreign-currency denominated debt held by the private sector—steep policy rate increases by the central bank were required to stem capital outflows. For its part, the Federal Reserve (Fed, the US central bank) has helped to minimize the disruption by outlining how it will reduce the value of its balance sheet and over what time period. Despite this, we expect further short-lived periods of volatility as global markets adjust to the gradual shift away from easy money. In this environment, we expect the number of countries seeing their currencies come under pressure to rise over the next two years.

Geopolitical risks foreshadow greater volatility

We also note the economic risks posed by the complex and deepening tensions in the Middle East. Various proxy conflicts between Iran and Saudi Arabia have the potential to further destabilize the region. Mr. Trump’s decision to withdraw the country from the Iran nuclear deal is another signal that the US is inclined to offer stronger support to its traditional allies in the region, Israel and Saudi Arabia, in the coming years. We expect regional security in the Middle East to deteriorate following the US withdrawal. The move gives hardliners in Iran the upper hand over their moderate counterparts, which is likely to lead to a more confrontational foreign policy. Most worryingly, a proxy conflict between Israel and Iran in southern Syria has a significant chance of escalating.

Heightened geopolitical risk in the Middle East increases the likelihood of volatility in global energy markets. The re-balancing of the oil market pursued by OPEC over the past 18 months means that geopolitical developments now have a more pronounced effect on prices. News of the US’s withdrawal from the Iran deal sent prices above US$75/barrel for the first time since 2014. We expect prices to settle at around US$74/b, on the assumption that Iran’s oil exports fall by around 400,000 barrels/day (b/d), relative to its average sales of about 2.5m b/d in the period when the US remained within the nuclear deal. We expect oil prices to become more volatile over the next two years as geopolitical tensions rise.

The global economy will remain healthy, although vulnerable to shocks

Although the global economy is more vulnerable to shocks, our central forecast is that the underlying fundamentals are strong enough to maintain a healthy growth rate for 2018‑19. Global growth accelerated markedly in 2017 to 3%, its fastest rate since 2011, and we expect the same rate of growth in 2018‑19. The global economy will continue to follow the trends in the world’s two largest economies, China and the US. We expect the Chinese economy to start to slow at a steady rate. The government has a long-held target of doubling real GDP between 2010 and 2020. To achieve this, it requires annual average GDP growth of 6.3% in 2018‑20. We expect it to continue to stimulate the economy to reach this rate. After that, the leadership will have greater latitude to move away from GDP targeting. This is ideologically consistent with the call by the president, Xi Jinping, at the Chinese Communist Party’s national congress in late 2017, for more inclusive growth. It is likely, therefore, that the economy will be allowed to slow more quickly in the second half of the forecast period, with growth standing at 5.3% in 2022.

We continue to expect a business-cycle downturn in the US in 2020. Capacity constraints will emerge in the economy in the second half of 2019, pushing up inflation and forcing the Fed to signal a faster pace of interest-rate increases. This acceleration will be sufficient to trigger a short-lived decline in private consumption and investment in early 2020. Our core forecast is that the dip will be shallow and the rebound relatively rapid, owing to the Fed cutting interest rates aggressively in response. These movements in the world’s two largest economies mean that global growth will moderate to 2.3% in that year. As the US recovers, the global economy will receive some support in 2021‑22, enabling an acceleration to annual average growth of 2.8%.

Global monetary conditions will tighten

Among developed markets we expect falling unemployment and slowly building inflation to push central banks towards monetary tightening. In the US, the Fed, having first raised rates in December 2015 following the global financial crisis, will increase rates three times this year and four times in 2019. The European Central Bank, responding to the entrenched economic growth in the EU, is set to end the tapering of its quantitative easing (QE) programme in 2018. The Bank of Japan (the central bank) will also begin to wean itself off QE in 2019. By the second half of that year the shift to tighter monetary policy will begin to dampen private consumption growth in many developed markets, as borrowing will become more expensive. Consequently, the period between mid‑2017 and mid‑2018—where growth has been strong, inflation benign and monetary policy still loose—may feel like the sweetest spot for the global economy in the current business cycle.

As the global economy picks up, inflation is oddly quiescent –But central banks are beginning to raise interest rates anyway

Print edition | Finance and economics

Oct 4th 2018

A FEW years ago, the news about the euro-zone economy was uniformly bad to the point of tedium. These days, it is the humdrum diet of benign data that prompts a yawn. Figures this week show that GDP rose by 0.6% in the three months to the end of September (an annualized rate of 2.4%). The European Commission’s economic-sentiment index rose to its highest level in almost 17 years. Yet when the European Central Bank’s (ECB) governing council gathered on October 26th, it decided to keep interest rates unchanged, at close to zero, and to extend its bond-buying program (known as quantitative easing, or Quantitative Easing “QE”) for a further nine months.

The central bank said it would slow down the pace of bond purchases each month, to €30 billion ($35 billion) from January. But Mario Draghi, the bank’s boss, declined to set an end-date for QE. A hefty dose of easy money will be necessary, he argued, until inflation durably converges on the ECB’s target of just below 2%. It shows few signs of doing so, despite the economy’s strength. Underlying, or core, inflation, which excludes the volatile prices of food and energy, fell from 1.1% to 0.9% in October, according to data published a few days after the ECB meeting. The euro zone’s miseries of 2010-12 were unique. But in its present, happier state of vigorous activity, low inflation and easy monetary policy, it is like many other big economies (see chart).

After a decade of interest rates at record lows, those central banks that are inclined to tighten policy naturally attract attention. The Bank of England’s monetary-policy committee raised its benchmark interest rate from 0.25% to 0.5% on November 2nd, the first increase since 2007. On the same day, the Czech National Bank raised interest rates for the second time this year. The Federal Reserve kept interest rates unchanged this week, having raised them in March and June, but a further increase is expected in December.

In Turkey, perhaps the only big economy that is obviously overheating, the central bank—which has been browbeaten by the president, Recep Tayyip Erdogan, who believes high interest rates cause inflation—opted on October 26th to keep interest rates on hold. Yet in most biggish economies, underlying inflation is below target (see chart) and monetary policy is being relaxed. Brazil’s central bank cut interest rates on October 25th from 8.25% to 7.5%. Two days later, Russia’s central bank trimmed its main interest rate, to 8.25%. This week the Bank of Japan voted to keep rates unchanged and to continue buying assets at a pace of around ¥80 trillion ($700 billion) a year. These economies are gathering strength. It is a puzzle that, in such circumstances, global inflation is stubbornly low.

To figure out why, consider the model that modern central banks use to explain inflation. It has three elements: the price of imports; the public’s expectations; and capacity pressures (or “slack”) in the domestic economy. Start with imported inflation, which is determined by the balance of supply and demand in globally traded goods, such as commodities, as well as shifts in exchange rates. Commodity prices have picked up smartly from their nadir in early 2016. The oil price, which fell below $30 a barrel then, has risen above $60.

This has put upward pressure on headline inflation: in the euro zone it is 1.4%, half a percentage point higher than the core rate. Where inflation is noticeably high, it is generally in countries, such as Argentina (where it is 24%) or Egypt (32%), that have withdrawn costly price subsidies and whose currencies have fallen sharply in value, making imported goods dearer. In Britain, rising import prices linked to a weaker pound have added around 0.75 percentage points to inflation, which is 3%.

A second influence on inflation is the public’s expectations. Businesses will be more inclined to push up their prices and employees to bid for fatter pay packets if they believe inflation will rise. How these expectations are formed is not well understood. The measures that are available are broadly consistent with the central bank’s inflation target in most rich economies. Japan is something of an outlier. It has struggled to meet its 2% inflation target in large part because firms and employees have become conditioned to expect a lower rate of inflation. Japan’s prime minister, Shinzo Abe, recently called for companies to raise wages by 3% in next spring’s wage round to kick-start inflation.

Leave aside the transient effects of import prices, and inflation becomes a tug-of-war between expectations and a third big influence, the amount of slack in the economy. The unemployment rate, a measure of labour-market slack, is the most-used gauge. As the economy approaches full employment, the scarcity of workers ought to put upward pressure on wages, which companies then pass on in higher prices. On some measures, Japan’s labour market is as tight as it has been since the 1970s. America’s jobless rate, at 4.2%, is the lowest for over 16 years. Inflation has nevertheless been surprisingly weak.

In other words, the trade-off between unemployment and inflation, known as the Phillips curve, has become less steep. A paper last year by Olivier Blanchard, of the Peterson Institute for International Economics, found that a drop in the unemployment rate in America has less than a third as much power to raise inflation as it did in the mid-1970s.

The central banks that see a need for tighter monetary policy are worried about diminishing slack. There are tentative signs of stronger pay pressures in Britain and America, and firm evidence of them in the Czech Republic, where wage growth is above 7%. Even so, with inflation expectations so steady, the flatter Phillips curve suggests that the cost for central banks in higher inflation of delaying interest-rate rises is rather low. The ECB is quite a way from such considerations. The unemployment rate is falling quickly, but remains high, at 8.9%. There is still room for the euro-zone economy to grow quickly without stoking inflation. The dull routine of good news is likely to continue.

US-China spat could affect fast-growing trade in Asia, but it’s also an opportunity for some economies

- Trade within Asia has gone up. The region had the fastest trade volume growth in the world in 2017 for both exports and imports — 6.7 percent and 9.6 percent, respectively, the World Trade Organization said.

- However, the ongoing trade spat between the U.S. and China may soon have an impact on Asia, especially emerging markets, experts say.

- But it could also be a good thing for certain markets in Asia, as companies look for alternative supply sources beyond the U.S.

Published 12:35 AM ET Mon, 2 July 2018 CNBC.com

Belt and Road Initiative Quarterly: Q3 2018

In this edition of the Belt and Road Initiative (BRI) Quarterly, we highlight a number of projects, both planned and under construction, which are facing delay, suspension, cancellation or other challenges in BRI countries. Although Chinese policymakers will continue to promote economic and trade links under the BRI, against the backdrop of the US-China trade war, the initiative will continue to face international pressures—potentially feeding domestic push back, too.

In our previous BRI quarterly we noted that overseas direct investment (ODI) and merchandise trade links between China and the 65 countries we define as belonging to the BRI were stable in the first quarter of 2018. In the period since April 2018, however, several BRI projects have encountered challenges, ranging from delay and suspension to outright cancellation, due to skepticism and push back against the project, as well as changes of government in some countries. These developments have in turn raised questions within China over the economic and diplomatic feasibility of the BRI, which has been the subject of criticism in the past for its international largess at a time when China still faces developmental challenges of its own.

Trade, investment and lending

Merchandise trade along the BRI remained strong in the second quarter of 2018, growing by 17.3% year on year to US$319 billion, according to the Ministry of Commerce. However, this was down slightly from the 19.4% growth recorded in January-March. Within that figure, exports rose by 11.7% to US$183.3 billion, while imports rose by 25.9% to US$135.6 billion. China’s trade surplus with BRI countries increased to US$47.7 billion in April-June, accounting for 52.7% of China’s global trade surplus in that period.

China’s top ten BRI trade partners accounted for 66.7% and 53.4% of total two-way exports and imports respectively in the second quarter of the year. This illustrates the degree to which China’s trade connections remain underdeveloped under the initiative. In addition, exports to Malaysia and Turkey, two of China’s largest BRI trade partners, shrank in the second quarter in year-on-year terms, due to a significant slowdown in shipments of machinery exports and textile products, which may be tied to a stalling of BRI projects in Malaysia and the deteriorating economy of Turkey.

In addition, imports from Vietnam—another major Chinese trade partner within the BRI—deteriorated in the second quarter, owing to a slowdown in shipments of electrical equipment and components. Regional shipments of these types of intermediate goods will continue to face headwinds, due to supply chain disruptions caused by China’s trade conflict with the US.

Other indicators point to slowing Chinese business activity in BRI countries. Non-financial ODI flows to BRI countries grew by only 5.6% year on year to US$3.8 billion in April-June, slowing from 20% growth in January-March. This represented only 12% of China’s total non-financial ODI flows in the second quarter. Meanwhile, the value of newly signed construction contracts by Chinese firms in BRI countries contracted by 44.7% year on year in April-June, following a 7.3% decline in the first quarter.

China’s lending to BRI countries is not transparent, but balance-of-payments (BoP) data can shed some light. The most recent detailed figures show that China-resident entities provided overseas loans (defined in the BoP capital and financial account data as assets) worth US$54 billion in January-March 2018, marking the strongest quarterly disbursement on record. However, this came after a period of restrained overseas lending in 2017. The BoP measure is not restricted to BRI countries and covers a variety of commercial lending, including to overseas Chinese entities, but it can be seen as indicative of trend.

Policy updates

In the second quarter of 2018 the Chinese government released a number of policies to strengthen the regulatory framework around the BRI. In April 2018 several central-government agencies released guiding opinions aimed at standardizing funding sources, enhancing general risk-management and better guiding financing channels for Chinese overseas projects. In July China established two international courts to specifically handle disputes under the BRI framework, based in Shenzhen (for disputes on the BRI’s maritime “road”) and Xi’an (for disputes within the BRI’s overland “belt”).

Chinese policy banks that are backing the BRI, including the China Development Bank (CDB) and the Export-Import Bank of China (China EXIM), have become more active in co‑operating with international lenders. In July the policy banks announced plans to work with international financing institutions to improve financial governance and to manage debt and investment risk. A UK-based newspaper, the Financial Times, has reported that both CDB and China EXIM are in discussions with the European Bank for Reconstruction and Development regarding co-financing projects under international lending standards, while CDB is in discussion with the French Development Agency on a joint project.

In July the US, Japan and Australia announced a joint investment fund to support infrastructure investment in the Indo-Pacific, in a move seen as a response to the BRI. The announcement was coupled with a commitment by the US to provide US$113 million in funding for regional development projects.

Project updates

The focus on enhancing international co‑operation in the financing and management of BRI projects has coincided with a number of reports regarding challenges facing BRI projects, both planned and under way.

A BRI flagship project, the China-Pakistan Economic Corridor (CPEC), has come under increasing economic pressure as Pakistan navigates a potential BoP crisis, which was brought on partially as a result of Chinese financing of CPEC projects (thereby depleting Pakistan’s foreign-exchange reserves, due to debt-repayment obligations). In May the Chinese government approved the extension of an existing bilateral currency swap with Pakistan to three years, doubling the total amount covered to Rmb 20 billion (US$3 billion).

In July China authorized a fresh US$1bn loan to Pakistan—upgraded to US$2 billion in August—to boost its foreign-exchange reserves, on top of an existing US$4 billion in Chinese loans delivered to Pakistan in the year to June 2018. While we expect China to remain the major international financier for the country, there is a chance that Pakistani authorities could appeal to the IMF for a bail-out. However, the US government has opposed this idea, worried that these funds would be used to repay Chinese creditors without precipitating economic reform.

Despite these financial troubles, the newly elected government in Pakistan has indicated that economic ties with China, including CPEC, will remain important. In July China announced that it would host 1,000 Pakistani students on a Chinese government-backed scholarship as part of a training programme covering solar power, hydro power engineering, space and high-speed railways. In the same month a Chinese telecommunications giant, Huawei, began the operation of a US$ 4 million fibre-optic cable within CPEC, which is planned to extend to Gwadar Port (another CPEC project).

Not all projects have proceeded smoothly, however. In August Myanmar announced that it would scale down the scope of the Chinese-backed Kyaukpyu port project to US$1.3 billion, from US$7.3 billion initially. The project is meant to support existing energy pipelines stretching from Myanmar’s Rakhine state to China’s south-western Yunnan province.

Meanwhile, the freshly elected prime minister of Malaysia, Mahathir Mohamad, announced in May that the country would re-assess a number of BRI projects to determine their feasibility. In July Malaysia suspended work on US$23 billion worth of Chinese projects, including the East Coast Rail Link (ECRL), over financing concerns. Following a state visit to China in August, Dr Mahathir confirmed that these projects—including the ECRL and a natural gas pipeline—would be cancelled until further notice.

Pushback in BRI nations has not been uniform, however. Although Sri Lanka has struggled under its debt burden to China, handing over its Hambantota port to China for 99 years in December 2017, as part of a US$1.1 billion debt repayment, the country has shown little sign of resisting future investment. In May China lent Sri Lanka another US$1bn to repay other loans that had matured earlier, and approved another US$1bn loan from CDB to finance a road project in that country. In July China issued another Rmb 2 billion in flexible loans to Sri Lanka. Loans to other fragile states—including a US$5 billion loan to Venezuela for oil development, as well as US$20 billion in loans for oil and gas development in Syria and Yemen—indicate that China’s risk-management and debt-scrutiny mechanisms remain underdeveloped, or at least secondary to political or strategic objectives.

China’s Exports Are Homeward Bound

Mainland businesses hit by Trump’s tariffs hope domestic consumers will pick up the slack.

By Daniela Wei and Bruce Einhorn

August 9, 2018, 2:00 PM MDT

Chinese millennials are eating more seafood.

PHOTOGRAPHER: QILAI SHEN/BLOOMBERG

On July 11, Zhuo Peihui learned the profit margins on the wooden furniture he’s been selling to the U.S. for 13 years were about to evaporate. That’s because the dresser drawers and dining tables made by the more than 100 workers at his factory in the Chinese province of Guangdong had landed on Donald Trump’s latest tariff hit list.

Trump is betting that punishing penalties on Chinese industry will force Beijing to end trade practices his administration says are unfair. But China has at least one powerful strategy for limiting the fallout of the levies: getting the nation’s 1.4 billion people, especially its swelling ranks of middle-class shoppers, to spend more like Americans.

China furniture exporters sold $29.2 billion in goods to the U.S. last year. The $200 billion round of tariff proposals will have the biggest impact on their industry, according to Deutsche Bank AG. They face levies of 10 percent or even 25 percent. That’s spurred Zhuo and other furniture makers to seek sales closer to home. “Although the domestic market is new to us and competition is very fierce, at least the demand is here,” he says. “The market is huge, and customers are paying more for good products.”

With trade tensions between the U.S. and China seeming to worsen by the day, mainland companies selling everything from handbags to fresh food to Christmas lights are boosting their attempts to cultivate local demand. Take Taizhou Tianhe Aquatic Products Co. From its base in Zhejiang province in eastern China, more than 1,000 workers process 10,000 tons a year of freshwater crayfish, frozen squid, dory fillets, and other seafood for sale to the U.S., Europe, and Australia.

Many of those products are facing new levies in the U.S.; the almost 200-page list of targeted items includes dozens of varieties of seafood, with the penalties due to take effect after public consultations end on Sept. 6. Luckily for Tianhe Aquatic, Chinese millennials are having a crustacean fixation. Demand from urbanites in their 20s and 30s helped the economic value of the crayfish industry climb 83 percent last year even as U.S. exports dropped, according to a June government report.

“Consumers in China care more about the quality of food and consider eating food that is popular in the U.S. and Europe to be fashionable,” says sales representative Doris Chen. Tianhe can’t keep up with local demand, even though it’s charging more and boosting profit margins, she says. “We can drop the U.S. market if we want.”

At the more than 3,000 supermarkets run by state-backed China Resources Holdings Co., shoppers have pushed up sales of jumbo Argentine red shrimp 20 percent in the first six months of this year. That’s because local demand is rising and Chinese middlemen who imported the shrimp with plans to sell them to the U.S. are selling them to the local grocery chain instead, according to the company.

Even before the escalation of trade tensions, the growing spending power of Chinese consumers was attracting greater interest from local producers who’d traditionally sold their goods overseas. Household consumption accounted for more than 39 percent of China’s gross domestic product in 2016 and 2017. That was the highest since 2005. “The trade war will highlight the change,” says Iris Pang, an economist with ING Bank NV in Hong Kong.

Chinese shoppers are still vastly under performing as engines of growth compared with their counterparts in the U.S., where personal consumption accounted for about 70 percent of GDP last year. Addressing that imbalance is an important part of President Xi Jinping’s plan to restructure the world’s second-biggest economy.

It’s not always easy to get mainland customers to mimic America’s consumerist habits. SDIC Zhonglu Fruit Juice Co. accounted for about 20 percent of China’s 654,000 tons of apple juice concentrate exports last year. Customers include Coca-Cola, Nestlé, and Kraft Heinz, and most of its output is exported to the U.S. and other developed markets. The Trump administration’s latest tariff list includes all types of juice.

So SDIC Zhonglu is trying to win over Chinese parents, who traditionally haven’t given the drink to kids. “We are studying and launching new products to create more juice demand among Chinese consumers,” the company said in a statement. “The China-U.S. trade war is speeding up our shift in market structure and product structure.”

Another big challenge for mainland manufacturers: Many Chinese associate local brands with poor quality. But businesses that have traditionally sold their wares to the U.S. have an advantage, says Fielding Chen, China economist for Bloomberg. “If you can export to the U.S., that means your quality is good,” he says. “This will be very good for them in developing the domestic market.”

Zhuo, the furniture maker, says he hopes that’s the case. While he already sells domestically through an online storefront and is building a physical store, local sales account for only 20 percent of his business so far. “This market gives hope and opportunity for manufacturers to gain big profits.” —With Dong Lyu

BOTTOM LINE – The trade war is forcing Chinese businesses that had focused on exporting to the U.S. to court consumers at home. That could remake the mainland economy in the long term.

Strafor Worldview Situation Report

Oct. 8 2018

What Happened: China’s central bank has announced a cut in reserve requirement ratios that is expected to free up as much as $105 billion worth of liquidity, Caixin reported Oct. 7.

Why It Matters: The central bank’s decision is Beijing’s latest step toward a pro-growth fiscal and monetary policy designed to mitigate the effects of a slowing economy and the ongoing trade war with the United States.

Background: Beijing has now moved to cut reserve requirement ratios three times in the past six months to weather the trade war. President Donald Trump has announced tariffs on nearly all Chinese imports into the United States; China has responded with similar tariffs on U.S. goods.

Read More:

- S. Tariff Threats Give China All the More Reason to Reform Its Auto Sector (Sept. 24, 2018)

- China, U.S.: The Trade Fight Escalates With New Rounds of Tariffs (Sept. 19, 2018)

- These Are the Areas Where U.S. Tariffs Will Hit China the Hardest (Aug. 31, 2018)

Pei Xin | Xinhua | Getty Images

Trade volume and activities have been going up within Asia, but that could soon change depending on which way trade tensions between the U.S. and China swing.

In the past year, growth in Asian trade corridors has increased, according to data derived from Citi’s support of clients’ trading activities.

The bank’s client business between South Korea and India went up by 55 percent between April 2017 and March 2018. Between China and the ASEAN (Association of Southeast Asian Nations) region, it shot up by 66 percent in the same period. Overall, its growth in Asia has gone up by 26 percent year on year, the bank said.

Increasingly, Asia “is relying more on Asia” as consumption goes up, Munir Nanji, Citi Global Subsidiaries Group’s head for Asia Pacific, told CNBC.

According to statistics from the World Trade Organization, world trade volume for goods went up by 4.7 percent in 2017, the highest since 2011 and a leap from the 1.8 percent growth in 2016. The 2017 increase was driven by rising import demand from Asia, as well as increased investment and consumption expenditure. In fact, Asia had the fastest trade volume growth of any region in 2017 for both exports and imports — 6.7 percent and 9.6 percent, respectively, the WTO said.

However, the ongoing trade spat between the U.S. and China may soon start to have an impact on Asia, especially emerging markets, experts say.

The WTO acknowledged that risk in its outlook for 2018 and 2019: “Balanced against these broadly positive signs is a rising tide of anti-trade sentiment and the increased willingness of governments to employ restrictive trade measures.”

But it could also be a good thing for certain markets in Asia, as companies look for alternative supply sources beyond the U.S.

What’s driving trade flows within Asia?

Trade-related growth between China and the ASEAN region is fueled mainly by infrastructure needs, while between South Korea and India, automotive and electronic goods are flourishing, according to Nanji.

A common theme is technology: Firms in China and South Korea are increasingly bringing their investments and tech into other parts of Asia.

“Generally, Asians are buying more from Asian companies. Both demand and supply is coming from Asia,” said Nanji, who noted that it used to be American and European companies providing the supply.

For instance, the components of most smartphones are mostly manufactured in Asia, he said.

Various countries’ initiatives are also helping to drive growth. That includes the Make in India initiative, which encourages companies to manufacture their goods in India, and the Shanghai Free-Trade Zone.

Trade spat could shift the movements of goods

In recent weeks, both China and the U.S. have threatened to impose tariffs on each other’s products.

J.P. Morgan analysts wrote in a note that there would be knock-on effects for the rest of Asia if the various tariffs suggested by U.S. President Donald Trump were to come into effect and result in a fall in Chinese exports to the U.S.

“Indirect links propagate shocks into the region, and could impact trade and growth … the product categories encompass mainly high-tech products, which would include electronics,” the note said.

“By its very nature, such products are highly reliant on tightly integrated supply chains. To that extent, this would propagate any trade shock into the region.”

The impact would be felt most in countries such as South Korea and Taiwan, the analysts said.

But it might spell good news for some markets. India, for example, would likely benefit from the spat — in the area of cotton exports.

The U.S., the world’s biggest exporter of the fiber, had cornered the bulk of Chinese demand. But China’s move to impose a 25 percent import tax on American farm commodities, including cotton, in retaliation for tariffs enacted by the U.S., may allow India to grab a bigger share of the Chinese market, according to a Reuters report.

In fact, India has already signed contracts to ship 500,000 bales (85,000 tonnes) of its new season harvest to China, in rare advance deals, officials said.

“If China decides not to buy agricultural products from the U.S., that could move to different parts of Asia to buy, to source it. The U.S., on the other hand, needs to export that somewhere else, so it would find another corridor,” Citi’s Nanji said.

“So when you have a trade war, the countries involved would have to go somewhere else. So other countries would benefit. Some of them could be in Asia, or Latin America. There will be shifts in trade corridors … the question is, where it shifts.”

— Reuters contributed to this report.

Weizhen Tan Markets Editor, CNBC Asia markets

Weizhen Tan Markets Editor, CNBC Asia markets

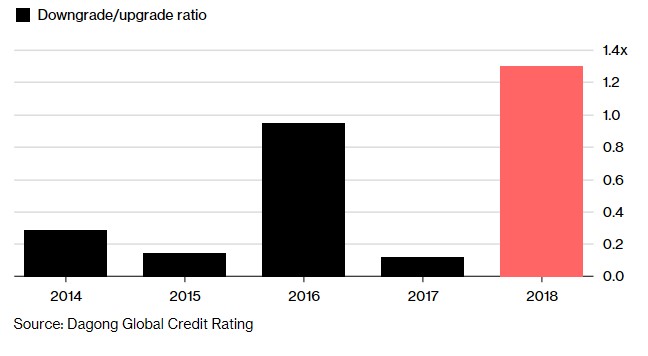

China Set for Record Defaults, and Downgrades Tip More Pain

Bloomberg News

July 2nd , 2018 3:00 PM

- Total so far this year is approaching full tally for 2016

- Regulators still seen intervening in case of systemic risk

Bloomberg’s Lianting Tu reports on China’s corporate bond defaults.

China is zooming to a record year of corporate-bond defaults.

Chinese companies have reneged on about 16.5 billion yuan ($2.5 billion) of public bond payments so far this year, compared with the high of 20.7 billion yuan seen 2016, according to data compiled by Bloomberg. Strains are set to get worse if the downgrading trends of credit-rating companies are anything to go by . Dagong Global Rating Co. have been downgrading firms by an unprecedented margin.

Drastic Turn for The Worse

Chinese local bond issuers face the worst rating trend this year

Source: Dagong Global Credit Rating

“Corporate profits have deteriorated this year and are unlikely to improve against the backdrop of an economic slowdown,” Li Shi, general manager of the rating and bond-research department at China Chengxin International Credit Rating Co. “Refinancing will continue to be tough as long as the crackdown on shadow banking continues.”

The domestic corporate-debt market is almost exclusively a domestic issue. Foreign investors normally gravitate to government-linked securities as China has boosted access to government bonds in recent years. The worsening in credit quality offers little incentive to dip in now, though in time analysts see a more disciplined credit market offering diversification opportunities.

In the meantime, rising yields are set to make the refinancing of maturing debt all the tougher for private companies that lack the access to the state-dominated banking system that national behemoths enjoy. With the People’s Bank of China making only limited steps to support credit to private companies, borrowing costs show no sign of dropping.

Borrowers have missed payments on at least 20 domestic bonds so far this year, according to data compiled by Bloomberg. There was about 66.3 billion yuan of defaulted notes outstanding at the end of May, or 0.39 percent of corporate bonds outstanding, PBOC data show. While still small, that share may be poised to rise.

Dagong has reported 13 credit-rating downgrades compared with 10 upgrades so far this year, the highest such ratio on record, according to Bloomberg-compiled data. Results from Dagong peers such as China Chengxin International Credit Rating Co. and China Lianhe Credit Rating Co. show similar trends.

The silver lining is that the defaults show Chinese regulators are increasingly comfortable with allowing struggling companies to fend for themselves without official rescues. Bond defaults are good for the long-term development of Chinese markets, Pan Gongsheng, director for State Administration of Foreign Exchange, said in Hong Kong Tuesday.

‘Necessary’ Defaults“They are necessary for better credit-risk pricing and will create a healthier bond market in the long term,” Christopher Lee, managing director of corporate ratings at S&P Global ratings in Hong Kong said of defaults. “It is unlikely there will be a wave of large-scale defaults or concentration of defaults — any such developments will be quickly contained to prevent systemic risks from emerging.”

With rising trade tensions with the U.S. threatening to hurt corporate cash flows, the temptation to shore up credit provision may rise. Data over the weekend showed that a gauge of export orders tumbled into contraction in June.

An escalation of the trade conflict could add to defaults in China’s financial system, said Jing Ulrich, JPMorgan Chase & Co.’s vice chairman for Asia Pacific. Consumer demand and the wider economy are likely to weaken and that “may translate into worse credit quality down the road,” she said in a Friday interview in Hong Kong.

“The volume of bond defaults will most likely surpass 2016 and hit a record this year,” said Lv Pin, an analyst in Beijing at CITIC Securities. While most failures in 2016 were from state-owned firms in industries with excess capacity, the majority of defaulters this year have been private-sector firms. With a variety of industries represented, the data show the breadth of the deterioration, he said.

| Read more on China’s credit markets: |

|

— With assistance by Lianting Tu, Jing Zhao, Yuling Yang, Ling Zeng, and Alfred Liu

China’s housing market marks policy anniversary in doldrums

Financial Times October 30, 2018

Two years ago this month, the Chinese government called time on a burst of housing market speculation unleashed by its recourse to stimulus in the wake of the economic turmoil of 2015. Local governments were compelled to bring red hot housing markets under control as part of a policy drive hinged on the official line that “houses are for living in, not for speculation”.

Since then, the market has speculated on just when the central authorities would once again relax their stance and allow local governments en mass to ease restrictions on home purchases.

The speculation has recently intensified on signs that broader economic growth is suffering from the government’s deleveraging campaign — the historical record shows how effective pumping up the housing market can be in boosting economic growth. Although our consumer surveys show that nearly a third of urban households already own two or more properties, a traditional belief in the sanctity of bricks-and-mortar, combined with an absence of reliable investment alternatives, mean underlying demand for property remains strong.

The latest FTCR China Real Estate Index shows the impact that two years of tight policy have had on the housing market. The headline index, based on a survey of 300 developer sales offices around the country, fell to 41.5 in October, its lowest level since the start of 2017. Sales across all city tiers fell for a fourth straight month as nearly 60 per cent of developers said even first-time buyers were having to pay above benchmark rates to secure a mortgage — up from just 6.6 per cent in October 2016.

Developers indicated that prices rose again in October — marking the fourth straight year that they have done so — even if at their weakest pace since February 2015. Our separate survey of urban consumers showed that price expectations weakened further in October, though the fact that more than 60 per cent of respondents still expect gains in the coming six months suggests the government’s tough policy line is only slowly getting through to buyers.

Officials are easing credit policy in response to signs of financial strains caused by the deleveraging campaign, and by the hit to sentiment from US president Donald Trump’s trade war. However, property policy remains off limits because the government in large part blames housing market speculation for China’s debt problems.

At least some of the extra funding added to the system this year is likely to wind up in the property market, if only because it usually does. For now, however, the central government looks likely to continue trying to use targeted relief measures, aimed predominantly at small, private companies, to shore up growth. If the government were to relax its housing market restrictions in the coming months, this would be a sign that the leadership has again put vigilance on debt to one side and upgraded its economic threat level.

Housing sales fell across all city tiers under coverage for a fourth straight month, with the weakest activity again seen in third-tier cities. Our Home Sales Index fell 3.2 points to 39.1.

First-time buyers were once again the biggest source of demand (43.9 per cent of total buyers) while upgraders accounted for 39.3 per cent. Additional homebuyers made up 16.8 per cent of purchasers.

House price inflation cooled for a fifth straight month, with our price index falling 0.4 points to 52.5. Among respondents to our survey, 70.7 per cent said that prices were unchanged relative to September. The index has been above 50, pointing to rising prices overall, since September 2014.

Among developers, 52.1 per cent said they offered discounts last month. Nearly 80 per cent were offering discounts just over two years ago, when purchase restrictions were loosened to prop up economic growth.

The supply of new units to the market fell across all city tiers for a fourth straight month. Our New Home Supply Index fell 2.5 points to an eight-month low of 45.

Our Home Sales Outlook Index fell another 6 points to 44.6, its lowest reading in almost two years. Price expectations were less bullish for a sixth straight month, with our Home Price Outlook Index down 3.8 points at 52.6, the lowest reading since February 2015.

The proportion of developers reporting that first-time buyers were having to pay above the benchmark mortgage rate rose to 56.4 per cent from 55.7 per cent in September. In May, a record 63.6 per cent of first-time buyers were paying above the benchmark.

Our Home Sales Index for first-tier cities fell 4.7 points to 40.9; in second-tier cities it fell 5.3 points to 40.2, while in third-tier cities it rose 1.5 points to 36.4. Our first-tier city house price sub-index fell 2.1 points to 52.3, while the second-tier city sub-index fell 1.7 points to 54.8. The third-tier city index rose 2.7 points to 48.4. The FTCR China Real Estate survey is based on interviews with 300 developers in 40 cities. For further details click here. This report contains the headline figures from the latest Real Estate survey; the full results are available from FT Database.

For all the ink spilled about a U.S.-China trade war — with the Federal Reserve eyeing the economic fallout and the like — the move suggests that the conflict is not at all conducive to a bull steepener. (That’s where the yield gap widens as two-year rates fall by more than their 10-year counterparts, as traders reduce Fed hike expectations.) Also backing that idea are the central bank’s dot plot and its assessment of the economic outlook. Put simply, the Fed’s concern about the ramifications of an onslaught of tariffs is dwarfed by its optimism on the U.S expansion.

The minutes from the July meeting showed that four officials saw the risks to growth as tilted to the upside (up from two in March), while a lone wolf continued to see things the opposite way. None viewed the risks to core inflation as biased to the downside. Add it all up, and it looks like Larry Kudlow’s wish might not come true.

But Brian Reynolds at Canaccord Genuity sees another way in which trade tensions have had an impact. “Banks were buying more Treasuries as they put on the ‘carry trade,’ buying longer-term bonds utilizing shorter-term funding,” he writes about the second quarter — suggesting the activity was driven by “trade-war worries.”

Meantime, nobody told break evens that trade wars were inflationary, or would foster a steepening in the inflation-risk premium. It’s possible that break evens could be distorted by a flight to safe and liquid assets thanks to deteriorating ties between the world’s two largest economies. But since these concerns about trade ratcheted higher in mid-June, market-based measures of inflation compensation actually drifted marginally lower — until Wednesday, at least.

Breakevens did perk up materially that day, particularly the two-year tenor, which extended their advance after the Fed minutes referenced “supply constraints” on three occasions. As Bespoke Investment Group macro strategist George Pearkes observes, that’s the first time the phrase has appeared more than once in this communique in at least a decade. The Fed is bullish on growth and shifting to inflation-prevention mode under the presumption it’s the best way to sustain the expansion for as long as possible. Others might see continued Fed tightening as bringing the end of the cycle all the nearer.

Which in turn leads to an astute quip from Family Management Corp. CIO David Schawel on Twitter: “If you believe the yield curve flattening, and think we eventually go back into a recession with the Fed cutting, then the 5-10y part of the curve isn’t as unattractive as many think.

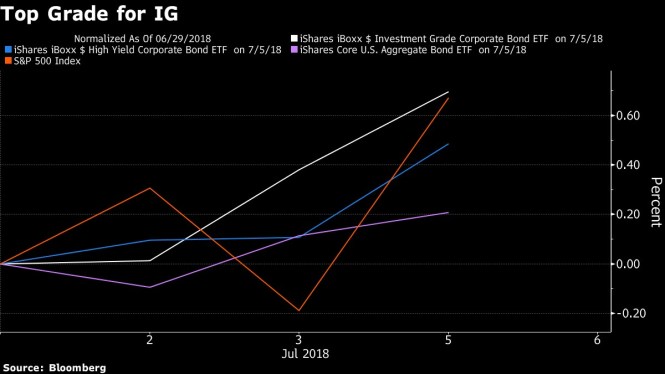

A Reprieve from IGnominy

It’s just three sessions into the third quarter (if you’re in the U.S.). But after blue-chip corporate debt was the worst-performing U.S. asset in the first half, it’ll take any stretch of out performance it can get:

A recent Citigroup survey shows just how unloved investment grade U.S. debt is: hedge funds have pared their holdings in the most aggressive fashion since early 2016, with allocations at the lowest level since 2008. Bloomberg’s Sid Verma notes that this may actually be a contrarian bullish signal, because it means funds have more room to add to the asset class going forward.

But any time in the sun may prove fleeting should long-term yields trend back to their 2018 highs.

“IG has become more of a duration product as well in the past few years, so if intermediate rates stay range-bound in Q3 (as we expect) and issuance remains subdued (given the summer low-issuance period ahead), then this might be the one quarter of 2018 where IG catches a bid,” writes George Goncalves, head of Americas fixed-income strategy at Nomura, who warned that the soft-supply dynamic wouldn’t last forever.

“We would use any tightening of spreads to lighten up on IG, as duration-based products are likely to suffer in the coming quarters and we anticipate that the higher-rates theme will eventually become a credit story, where HY and IG are both hit,” Goncalves says.

To his point on rate sensitivity, mid-April saw bond managers’ allocation to corporate debt as a share of assets deteriorate as the 10-year Treasury yield made its push through 3 percent for the first time since 2014. It’s a picture of what happens when duration risk and the competition for capital collide.

Buyout activity could change the supply picture materially for IG, to boot. Bloomberg Intelligence estimates more than $1 trillion in pending deals, and strategists warn of a flood companies coming to tap the market, raising questions about whether that’s already priced in. That’s the major wild card for high grade — and to a certain extent for the Russell 2000 Index as well, as many potential acquisition targets in the health care space have gone on tears this year.

The Chinese Road More Traveled

“Two roads diverged in a wood, and I—

I took the one less traveled by,

And that has made all the difference.”

-Robert Frost, The Road Not Taken

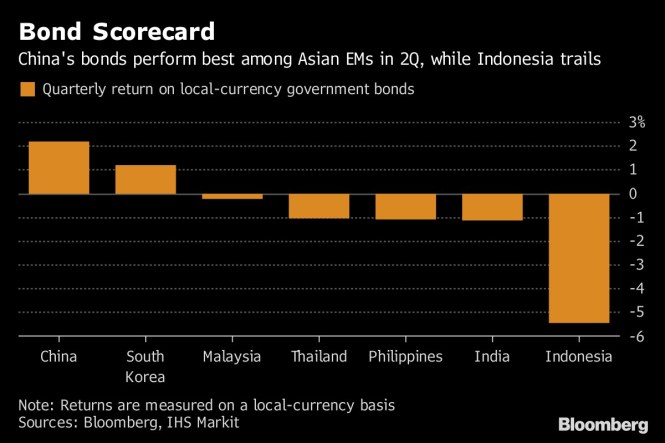

Chinese policy makers either haven’t read Robert Frost, or they don’t agree with him when it comes to economic policy. Their tendencies have been clear, and repeated. When Beijing senses that any trade-off between growth and deleveraging poses a significant threat to the former, its policy stance shifts to prioritize current activity. No wonder Chinese debt topped the second-quarter leader board for Asian EM local-currency performance. in anticipation of an accommodative response by the People’s Bank of China to the brewing battles over commerce.

The pseudo-monetary stimulus that’s ensued also has one Chinese hedge fund calling for a bottom in the nation’s embattled equities.

Meanwhile, PBOC adviser Ma Jun hinted that the deleveraging campaign won’t take a “one-size-fits-all” approach. Unsurprisingly, more than a whiff of moral hazard (along with the smog) lingers in the air. The head of financing at state-owned Qinghai Provincial told Bloomberg he doesn’t expect the government to let the issuer, considered to be a local government financing vehicle in some quarters, default on its obligations. Drawbacks aside, the China model of targeted curbs may be preferable to the West’s reliance on the blunt tool of interest-rate adjustments as a moderating force for the modulations of the business cycle.

The big question is: how is China going to keep its currency stable and run broadly accommodative monetary policy while shrinking leverage in the midst of a Fed tightening cycle? Possible ways to square this circle include further targeted cuts to banks’ required-reserve ratios, additional lending to policy banks and capital controls.

Plan to Dismount

You have to feel sorry for the Fed. The pressure on its policy target isn’t the Fed’s making, but it’s the only entity that might be willing and able to offer a solution. Massive debt issuance by the Treasury is propelling short-term bill rates higher, and demand hasn’t been that hot recently, either. This deluge, which has pressured a variety of short-term rates higher, is prompting would-be lenders in the federal funds market to engage in more profitable opportunities elsewhere.

As a result, there’s a dearth of liquidity in that corner of the market, and that has helped push the effective fed funds rate up towards the top of policy makers’ target range.

U.S. fiscal policy is therefore the prime culprit for why the Fed is encountering problems with plumbing of monetary policy. Regulatory confusion is somewhat to blame for banks’ hoarding of reserves, too.

At the same time, the Fed is destroying reserves via its unwinding of asset purchases, potentially exacerbating the issue. Since that’s the primary lever the Fed can use to alleviate upward pressure as it proceeds with hiking rates, analysts are beginning to suspect Chairman Jerome Powell and his team will pull it. That entails pausing, slowing or ending the shrinkage of the Fed’s bond portfolio.

In the minutes, a few participants suggested that “before too long, the Committee might want to further discuss how it can implement monetary policy most effectively and efficiently when the quantity of reserve balances reaches a level appreciably below that seen recently.”

Some might find it peculiar that balance-sheet normalization has been on an explicit preset course despite the Fed having taken care to stress that its trajectory for rates wasn’t on any such divined trajectory through the tightening cycle. So perhaps this ahead-of-schedule incident may have a silver lining: it’s a reminder that the balance sheet is, and likely will be, an active tool for major central banks for the foreseeable future — regardless of any protestations otherwise.

Meanwhile, here is a central bank whose control over the market is something to marvel at.

‘Bout That Basis

It’s been a while since the ISDA basis graced these pages. This is an oversight. As a refresher, this refers to the difference in pricing for credit-default swaps that include currency re-denomination as an event of default versus ones that do not. Even as Italian sovereign yields have retraced a sizable portion of their rise, the ISDA basis has blown out and remained near record highs.

The ECB certainly doesn’t seem shaken by Italian politics. Instead, some policy makers are said to be concerned that markets don’t see a rate hike until the end of 2019, because the lift-off could come sooner. That revelation weighed on sovereign debt in the currency bloc on Wednesday. Perhaps there’s some merit to downplaying the effect of the political drama on economic activity — particularly since Italian officials are far from dead-set on withdrawing from the currency union.

“Nobody wants to leave the euro, but if we don’t fix it, things risk getting worse,” said Italian Finance Minister Giovanni Tria. But in a show of defiance to financial markets, the new government is putting tax cuts and a universal basic income in its first budget. At the same time, it’s asking the European Commission to extend a state loan-guarantee program that’s helped bad bank assets find good homes.

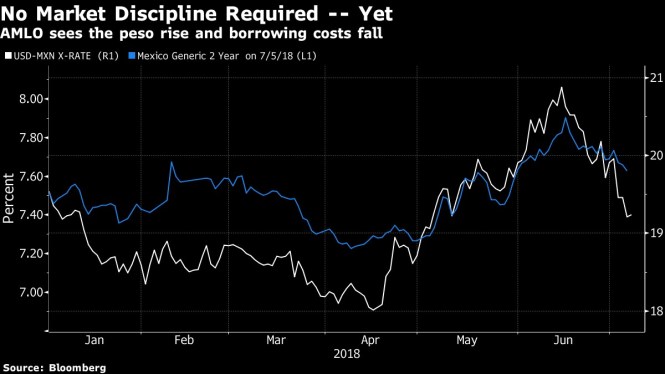

Contrast Italy’s situation with the early whispers out of Andres Manuel Lopez Obrador’s purportedly leftist, populist government in Mexico. His chief of staff said AMLO wouldn’t use his legislative might to roll back the oil reform of 2013, stressing the need to avoid “hurting private investment.” To adapt Obi-Wan Kenobi, these are not the populists you’re looking for. For the time being, at least. Accordingly, the peso is stronger and two-year yields are lower since his victory.

In fact, it’s the best performing currency among the expanded majors tracked by Bloomberg. It seems the election was a case of “buy the rumor, sell the news” for dollar-peso.

China Economic Update

By Eric Wong

Managing Director, Canada Wood China

July 26, 2018

Posted in: China

2018 Q2 highlights:

- China has posted its Q2 GDP growth of 6.7%, slightly lower than 6.8 percent in Q1 of 2018. Tighter financial conditions (such as authorities continue to demolish on shadow banking and back up financial deleveraging) led to a moderated economic growth in first half of 2018, while manufacturing output moved slower but high-tech related activities remained solid growth; resilient domestic demand helped China maintain strong growth this year even though recent data show its economy is making slower paces. Focus Economics experts forecasted a 6.5% economy growth nationwide in 2018 and 6.3% in 2019.i

- Property sales went down for the first time in six months due to continued speculation restrictions and rising mortgage rates both led by the government. However, new starts of real-estate construction in Q2 grew 11.3% compared 2017Q2 to 1.46 billion m2.

PMI (Caixin) indexes remained steady in Q2, both hit 51.1 in April and May and slightly decreased to 51.0 in June.ii Followed by a 12.6% year-on-year growth in May, China Exports achieved a 11.3% gain compared with the same period of last year to USD 216.7 million in June which surpassed the 10% growth forecast previously.iii

China Consumer Price Index (CPI) kept unchanged in April and May (101.8) and slightly raised to 101.9 in June.iv USD/CNY had been on the rise in Q2, increased from 6.34 (May 1st) to 6.42 (June 1st) and hit 6.62 on July 1st;v CAD/CNY kept the similar upward trend, went from 4.93 (May 1st) to 4.95 (June 1st) and hit 5.04 on July 1st.vi

Wood import data ceased to renew since March 2018

A notification was distributed from China Customs that all wood import data ceased to renew since March 2018 for now. BOABC, our regular data vendor informed Canada Wood China that all data renewal work will be back on track soon, China Economic Update will analyze data starting from April in detail at the end of Q3 2018.

Building material prices

Cement price dropped slightly from RMB 447.50 to RMB 441.67 per metric ton (down 1.30%) over June 2018.vii On the other hand rebar steel price went up lightly by 0.35% from RMB 4,007.86 per metric ton on June 1st 2018 to RMB 4,022.00 per metric ton on June 30th 2018.viii The log price index in March 2018 was 1,115.91 points which decreased 0.48% less than February 2019 and grew 2.22% compared to the same period year-on-year; the lumber price index in March 2018 was 1,123.99 which went down slightly of 0.33% month-on-month and decreased 0.56% year-on-year.ix

Wood import of Chinax

China softwood lumber imports reached 2.05 million m3, dropped 1.43% year-on-year and increased 63.43% month-on-month which fits the trend each year that the import volume always rises after Chinese New Year. From January to March 2018 the total volume of softwood lumber imports hit 5.37 million m3 with 0.28% growth year-on-year; of which the imports of Fir & Spruce and Radiata pine was 2.12 million m3 (down 0.1% year-on-year, accounts for 39.5% of total softwood lumber imports) and 0.27 million m3 (up 2.2% year-on-year, constitutes 5% of total softwood lumber imports) respectively.

In March China softwood lumber imports from Russia, Canada and Finland achieved 1.16 million, 0.34 million and 0.13 million m3 respectively. From January to March 2018 the above-mentioned three countries represented 57.36% (up 5.38% year-on-year), 16.56% (down 21.71% year-on-year) and 7.21% (up 4.68% year-on-year) of total softwood lumber imports.

Focus Economics (June 19th, 2018). China Economic Outlook

ii Trading Economics (July 15th, 2018). China Caixin Manufacturing PMI

iii Trading Economics (July 15th, 2018). China Exports

iv Trading Economics (July 15th, 2018). China Consumer Price Index (CPI)

v XE Currency Charts: USD to CNY

vi XE Currency Charts: CAD to CNY

vii Sunsirs (July 2018). Spot Price for Cement

viii Sunsirs (July 2018). Spot Price for Rebar Steel

ix BOABC (June 2018). China Wood and Its Products Market Monthly Report

x BOABC (January to June 2018). China Wood and Its Products Market Monthly Report

Canada Wood China inks MOU with China Railway Real Estate Group

By Kajia Deng

July 4, 2018

Posted in: China

Canada Wood China (CW China) signed a Memorandum of Understanding (MOU) with China Railway Real Estate Group on June 20 in Beijing.

The two sides agreed to develop a long term strategic partnership, which will focus on development of wood construction in Xiong’an, a new economic zone founded in April 2017. China wants Xiong’an to be a low-carbon, smart, livable and globally influential city.

The MOU sets the goal and principle for the cooperation between the two parties and allows CW China to introduce wood construction into the development of Xiong’an through an extensive range of activities including researches, technical transfer and promotion programs, etc.

Canada Wood China is dedicated to promoting the use of legal timbers and wood trade between the two countries, as well as consolidating Canada’s position as the world’s largest wood products exporter and a world leader in modern wood structure technology.

China Railway Real Estate Group was founded in 2007 with a registered capital of 6.5 billion yuan. It is a wholly owned subsidiary of China Railway Group Limited and its only company involved in the real estate sector.

The group develops real estate projects and offers a range of property services.

As the U.S.-China trade war threatens supply chain disruptions and China amplifies cross-strait tensions while growing more technologically competitive, Taiwan has urgently emphasized the development of economic relations beyond the mainland.

PATRICK LIN/AFP/ Getty Images A container truck drives along a pier at Taiwan busy northern Keelung harbor.

Highlights

- Taiwanese electronic firms are still more advanced than mainland China’s in developing most cutting-edge technologies, but they are increasingly linked to mainland supply chains.

- This integration could help Beijing move up the production value chains, compromising Taiwan’s competitive advantage.

- U.S.-China trade tensions will likely increase production costs and push Taiwanese-owned, low-end manufacturing companies to move away from China and into Southeast Asian states.

- Though Taiwan will continue to struggle to form regional, multilateral free trade agreements, it could see more success pursuing bilateral deals with the mainland’s biggest rivals.

Taiwan is caught in the middle of the escalating trade war and larger strategic competition between mainland China and the United States. And the clash is threatening the self-governing island’s export- and tech-oriented economy, which relies heavily on the mainland’s supply chains for assembly, export opportunities and market access. (This is particularly true for its electronic and semiconductor industries, which together account for about 25 percent of the island’s gross domestic product.)

The Big Picture

The trade tensions between China and the United States are unsettling global supply chains. This disruption will have an impact on Taiwanese businesses, many of which are closely linked with the mainland. Combined with Beijing’s increasing use of coercive tactics against Taipei since Taiwanese President Tsai Ing-wen took office, these issues are driving Taiwan to diversify its economy away from mainland China.

See 2018 Fourth-Quarter Forecast

See Asia-Pacific section of the 2018 Fourth-Quarter Forecast

Adding to Taiwan’s economic troubles is Beijing’s two-pronged campaign to diplomatically isolate the island and poach its businesses and talent, all in the hopes of eventual reunification. Together, these threats are increasing Taipei’s desire to rely less on the mainland’s economy, to diversify its trade and investment relationships with its neighbors, particularly India and those in Southeast Asia, and to establish more free trade agreements. In the past, these efforts have had mixed results, but the current economic and strategic pressure will likely harden Taipei’s resolve in the coming months.

Deepening Connections

Over the past two decades, disputes over sovereignty have contributed to a volatile political relationship between Taiwan and mainland China. But at the same time, trade and investment links between the two have grown. Taiwanese investments into the mainland have steadily increased since Beijing opened up access in the early 1990s. Because of a similar culture and language, and the mainland’s huge market potential and cheap labor, many capital-rich Taiwanese businesses relocated to the mainland. Today, China accounts for over 40 percent of Taiwan’s exports, of which 80 percent are intermediary goods that are assembled in China before being sold domestically or exported.

These developments have had the added effect of nurturing China’s economy during its reform and transformation era. The Taiwanese business community not only serves as a top capital source for once cash-strapped China but has also become an important means through which Beijing could influence the island and forge cross-strait connections.

And as such links grew, Taiwan found it had few options besides mainland markets and production. The island’s economy was plagued by years of stagnation, low wages and productivity throughout the 2000s, and it continues to face high-tech competitors in South Korea. Indeed, during the global financial crisis of the late 2000s, former Taiwanese President Ma Ying-jeou’s administration removed a host of restrictions on investment in key high-tech sectors on the mainland, contributing to an even heavier dependence on the mainland economy and creating new cross-strait supply chains in those industries.

As Taiwanese electronics firms outsource to mainland China, they are keeping higher value-added work — such as the development of semiconductors, chips and other key electronic components — at home. But a significant portion of these components are supplied to Chinese, Taiwanese or foreign firms in China. As much as 90 percent of Taiwanese-branded computers, laptops and mobile phones are produced outside the country, with a majority being produced in mainland China.

The Consequences of Linking Supply Chains

While the mainland and Taiwan have both benefited from their interconnectedness in economic terms, the relationship has spurred increasing debate within Taiwan about its impact on the island’s de facto independence. The mainland’s relatively high-skill, low-cost labor and integrated supply chains offer Taiwanese businesses competitive advantages, but they also open up the opportunity for China to interfere with Taiwan’s internal politics and, in a more extreme scenario, to challenge its industrial development.

Beijing’s ultimate imperative is reunification, so it has been careful in applying serious economic pressure on Taiwanese businesses on the mainland. But it has increasingly leveraged its economic influence to try to shape Taiwan’s internal politics in its favor, as it did during Taiwan’s presidential election in 2012.

Moreover, a heavy reliance on overseas production is eroding the Taiwanese incentive to innovate and allowing mainland competitors to gain knowledge as China pushes to move up the value chain. This drive threatens Taiwan’s competitive advantage in lower-end technology sectors. In particular, Beijing has been moving aggressively to develop a more self-reliant semiconductor industry, as outlined in its signature Made in China 2025 project.

These developments could have several implications for Taiwan. China has ramped up its efforts to absorb talent and technological capability, and Taiwan is a target due to Beijing’s reunification goal and its strategic intention to move up the semiconductor value chain. And Beijing’s capital- and state-led efforts are expected to boost China’s tech industry, putting Taiwanese companies in a race to climb the ladder of cutting-edge technology.

Of course, as the ZTE case has illustrated, Beijing is still perhaps a decade away from its goal of achieving greater technological independence, while Taiwan holds a leading position in the most advanced technologies, such as integrated circuit design, fabless integrated circuits and foundries. But the mainland’s efforts to climb the value chain with products such as solar panels and smartphones have rapidly eroded Taipei’s advantages in those global markets.

Taiwan Strives to Diversify

As the U.S.-China trade war threatens to disrupt supply chains and as China amplifies cross-strait tensions while growing more technologically competitive, Taiwan has urgently emphasized the development of economic relations beyond the mainland, which the island has pursued in one form or another for the past several decades.

Since taking office in 2016, Tsai has implemented her “New Southbound Policy” to ramp up connections with and investment in Southeast Asian states and India — an extension of similar goals held by two previous administrations. Her government has also accelerated its longtime quest for free trade agreements, hoping to better integrate Taiwan’s economy on a global level. This was a goal in the 2000s as well, as the proliferation of regional free trade agreements threatened to undermine Taiwan’s competitive advantage in the Asia-Pacific.

But the previous diversification policies didn’t yield much progress, since Beijing’s ever-growing and outperforming economy meant China remained the most lucrative place for investment. And Taiwan’s attempts to join multilateral free trade agreements, such as the Regional Comprehensive Economic Partnership between the 10 members of the Association of Southeast Asian Nations (ASEAN) and the Trans-Pacific Partnership, didn’t yield much success due to the island’s political status and the concerns of some countries that they would risk backlash from Beijing.

In the two years since Tsai took office, Taiwanese investment in Southeast Asia has moderately picked up but still fell short of what the island was investing in those regions in the late 1990s and early 2010s. Most of the current investments are concentrated in the retail and financial sectors, indicating that they are primarily oriented to capture those growing markets instead of directing markets away from mainland China. Moreover, Taiwan has so far made few electronics investments in Southeast Asia (with a few in Malaysia and Indonesia and some most recently in Thailand). After two decades of developing sophisticated, well-functioning supply chains for items such as semiconductors, Taiwanese businesses are less than eager to relocate and abandon the growing domestic Chinese market.

What’s Different Now

But Tsai’s conviction of the need to diversify Taiwan’s economy is strong, and things may change this time around. Many countries in the ASEAN, such as Vietnam, Indonesia and the Philippines, are developing strong economies of their own, working to move up the value chain and moving factories out of China. Inspired by their success, Taipei will likely work hard to keep up. Additionally, even as Taiwan remains an unlikely candidate for regional free trade agreements in the short term, its quest for bilateral free trade agreements with the United States and, to some extent, India may get new momentum as Washington challenges the current state of cross-strait relations.

All these developments, combined with the protracted U.S.-China strategic competition that could disrupt critical supply chains and with a mainland government that is increasingly challenging Taiwan’s autonomy, will drive Taipei to focus on its goal of disengaging its economy from the mainland, despite the barriers to that objective.

Russia: lumber export value 17.8% up in Jan-Apr 2018

July 13, 2018

Source:

FTS/Fordaq

In January-May 2018, Russia increased its sawn timber exports, both in value and in volume terms, indicate the statistics published by the Russian Federal Customs Office.

Thus, during the first five months of the current year Russia exported 7.616 million tonnes of sawn timber. That is 3.4% more than during the respective period of the last year.

The total value of the exported Russian sawn timber increased as well. In January-May it came up to $1.805 billion having gone up by 17.8%.

In their turn, Russian log exports went down in volume terms, but increased in value terms.

In January-May 2018, the Russian log exports came up to 7.313 million m3, having gone down by 6.2% year-on-year.

The total value of the Russian logs exported in January-May 2018 came up to $636 million, that is 5.9% more than during the respective period of 2017.

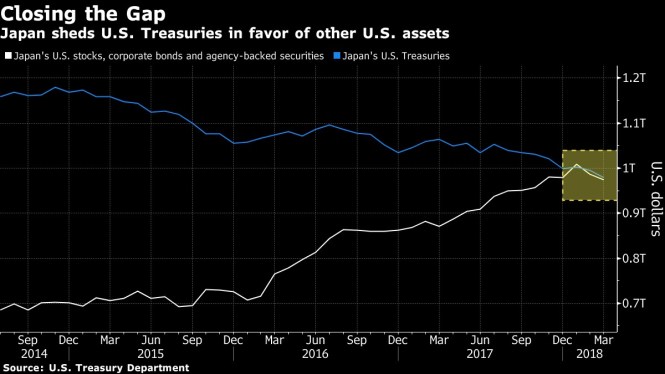

A “slow-mo” credit crunch has already taken hold, says HSBC.

Japan is reaching for yield in the U.S.

The nascent return of India’s biggest bond buyers

Moody’s survey shows oil prices as the main risk to India’s economy

Mumbai, July 04, 2018 22:52 IST

A | Photo Credit: K_Pichumani

Mumbai, July 04, 2018 22:52 IST

Interest rates, politics too seen as risks

Oil prices, pace of banks’ balance sheet clean-up and investment remain the key credit risks in India, according to an investor survey by Moody’s Investors Service.

While market participants in Singapore and Mumbai were unanimous in pegging high crude price as the main risk to India’s economy, views varied on the second biggest risk, according to the ratings agency.

“When asked about the top risks facing the Indian economy, most of the respondents highlighted high oil prices as the top risk, while 30.3% of those in Singapore picked rising interest rates as the next top risk, and 23.1% of those in Mumbai picked domestic political risks as the second top risk,” Joy Rankothge, a vice president and senior analyst at Moody’s, said in a press release.

Participants at Moody’s 4th Annual India Credit Conference, conducted by the credit ratings agency along with its Indian affiliate ICRA Ltd. in Mumbai and Singapore in June 2018, were polled on some of the most pressing credit issues facing India.

Almost 175 people representing more than 100 local and international financial institutions attended the conference, Moody’s said.

Fiscal slippage seen

Most attendees at both locations opined that India would not meet the central government’s fiscal deficit target of 3.3% of GDP for the financial year ending in March 2019, according to the release.

Further, only 23.3% of the respondents in Singapore and 13.6% in Mumbai thought that the fiscal targets would be achieved, with 84.7% in Mumbai and 76.7% in Singapore expecting some fiscal slippage.

Those polled in both Singapore (85.7%) and Mumbai (93.6%) believed the government’s bank recapitalization package was mostly insufficient to resolve solvency challenges.

‘Capital insufficient’

“Although we expect the recapitalization package to be sufficient to meet the minimum regulatory capital needs, we think it will be insufficient to support credit growth,” Moody’s said in a report. “Banks have not been able to raise new capital from the equity markets as planned under the government’s recapitalization measures,” it said.

Incidentally, while 59.6% of the attendees in Mumbai thought that banks would be unable to raise capital from the markets as planned, only 32.1% of those polled in Singapore held that view, Moody’s said.

(Shutterstock)

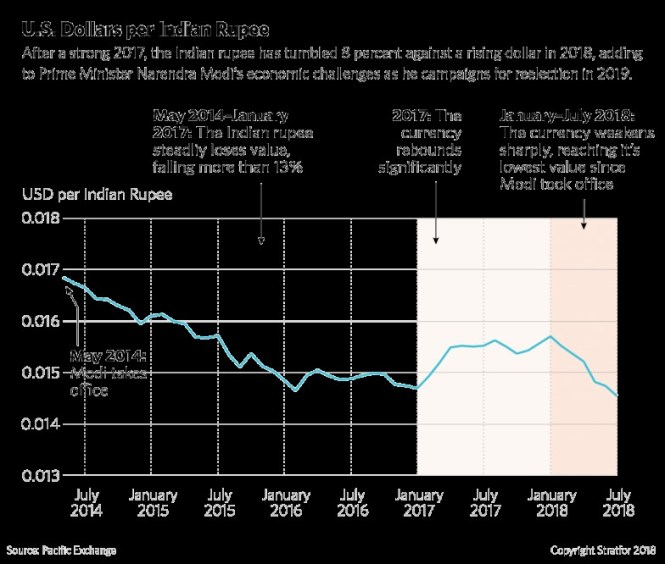

What the Falling Rupee Means for India’s Economy

https://worldview.stratfor.com/themes/indias-own-worst-enemy

Highlights

- A strengthening U.S. dollar is causing the rupee to depreciate as the cost of India’s hefty, dollar-denominated oil imports are rising.

- The falling rupee suggests that Indian monetary policy will enter a tightening phase to stem debt outflows, manage inflation and ease the currency’s fall in the world’s fastest-growing economy.

- With an eye on re-election in 2019, Prime Minister Narendra Modi will continue to indulge in populist spending, which will expand the country’s deficit and slow the government’s fiscal consolidation drive.

- While economic trends in India will weaken Modi as a candidate, the absence of a unified opposition indicates that he will remain the favorite in the 2019 general elections.

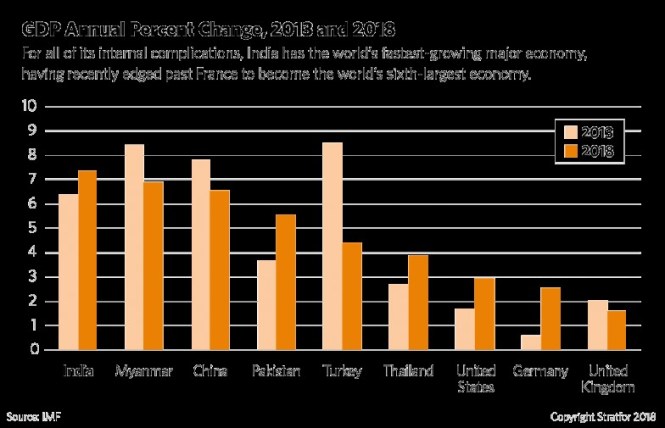

With a gross domestic product of $2.6 trillion, India recently eclipsed France to become the world’s sixth-largest economy. What’s more, the South Asian country of nearly 1.3 billion people is home to the world’s fastest-growing economy, having edged out China with its 7.7 percent growth rate from January through March. While these figures are impressive, they rest uncomfortably alongside less sanguine facets of India’s macroeconomic picture.

The Big Picture

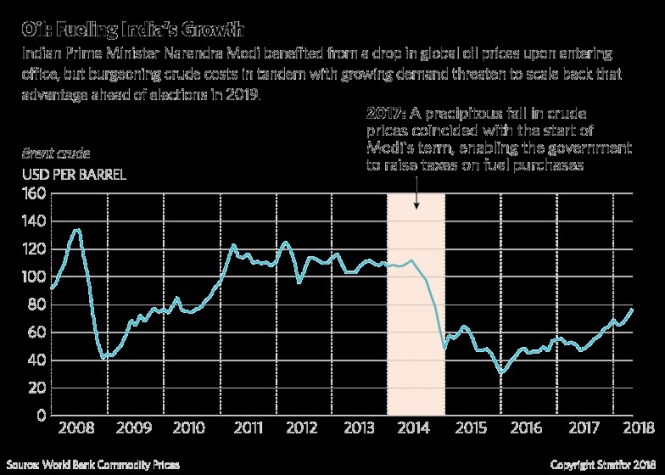

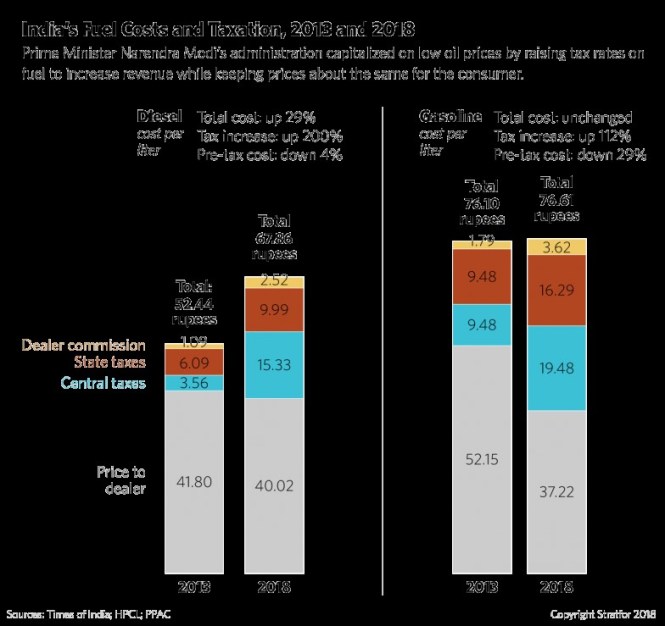

Indian Prime Minister Narendra Modi will seek another five-year term in 2019 to try to advance the land, labor and tax reforms that he argues are necessary to produce the job growth needed to absorb the 12 million Indians who enter the labor market each year. But a weakening rupee, rising oil prices and other external vulnerabilities point to the challenges ahead for Modi as he campaigns for re-election.

Ongoing shifts in U.S. monetary policy are causing India’s rupee to depreciate against the dollar. As the U.S. Federal Reserve cautiously raises interest rates to keep inflation in check — in June, the U.S. consumer price index hit its highest level since 2012 — the U.S. Treasury has increased its issuance of bonds to cover large deficits resulting from recent U.S. tax cuts. Together, these U.S. decisions have put additional pressure on the rupee, which has tumbled more than 8 percent against the rising dollar in 2018. This decline makes the rupee Asia’s worst-performing currency this year (though India’s real effective exchange rate — a measure of the rupee’s value in relation to trading partner currencies — is down only 3.5 percent since December)

India’s $409 billion in foreign exchange reserves enable it to weather any currency shocks, giving the Reserve Bank of India the ability to intervene by quietly selling dollars to pull rupees out of circulation and thereby boost their value. But broadly speaking, the rupee’s performance against the dollar in tandem with rising oil prices will increase India’s import bill, lead to debt outflows and compel the Reserve Bank to embark on its own phase of monetary tightening while Prime Minister Narendra Modi’s populist spending in support of his 2019 re-election bid is expanding the country’s fiscal deficit.