October 17th 2018

EIU global forecast – Trade war will disrupt supply chains

The Economist Intelligence Unit expects the global system to be characterized by competition between the major powers in the next five years. Of most importance to the global economy is the relationship between the world’s two largest economies, China and the US. The bilateral trade war between these countries will drag down global economic growth in 2019, as well as disrupt global supply chains. However, the trade dispute is increasingly spilling into areas of political and security concern. On October 4th the US vice-president, Mike Pence, signaled a significant hardening of US strategy towards China. The most explosive allegation from Mr. Pence’s speech was that China was meddling in US politics ahead of the mid-term elections in November. However, the speech also addressed several larger issues, including the controversy over the “Made in China 2025” initiative, the debt issues surrounding China’s Belt and Road Initiative and the campaign against Taiwan. In a clear signal of US intent, the revised North American Free-Trade Agreement, officially re-branded as the United States Mexico Canada Agreement (USMCA), contains an anti-China provision aimed at increasing the trade pressure on the country. The USMCA casts a spectre over potential future trade deals between China, Canada and Mexico by stipulating that any party would have grounds to withdraw from the deal if another party were to enter into a free-trade agreement with a non-market economy (a term used by the US to describe China).

Signs of renewed tensions over Taiwan are of concern, given the island’s key strategic significance for China. On September 25th Geng Shuang, a spokesman for China’s Ministry of Foreign Affairs, told a press briefing that China had lodged a complaint against the US regarding the approval of a US$330 million arms sale to Taiwan, announced the previous day. This followed a statement on September 7th by the US Department of State that it had recalled its ambassadors to El Salvador, Panama and the Dominican Republic following the decision by those countries to no longer formally recognise Taiwan. All three countries switched diplomatic recognition from Taiwan to China in 2018. We expect that nationalist sentiment is also likely to increase in Asia, given our view that the trade war is likely to endure until at least 2020. For China, reunification has long been designated a core national issue, and Xi Jinping, China’s president, may also view Taiwan as a legacy issue for his presidency. Moreover, if Mr Xi has concerns about China’s medium-term growth prospects, owing to issues such as an ageing population and unsustainable debt, he may be tempted to address these sooner rather than later. Consequently, risks are developing around the question of Taiwan, suggesting that the likelihood of conflict erupting at some point in the next five years is higher than it has been in decades.

The world’s other major power, Russia, is also expanding its global presence, presenting a challenge to the US’s dominance of global security. During a recent visit to India by the Russian president, Vladimir Putin, Russia signed a US$5.4 billion deal for the sale of S‑400 Russian air defense missile systems to India. The deal is in line with our view that Russia will strive to be on the same level as the US in terms of its economic and security relationships, a process that risks increasing tensions in the region. Other flash points also present a significant risk to the global economy, and, with the lack of co‑operation between the US, China and Russia, diplomatic options to resolve tensions look remote. North Korea continues to be a threat to global stability, despite the country’s current rapprochement with the US. A breakdown in talks is possible, as differences remain over the terms of denuclearization, and, with US‑China relations deteriorating, China is unlikely to give full support to the US’s engagement with North Korea. A return to heated rhetoric between the US and North Korea is possible, which would be of particular concern since the room for diplomatic maneuver is limited. In the Middle East, a conflict between Iran and Israel is a medium-term risk. The two countries are involved in a proxy conflict in Syria, but a direct confrontation would further destabilize the region. The source of this risk is Iran’s decision to consider restarting its nuclear program in the coming years, owing to the collapse of the Iran nuclear deal with the US. If the program were to be restarted, a direct attack on Iran by Israel would be a possibility.

Set against this backdrop of geopolitical shifts are the trends of declining democracy and authoritarian regimes. According to our 2017 Democracy Index, 89 out of 167 countries saw a decline in their democracy scores, and about one‑third of the world’s population lives under authoritarian rule. Following the decision by Mr. Xi to abolish presidential term limits, authoritarian rule is set to endure in China. Russia is also an authoritarian regime under Mr. Putin’s rule. Examples of authoritarian-leaning, strongman leadership also exist in Hungary, the Philippines, Turkey and Saudi Arabia. Brazil could join this group if Jair Bolsonaro wins the second-round presidential election against his opponent, Fernando Haddad. Given this picture, we expect a growing number of economic and diplomatic disputes, and although we do not expect a major power conflict to occur, businesses should be cautious of bilateral tensions escalating to a breakdown of relations between countries.

The US-China trade war will escalate and endure

The US president, Donald Trump, has moved ahead with tariff increases on a further US$200 billion-worth of Chinese imports. China responded with additional tariffs on US$60 billion-worth of US imports. The trade dispute is likely to escalate further, and we now expect the Trump administration to move ahead with tariffs on most of the remaining Chinese imports that have yet to be covered in the dispute. At the heart of the dispute between China and the US is a disagreement over intellectual property and China’s technology transfer practices, although the US trade team is divided on this issue, with Mr. Trump also focusing on the US’s trade deficit with China. Given this, discussions thus far between the two countries have failed to resolve the dispute, and a resolution looks unlikely in the short term. By 2019 this will dampen growth in both economies and act as a drag on growth in the wider global economy. We expect that, combined with softening economic growth in key emerging markets, especially those in Latin America, global growth will slow to 2.7% at market exchange rates in 2019, from 3% in 2018.

Growth in the US and China will slow more than expected in 2019

The trade war comes at a challenging time for the Chinese economy. Concerns over the strength of domestic demand have returned as momentum in both private consumption and investment has weakened. The effects of tighter monetary policy, corporate deleveraging efforts and a crackdown on shadow financing have become more apparent in the economy this year, having raised the cost and availability of capital for both firms and consumers. The trade war will lessen the focus on deleveraging, with authorities needing to take measures to support growth in the short term. We are likely to see a moderate easing in fiscal policy, such as cuts to taxes and fees, together with an easing of reserve requirements from the People’s Bank of China (the central bank). There is recognition from policymakers, however, that capacity to support the economy will be limited by China’s debt profile. On the back of these assumptions, in July we revised down China’s growth forecast for 2019 to 6.2%, from 6.4%. Although we expect growth to be maintained to reach the government’s target of doubling real GDP this decade, the trade war has again raised the spectre of China’s financial vulnerabilities, which will cloud the economy’s outlook for the foreseeable future.

The trade war will also affect the US economy, which has so far had a stellar year in 2018. We have revised up our forecast for real GDP growth in 2018 to 2.9% (from 2.8%), to reflect faster than anticipated growth in the second quarter, of 4.1% in annualized terms, and heightened expectations of a similar rate of growth in the third quarter. The economy continues to receive support from the Trump administration’s fiscal policies, as well as from the ongoing strength in the labor market. However, the escalating trade dispute with China will start to weigh on growth later in 2018 and into 2019—we expect growth to slow in 2019 to 2.2%. The US manufacturing and agricultural sectors will be hit by the trade dispute, and rising interest rates will cause private consumption to slow. Growth will continue to slow in 2020, to a low of 1.3%, as the lingering effects of the trade dispute, higher interest rates and softening corporate balance sheets result in a business-cycle slowdown. A mild recovery will take place in 2021‑23 as these effects unwind, with growth averaging 1.9%.

Financial market volatility will remain high in 2019-20

The US-China trade war and growing geopolitical tensions will add to the risks facing emerging markets. Volatility in emerging-market currencies in recent months has fueled fears of a full-blown crisis. Capital flight has so far led to genuine currency crises in Turkey and Argentina, and we expect recessions in both. The Argentinian and Turkish crises have intensified the sell-off in emerging-market assets, which began in April because of the strengthening US dollar. Further periods of market volatility are likely as several key trends—tightening monetary conditions, the global trade dispute, heightened geopolitical risk and, in many emerging markets, a significant increase in debt levels in recent years—interact in challenging ways. Turkey and Argentina have experienced a perfect storm of external imbalances, namely weak monetary policy credibility and political risk, which few other economies currently share. As a result, we expect future exchange-rate crises to remain confined to the most vulnerable countries, with non-Organization for Economic Cooperation and Development (OECD) economic growth remaining steady in 2019‑20. However, there is a moderate risk (21‑30% probability) that a souring of market sentiment towards emerging markets as an asset class could lead to a noticeable slowdown in emerging-market growth in 2019‑20.

Our forecasts crucially assume that US monetary tightening will remain controlled and relatively gradual in 2019‑20, with inflation picking up only modestly. However, there remains a risk that US inflation and interest rates could rise faster than the rate that is currently built into financial market pricing, leading to falls in a wide range of asset prices that have been supported by years of extraordinary monetary policy support. Financial markets could also prove more sensitive to rises in interest rates than we currently assume. By keeping long-term interest rates extremely low through quantitative easing programs, major central banks have forced investors to look elsewhere for attractive returns, pushing up the prices of bonds, stocks and property. The effects on financial markets of withdrawing huge amounts of monetary stimulus are not well understood. The sharp sell-off in global share markets in October, amid rising US bond yields, shows the fragility of financial market sentiment. We have raised from low to moderate the likelihood of a sharp global slowdown brought about by a faster than expected increase in US interest rates.

Nov 27, 2018 | 13:49 GMT

Asia-Pacific

The Asia-Pacific is home to more people than any other region. Centered on the western rim of the Pacific Ocean, this region includes the easternmost countries of continental Asia as well as the archipelagos that punctuate the coast. Several of these countries, most notably China, experienced rapid economic growth in the second half of the 20th century, giving the region a new sense of global economic relevance that continues today. That relevance, however, depends largely on China, a power in transition whose rise is testing the network of U.S. alliances that have long dominated the region. How effectively Beijing manages its transition will shape the regional balance of power in the decades to come. Read the Synopsis

(Thoyod Pisanu/Shutterstock.com)

Table of Contents

- Global Trends

- Middle East and North Africa

- Asia-Pacific

- Europe

- South Asia

- Eurasia

- Americas

- Sub-Saharan Africa

Key Trends for 2019

China Weathers the Trade Storm

Beijing will try to keep its lines of communication with Washington open on trade by offering to buy more U.S. goods and selectively lower barriers to investment, but its concessions won’t meet U.S. demands for structural economic reform. Still, China will only respond in kind to U.S. measures targeting Chinese firms and entities and not take any blanket punitive action against U.S. businesses. Beijing will also deepen public-sector reforms by soliciting foreign investment for its financial, auto and energy sectors. Furthermore, it will ease restrictions in sectors that align with China’s prime interests, such as medical services and education.

China’s refusal to concede to U.S. demands will prolong the ongoing trade dispute.

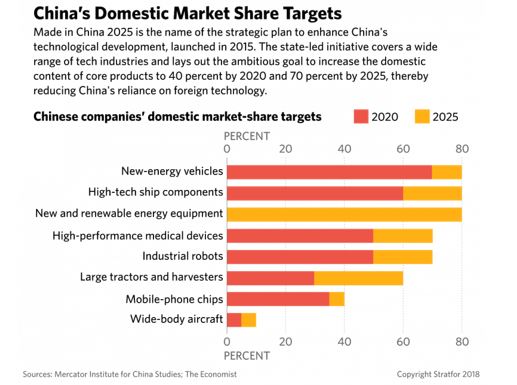

The United States will maintain its demand that China ease state support for its tech sector, but that will only compel Beijing to accelerate its efforts to ease China’s dependence on foreign technology and diversify its supply chain — thereby necessitating increased state support for the sector. China’s refusal to bow to U.S. pressure on tech will prolong their trade dispute. At the same time, China will strive to acquire technology and cooperate on sector-specific activities with advanced tech powers like Japan, Israel, Taiwan and the European Union, but such activities will face increased scrutiny over concerns about Chinese investment and industrial espionage. Read more on China’s efforts to reform its state sector.

Beijing Battens Down the Hatches

Because the extended trade war threatens the economy in China’s coastal regions (and, thus, social stability), Beijing will ease its tight regulations designed to contain debt and protect the environment while upgrading infrastructure, generating credit and offering direct subsidies to boost growth. China will also carefully manage the yuan’s value to mitigate the damage to exports, allowing it to cope with reduced growth. But an accumulation of debt and the fragility of the housing market will limit Beijing’s ability to use massive credit flows and sharp currency devaluations as a means of economic stimulus.

China will have to rely more on fiscal stimulus — including reducing taxes — to encourage consumption and private sector activity.

It will also encourage the increased use of the yuan in currency swaps and in trade with countries participating in the Belt and Road Initiative to mitigate currency volatility. And to keep hedging against U.S. trade pressure, Beijing will pursue bilateral and regional free trade agreements, such as the Regional Comprehensive Economic Partnership in the Indo-Pacific region and trilateral negotiations with Japan and South Korea, all while forging ties with new export markets along the Belt and Road and in Africa. Southeast Asia’s emerging economies, meanwhile, will be ready to lure any factories that relocate from China amid the trade war. Threats to the overall regional supply chain and external financial volatility could also present challenges to countries with higher debt or current account deficits, such as Malaysia, Indonesia and the Philippines. Learn more about why state-owned enterprises are so important to China.

Great Power Competition in the Asia-Pacific

As it tries to chip away at the U.S. regional alliance structure, China will continue its conciliatory outreach to Japan, India and the member states of the Association of Southeast Asian Nations (ASEAN) by privileging dispute resolution efforts and economic partnerships while also making overtures to Australia, whose April elections could foster some rapprochement. At the same time, Washington will bolster its naval presence in the South China Sea and the Taiwan Strait and further challenge the One China principle by elevating Taipei’s status at international associations and regularizing arms sales, naval patrols and high-level visits.

The U.S. Navy will be more prevalent in the South China Sea and the Taiwan Strait, which will provoke China to adopt a more robust military posture.

In response, China will adopt tougher naval and aerial postures to assert its territorial claims, increasing the chances of accidents involving the U.S. military. The United States is considering making a naval port call in Taiwan — an event that would trigger a more direct Chinese military response. Japan, India and Australia will increase security cooperation with Washington, but they will refrain from joining U.S. freedom of navigation operations in the South China Sea or patrols in the Taiwan Strait. Elsewhere in the region, U.S.-ASEAN military exercises and U.S.-Vietnamese defense cooperation will complicate Chinese efforts to limit the further regional expansion of U.S. influence. Find out more about Taiwan’s role in U.S.-China competition.

A Fraying Consensus on North Korea

The United States is intent on extracting tangible concessions from North Korea in 2019. But this is also the year that Pyongyang hopes to squeeze the most out of the Trump presidency before the United States becomes distracted by its election cycle. Given the obviously high stakes of open warfare, neither will deliberately scuttle the dialogue. North Korea will carefully offer tangible pledges but will also expect concrete progress on sanctions relief or toward a peace deal; throughout the process, it will obfuscate and delay where it can. Pyongyang will also insist on assurances that any bilateral deal will have staying power beyond the current administration.

The United States will hesitate to extend an economic lifeline to North Korea by lifting sanctions, but time is on Pyongyang’s side as the international consensus on maintaining sanctions unravels.

For the moment, Washington’s veto power on the U.N. Security Council will allow it to block any effort to repeal the multilateral measures, even as China and Russia push for the international community to reward North Korea for its cooperation. At the same time, the United States will pressure others to fall into line on sanctions by shaming transgressors and threatening secondary sanctions against those who deal with Pyongyang. Complicating matters, inter-Korean detente is reaching the point where it cannot proceed much further without sanctions exceptions — something the United States will only approve after careful consideration. The growing discrepancy between the pace of the inter-Korean dialogue and the pace of the U.S.-North Korean discussions will leave room for China to extend its influence on the Korean Peninsula. Overall, while swings towards breakthroughs and breakdowns will occur throughout the year, North Korea will still maintain possession of many elements of its hard-won nuclear program at the end of 2019.

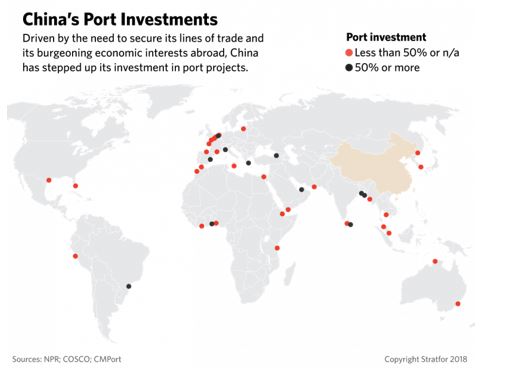

Moving the Belt and Road Forward

With its access to U.S. markets under strain, Beijing will redouble its efforts to find new export markets and partners through the Belt and Road Initiative. Washington will work principally with Japan and Australia to offer alternative infrastructure investments to counter China’s ambitions in the Indo-Pacific, but Beijing will temper potential partners’ concerns regarding financial sustainability, political influence and national security threats by attracting third-party investors. It will also work to undermine Washington’s regional initiatives by pursuing joint projects with middle powers, including Japan, the European Union and India. Take a more in-depth look at the resistance to the Belt and Road Initiative.

A Japanese Awakening

Secure in his position through 2021, Japanese Prime Minister Shinzo Abe will aim to pass constitutional reforms before the end of 2019 while offsetting the economic impacts of a consumption tax hike through public works spending, incentives for private sector investment and tax exemptions for certain products. And though Russia and Japan will continue to negotiate over the disputed Kuril Islands, a larger standoff between Moscow and the West will scuttle any hopes of a deal.

When it comes to trade, the United States and Japan have an arrangement for now, but much will depend on how far Washington pushes Tokyo.

Meanwhile, Tokyo will grant concessions that will partly placate U.S. trade concerns — so long as the U.S. push for agricultural access does not exceed the limits outlined in the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) and EU-Japan trade deals. If Washington pushes further, Tokyo will experience a backlash from its powerful farming lobby — although it will weigh whether to sacrifice its agricultural sector to avoid U.S. tariffs on its critical auto sector. Beyond that, Tokyo will also resist U.S. attempts to limit any future Japanese trade deal with China. Read more on Japan’s calculations on automotive and agricultural trade in the face of U.S. pressure

Related Forecasts

These Stratfor analyses provide additional insights for the year ahead

- The U.S.-China trade war could benefit Vietnam economically but will complicate Hanoi’s delicate balance between the two.

- China’s large debt accumulation will hamper Beijing’s efforts to stimulate the economy.

- China’s tech sector will become an increasing concern for the United States, particularly as the two battle over artificial intelligence.

Key Dates to Watch

- Early 2019: Release of a World Trade Organization panel report on China’s challenge of the European Union’s refusal to grant China market economy status.

- Early 2019: Next Trump-Kim summit may occur.

- Jan. 1: Date that the United States could possibly raise the tariff rate on $200 billion worth of Chinese imports to 25 percent.

- Jan. 14: First day the United States can hold formal trade deal talks with Japan.

- January: First round of CPTPP’s tariff cuts will take effect.

- March: Joint U.S.-South Korean military exercises Foal Eagle, Double Dragon and Key Resolve normally held.

- May 18: Australia’s Senate elections must be held before this date, with House of Representative elections due by November.

- June 28-29: A G-20 summit is scheduled to be held in Osaka, Japan.

August: U.S.-South Korean Ulchi Freedom Guardian military exercise normally held.

Emerging middle class promises bumper payday for asset managers Growth will come from harnessing demand for financial products as demographics shift

Chris Flood DECEMBER 2, 2018

Many asset managers describe their businesses as global because they invest in financial markets across the world. Yet not one has succeeded in building a truly global client base that can rival those of leading technology companies such as Google and Amazon. Building a client base in emerging markets requires international investment managers to confront myriad legal and regulatory obstacles that can pose a threat to expansion plans. Yet the prize for doing so is potentially huge.

The growing size and prosperity of the middle classes across many emerging markets offers a tantalizing reward to those managers that can address the needs of institutional clients and retail investors in these countries. “The investment industry is a natural beneficiary of the growth in wealth and savings among the middle classes in emerging markets,” says Kunal Desai, a portfolio manager with Mobius Capital, a London-based specialist emerging market boutique. “But it tends to get overlooked in favour of sectors that are seen as more obvious winners, such as consumer goods.” Investor assets managed in the Asia-Pacific, Latin America, Middle East and Africa regions will increase from about $16.1 trillion at the end of 2016 to $38.5 trillion by 2025, according to PricewaterhouseCoopers (PwC), a professional services provider.

Olwyn Alexander, a partner at PwC, says profiting from this rise requires cultural change. “Historically, there has been a lack of an investment culture in many emerging markets,” she says. “But even a small shift can present significant opportunities given the magnitude of the populations in some of these countries.” $420 billion New money expected to flow into the fund industry in India over the next decade Asset managers need to ensure they can cater to younger investors, Ms. Alexander says. “Asset managers will need technology capabilities to process large numbers of small dollar value transactions from mobile devices,” she adds. Among the fastest-growing managers in Asia, local and international, two common traits stand out. All are making big bets on China and have invested in new digital services to attract the growing middle class’s rising wealth.

A successful marriage between technology and asset management is exemplified by Yu’E Bao, a fund created as a repository for leftover cash from consumers’ online spending accounts by the Chinese company Ant Financial in 2013. Yu’E Bao has grown into the world’s largest money market fund with more than 400 million users. “The big fin techs are aiding China’s shift to a cashless society,” says Jacob Dahl, a senior partner at McKinsey, based in Hong Kong. “How asset managers position themselves to serve these digital platforms will be critical, not only in China but also in other Asian markets where fin techs are gaining ground.” China, which is on course to replace Europe as the world’s second-largest fund market behind the US, provides the single largest growth opportunity for global asset managers over the next decade. The country’s mutual fund assets could multiply five-fold to reach $7.5 trillion by 2025, creating a fee pool worth $42 billion a year, according to UBS. “But it all depends on the progression of reform and deregulation,” says Kelvin Chu, an analyst with UBS.

In India, a decade of consistently strong economic growth has helped to accelerate the rise of the middle class. The National Council of Applied Economic Research, a Delhi-based think-tank, has forecast that this group will number 547 million people by 2026, from 267 million in 2016.

India’s middle class is expected to double to 550 million by 2026 © Alamy

India’s government has implemented a series of reforms that have significantly boosted inflows into fund management. “We estimate that around $420 billion in new money from domestic investors will flow into the fund industry in India over the next decade,” Mr. Desai says. “This compared with around $180 billion from both domestic and international sources over the past 10 years.”

Managers should be careful not to overlook Indonesia, Malaysia and Thailand, Mr. Dahl says. “We expect assets under management in these markets to nearly double over the next five years from a collective $600 billion today,” he says.

Across Asia as a whole, close to 90 per cent of financial assets sit outside the control of asset managers, with the industry overseeing a far lower share than in Europe or the US, according to McKinsey.

However, rising numbers of billionaires in Asian countries, the further growth of large government-sponsored sovereign wealth funds and the development of private pension systems to meet the needs of rising numbers of savers should all provide new sources of growth. “The Asia asset management revenue [fee] pool stands at around $66 billion today and we expect this to [reach] $112 billion by 2022,” says Mr. Dahl.

China Economic Update

By Eric Wong

Managing Director, Canada Wood China

October 31, 2018

China to Reduce Wood Import Tariffs November 1

2018 Q3 highlights:

- China’s GDP hit the lowest growth in September (6.5%) since the first quarter of 2009 during the global financial crisis and missed market consensus of 6.6%.i

- China Economic growth slowed down in the third quarter due to:

- to a decrease in infrastructure investment

- a negative spillover from financial deleveraging

- the impact of previous economic reforms

- a cooling housing market.

- However, export growth continued to grow strongly in Q3 in spite of trade tension with the U.S.ii

- A recent government announcement effective November 1st, 2018 states that China will cut import tariffs on more than 1,500 products to lower the average import tariff to around 7.8%. Import tariffs on wood and paper products will be decreased to 5.4% from 6.6% which will help wood-based panels and other related imports to grow in China.iii

PMI (Caixin) index in September (50.0) dropped to a 16-month low and missed market consensus of 50.5 which was also the lowest point of the continuously descending trend started from May (51.1).iv China Exports achieved a 14.5% gain year-on-year to USD 226.7 million in September which was the fastest growth in outbound shipments since this February and also beat market consensus of 8.9%.v

China Consumer Price Index (CPI) started to go up from May (101.8) to September (102.5) which achieved the second highest month only after February (102.9).vi Similar to Q2, USD/CNY had also been on the rise in Q3, increased from 6.62 (July 1st) to 6.81 (August 1st) to 6.83 on September 1st;vii CAD/CNY kept the similar upward trend, went from 5.04 (July 1st) to 5.23 (August 1st) and hit 5.24 on September 1st.viii

Building material prices

Cement price increased slightly from RMB 435.67 to RMB 456.00 per metric ton (up 4.67%) over September 2018.ix Rebar steel price also went up slightly by 2.63% from RMB 4,415.38 per metric ton on September 1st 2018 to RMB 4,531.54 per metric ton on September 30th 2018.x The log price index in September 2018 was 1,096.96 points which decreased 0.26% less than August 2019 and reduced 0.84% compared to the same period year-on-year; the lumber price index in September 2018 was 771.05 points which went up slightly by 0.02% month-on-month and increased 0.36% year-on-year.xi

China-US Trade Dispute Update xii

The trade war between China and United States continues to impact markets.

During the first half of 2018 U.S. wood products made up:

- 13% of China’s softwood log imports; was 54% in 2017

- 2% of China’s softwood lumber imports; was 38% in 2017

- 7% of China’s hardwood log imports;

- 21% of China’s hardwood lumber imports.

China Wood Imports xiii

Russian softwood lumber imports have been rising steadily since this February when imports hit the highest in May (1,590,000 m3) and maintained at the level of 1,500,000 m3 in August; Canadian softwood lumber imports on the other hand maintained 350,000 m3 each month from June to August but decreased 29% in August to (327,000 m3) compared to the same month last year.

Logs and lumber inventory at Taicang, Wanfang and Meijing ports hit a new low in August (802,000 m3) which decreased consistently since this March, but winter and Chinese

New Year inventory volume at all ports will be on the rise based on previous trends. Import volumes of total logs and lumber fluctuated at reasonable curves and achieved 8,814,000 m3 in August, the second highest month so far in 2018.

China softwood lumber

i Trading Economics (October 20th, 2018). China GDP Annual Growth Rate

ii Focus Economics (October 16th, 2018). China Economic Outlook

iii Wood Markets/FEA (October 2018). China Bulletin

iv Trading Economics (October 20th, 2018). China Caixin Manufacturing PMI

v Trading Economics (October 20th, 2018). China Exports

vi Trading Economics (October 20th, 2018). China Consumer Price Index (CPI)

vii XE Currency Charts: USD to CNY

viii XE Currency Charts: CAD to CNY

ix Sunsirs (October 2018). Spot Price for Cement

x Sunsirs (October 2018). Spot Price for Rebar Steel

xi BOABC (October 2018). China Wood and Its Products Market Monthly Report

xii Wood Markets/FEA (October 2018). China Bulletin

xiii Wood Markets/FEA (October 2018). China Bulletin

Who will benefit from the American timber tariff?

By Dora Xue

October 31, 2018

China announced a 25% tariff on U.S. imports, on a value of $16 billion from August 23rd. The taxed products include $1.83 billion of wood products and logs.

A large range of wood products are listed in the tariff list, including oak logs, birch logs, OSB, spruce, larch, teak, wooden window frames, shelves, furniture etc.

China is the biggest importer for American wood products. The United States exported 6.14 million m3 logs to China, accounting for 53.9% of U.S. logs, and 3.27 m3 lumber, accounting for 38% of U.S. sawn timber exports, according to the U.S Bureau of Statistics. The China market represents half of total U.S. log exports, and one third of its sawn timber exports.

The U.S. tariffs will increase the cost of U.S. wood imports, which will make America timber gradually lose its competitiveness and market position in China.

As forecasted by China Timber Website, Chinese buyers may turn to other countries such as Russia and Europe as the properties of timber from those countries are very similar to that of the U.S.

Korean Technical Mission Ends in Success

By Tai Jeong

Technical Director, Canada Wood Korea

October 31, 2018

Posted in: Korea

Canada Wood Korea has successfully completed its annual Technical Mission, visiting Canada and Japan from September 26 to October 7 with participation of 13 WFC industry leaders including renowned architects, structural engineers and prefab manufacturers and 1 media reporter.

Mission participants attended technical seminars both at FPInnovations and Canada Wood Japan office to learn about technical aspects and commercialization of the Midply Shearwall system, industrialization plants and various buildings sites both in Canada (British Columbia and Alberta provinces) and Japan to learn about innovative industrialized WFC systems including pre-fabrication, modular homes and tall wood mass timber construction.

All participants said It was a wonderful opportunity to experience actual applications of wood along with technical seminars. Especially, Mr. Je Yu Park, President-elect of the Korean Institute of Architects (KIA) who participated in the mission, agreed to sign an MOU with Canada Wood for technical cooperation and jointly hold the WFC Seismic Workshop for member architects in conjunction with the Forest Sector Mission to Korea led by the Minister Doug Donaldson this coming December 2018. Mr. Park also promised to establish a Wood Structure Design Advisory Committee Division at KIA after his inauguration next year.

Canada Wood Korea signs agreement with Korean Institute of Architects

JOC News Service December 17, 2018

VANCOUVER — Canada Wood Korea and the Korean Institute of Architects have signed a memorandum of understanding (MOU) to help Korean architects work better with Canadian wood.

The technical co-operation agreement was signed on Dec. 7 by senior forest industry representatives on the Forestry Asia Trade Mission, which consisted of a group of more than 40 delegates including industry, research, labour, First Nations and government.

The group also visited the Gapyeong Canada Village Project on Dec. 8., which uses wood products from B.C. and other parts of Canada. The village is the result of a 2013 MOU signed by Canada Wood Korea, the Gyeonggi Urban Innovation Corporation and Dreamsite Korea.

“South Koreans’ interest in wood construction is growing because they recognize that wood construction fares better than other materials in the event of earthquakes. By promoting the benefits of wood and sharing technical expertise, we can open up new opportunities in Korea for our province’s high-quality wood products. This, in turn, supports forestry jobs in B.C.,” said B.C. Minister of Forests, Lands, Natural Resource Operations and Rural Development Doug Donaldson in a statement.

The MOU is intended to raise the skill and knowledge levels of Korean architects and designers so they are better equipped to work with wood. The Institute will benchmark Canadian best practices for wood-frame residential housing, wood interior walls and Super-E/Net-Zero housing design, a standard designed by Natural Resources Canada where a home produces all needed energy from renewable sources and releases no carbon from the burning of fossil fuels.

South Korea is B.C.’s fifth-largest market for wood products, with softwood lumber exports totaling over $73 million in 2017.

Korea – Economic forecast summary (November 2018)

READ full country note (PDF)

Economic growth is projected to remain close to 3% through 2020, as fiscal stimulus offsets sluggish employment growth, which reflects double-digit hikes in the minimum wage in 2018-19 and restructuring in the manufacturing sector. Measures to stabilize the housing market have led to a decline in construction orders for residential property. Inflation is expected to edge up from 1½ per cent toward the 2% target, while the current account surplus will remain above 5% of GDP.

Hikes in the minimum wage should be moderated to avoid negative effects on employment. The “income-led growth” strategy, driven by minimum wage increases and higher public employment and social spending, needs to be supported by reforms to narrow productivity gaps between manufacturing and services, and between large and small firms. Short-term fiscal stimulus should be accompanied by a long-term framework to cope with population ageing, which will be the fastest in the OECD. With inflation below target, the withdrawal of monetary accommodation should be gradual.

Korea

http://dx.doi.org/10.1787/888933876974

Supportive macroeconomic policies should be accompanied by structural reforms The government is responding to weaker domestic demand with fiscal stimulus. Spending is to increase by 9.7% in 2019, the highest since 2009 in the wake of the global recession. Social welfare spending is the priority, along with outlays for job creation, which are set to rise by 22%. In addition, the government aims to boost public employment by 34% over 2017-22. Despite increased spending, the general government budget will remain in surplus at around 2% of GDP in 2019, while government debt is low at just under 45% of GDP. The policy interest rate has remained at 1.5% since late 2017. With consumer price inflation below 2%, the normalization of monetary policy should be gradual. Monetary policy also needs to consider potential risks to financial stability, including capital flows and household debt, which rose at an 8% pace in the first half of 2018. At 186% of net disposable household income in 2017, household debt remains a headwind to private consumption. Raising labour productivity, which is 46% below that in the top half of OECD countries, is increasingly important for growth as the working-age population peaked in 2017. The priority is regulatory reform, focusing on services, where labour productivity is less than half of that in Korean manufacturing. Policies to promote entrepreneurship and raise productivity in SMEs are also needed to promote inclusive growth. Increasing female employment and reducing the gender wage gap, which is the highest in the OECD at 37%, is another priority. Growth is projected to be stable Output growth is projected to remain close to 3%, despite sluggish employment growth in 2019, partly as a result of a hike in the minimum wage by a further 10.9%. Further large increases, as part of the government’s commitment to a sharp increase in the minimum wage, would damp employment and output growth. The improved relationship with North Korea is a landmark event that may also have positive economic implications. Moreover, progress with structural reforms to raise productivity in lagging sectors would boost output growth. However, trade protectionism remains a concern: with intermediate goods accounting for four-fifths of Korea’s exports to China, its largest trading partner, Korea is vulnerable to higher import barriers on Chinese exports to the United States.

Taiwan exports end 24-month rise

U.S.-China trade war played part in sudden drop: MOF

By Matthew Strong,Taiwan News, Staff Writer

2018/12/07 17:29

Taiwan’s exports end 24 consecutive monthly increases. (By Central News Agency)

TAIPEI (Taiwan News) – Taiwan’s exports ended 24 consecutive months of increases by recording a drop of 3.4 percent for November, the government announced Friday.

The Ministry of Finance (MOF) identified lower-than-expected sales of high-end smartphones, a weakening of overseas investment needs, and the impact of the trade war between the United States and China as the three reasons why exports fell in November compared to the same period last year, the Apple Daily reported.

The value of exports for November totaled US$27.81 billion (NT$858.78 billion), a drop of 3.4 percent compared to November 2017 and of 5.9 percent compared to October 2018, according to MOF data.

However, for the period from January to November 2018, exports still rose from the same period last year to reach a total of US$307.46 billion (NT$9.49 trillion), the MOF stated Friday.

100 days under Pakatan

Economy faces mounting risks

Prime Minister Mahathir Mohamad said his government had realized over a third of its 60 election promises “to unshackle Malaysia from the issue of corruption and ensure good governance” .PHOTO: EPA-EFE

PUBLISHED

AUG 18, 2018, 5:00 AM SGT

KUALA LUMPUR • Malaysian Prime Minister Mahathir Mohamad marked his 100 days in office yesterday with risks mounting against the economy.

Gross domestic product in the second quarter grew at 4.5 per cent, its slowest pace in over a year, the current-account surplus narrowed sharply and the currency is facing pressure as an emerging-market rout worsens.

After a shock election win in May, Tun Dr Mahathir has moved quickly to deliver on promises to a speech broadcast nationwide yesterday, Dr Mahathir said his government had realized over a third of its 60 election promises “to unshackle Malaysia from the issue of corruption and ensure good governance”. These measures included policies on declaring assets, bolstering anti-corruption institutions and protecting media freedom.

The political transition had an impact on the economy last quarter, with public sector investment contracting 9.8 per cent from last year.

Noting in his speech that the national debt was RM 1 trillion (S$334 billion), Dr Mahathir listed infrastructure projects that have been put on hold, including the Singapore-Kuala Lumpur High-Speed Rail, the third phase of the Mass Rapid Transit and the China-backed East Coast Rail Link.

Domestic demand remained strong and was buoyed by the scrapping of a 6 per cent goods and services tax in June, another election pledge.

Related Story

100 days under Pakatan: Mahathir, the strongman reformist?

Related Story

100 days under Pakatan: Malay, Islamic issues still dominate politics

Private consumption climbed 8 per cent last quarter from a year ago, while investment surged 6.1 per cent.

“The bigger picture we see going forward, private consumption will be modest as many Malaysians probably front-loaded their purchases ahead of the sales tax coming in September, so it’s hard to see how that’s sustained,” said Mr. Brian Tan, an economist at Nomura Holdings in Singapore.

Central bank governor Nor Shamsiah Mohd Yunus said the economy will probably expand about 5 per cent this year, lower than the previous government’s projection of 5.5 per cent to 6 per cent.

BLOOMBERG, BERNAMA

A version of this article appeared in the print edition of The Straits Times on August 18, 2018, with the headline ‘Economy faces mounting risks’. Print Edition | Subscribe

Destitute dotage

Vietnam is getting old before it gets rich

That makes caring for the elderly hard to afford

Print edition | Asia

Nov 8th 2018| HANOI

As dawn breaks in Hanoi the botanical gardens start to fill up. Hundreds of old people come every morning to exercise before the tropical heat makes sport unbearable. Groups of fitness enthusiasts proliferate. Elderly ladies in floral silks do tai chi in a courtyard. In the shade of a tall tree, dozens of ballroom dancers sway to samba music. Others work up a sweat on an outdoor exercise-machine. Tho, an 83-year-old with a neat white moustache, says he comes to walk round the lake every day, rain or shine.

In the next few decades the gardens will become busier still. Vietnam has a median age of only 26. But it is greying fast. Over-60s make up 12% of the population, a share that is forecast to jump to 21% by 2040, one of the quickest increases in the world (see chart). That is partly because life expectancy has increased from 60 years in 1970 to 76 today, thanks to rising incomes. Growing prosperity has also helped bring down the fertility rate in the same period from about seven children per woman to less than two. In the 1980s the ruling Communist Party started to enforce a one-child policy. Though less strict than China’s, it has hastened the decline.

Demography is changing in similar ways in many Asian countries. But in Vietnam it is happening while the country is still poor. When the share of the population of working age climbed to its highest in South Korea and Japan, annual GDP per person (in real terms, adjusted for purchasing power) stood at $32,585 and $31,718 respectively. Even China managed to reach $9,526. In Vietnam, which hit the same peak in 2013, incomes averaged a mere $5,024. Indonesia and the Philippines are expected to reach the turning-point in the next few decades, with an income level several times higher than Vietnam’s.

This shift brings headaches. First, will the government be able to support millions more Vietnamese in old age? Only the extremely poor and people over 80 (together around 30% of the elderly) get a state pension, which can be as little as a few dollars a week. The most recent survey of the old, in 2011, found that 90% of them had no savings worth the name. Debt was common. Supporting them will become ever more expensive. The IMF predicts that pension costs, at the present rate, could raise government spending as a share of GDP by eight percentage points by 2050. That is faster than in any of the other 12 Asian countries it examined.

The problem is worse in the countryside, where most old folk live. Previously the young cared for their parents in old age. Today they tend to abandon village life to seek their fortune in the city. Surveys suggest that the share of old people living alone is rising, especially in villages. Many work until they die. Around 40% of rural men are still toiling at 75, twice the rate of city-dwellers. In Britain that figure is 3%. Often they do gruelling manual jobs, such as rice farming or fishing.

Providing health care for millions more old people is another worry. Alzheimer’s, heart disease and age-related disability are growing. In the botanical garden Toau, a 78-year-old in a white sports t-shirt, says he is there on doctor’s orders, before taking a pill for his bad heart and joining an exercise group. About a third of over-60s do not have health insurance, which is costly. Many provinces still have no proper geriatric departments in hospitals. Informal health-insurance groups have popped up to fill the gaps. For a fee, members get exercise classes and free check-ups. But few doctors are trained or equipped to treat more serious conditions.

The government is starting to implement policies to reduce the fiscal burden and improve the lot of the elderly. Last year it relaxed the one-child policy. In May it said it would increase the retirement age from 55 to 60 for men and 60 to 62 for women, and reform the pension scheme to provide wider coverage. Next year it plans to begin revamping the health-insurance and social-assistance systems.

But none of that will change the structure of the economy. Usually as countries climb the income ladder, they shift from farming to more productive sectors, like services. By this yardstick, Vietnam is lagging its neighbors. When the working-age population peaked in 2013, agriculture accounted for 18% of the economy. At the same juncture in China, agriculture was just 10% of GDP. Worse, farmers’ output tends to decline with age, unlike, say, that of managers. This over-reliance on agriculture partly explains why three-quarters of Vietnam’s workers are in jobs where they become less productive as they get older. In Malaysia that is the case for only about half the labour force.

Boosting productivity will be tricky. The government is still wedded to “statism”. State-owned enterprises dominate many industries. Most university students, meanwhile, waste at least a year learning Marxist and Leninist theory. Many countries in Asia are ageing fast. But growing old before it becomes rich makes Vietnam’s problems all the greater.

Economists fret over trade tensions, shave forecast for Singapore growth in 2019

WED, DEC 12, 2018 – 12:00 PM

ANNABETH LEOW leowhma@sph.com.sg@AnnabethLeowBT

For 2018, Singapore’s economy is expected to grow by 3.3 per cent, a tad up from September’s forecast of 3.2 per cent.

ST PHOTO: KUA CHEE SIONG

PRIVATE economists unanimously fingered higher US-China trade tensions as a downside risk to Singapore’s growth, as they dialed down their forecast for 2019 in a recent industry poll.

Economists expect Singapore’s gross domestic product (GDP) growth to ease to 2.6 per cent in 2019, from an estimated 3.3 per cent in 2018, according to results out on Wednesday from a quarterly survey by the Monetary Authority of Singapore (MAS).

They had previously projected in September’s poll that the national GDP would notch 3.2 per cent growth in 2018 and 2.7 per cent in 2019.

The subdued showing is expected to come on the back of a marked slowdown in manufacturing growth – from an estimated 7.4 per cent in 2018, to just 3 per cent in 2019 – and cooling growth in the finance and insurance sector, from 6.9 per cent in 2018 to 5.4 per cent in 2019.

The weakness is expected to extend to the accommodation and food services sector, where growth could ease from 3.4 per cent in 2018 to 2.8 per cent in 2019.

SEE ALSO: Singapore retail sales inch up by 0.1% in October as growth tapers off

Such declines would offset the anticipated improvement in wholesale and retail trade – with growth expected to pick up from 1.3 per cent in 2018 to 1.7 per cent in 2019 – and a turnaround in the construction sector, which could go from a year-on-year contraction of 3.5 per cent in 2018 to an expansion of 1.5 per cent in 2019.

Growth in non-oil domestic exports is expected to fall by more than half, from 6.2 per cent in 2018 to 2.9 per cent in 2019.

Headline inflation was predicted to come in at 0.5 per cent for 2018, in line with official estimates, as private economists moved their forecast down from September’s 0.7 per cent.

They also trimmed their expectations for 2019’s headline inflation numbers, to a forecast of 1.3 per cent, from the 1.5 per cent that was anticipated in September.

The downgrade came on the back of an expected moderation in private consumption, from 3.4 per cent growth in 2018 to 3.1 per cent in 2019.

Estimates for core inflation – an MAS indicator that strips out private transport and housing costs – were kept intact at 1.7 per cent for 2018 and 1.8 per cent for 2019.

Meanwhile, trade protectionism was seen as the top risk to the economy by far – picked by all of the survey’s respondents, against 89 per cent of them in September – even as the share of watchers concerned by rising interest rates and a slowdown in China also edged up to 41 per cent of respondents, from 37 per cent in the previous survey.

“A growing number of respondents flagged slower growth in China as a downside risk, on the back of tightening credit conditions,” said the MAS in its summary of the survey results.

“Faster than expected US interest rate hikes, which could trigger financial market turbulence, also continue to be a downside risk for a number of respondents.”

But, on the bright side, cooling trade tensions could lift the growth outlook, said 47 per cent of respondents, up from 37 per cent in September.

Slower-than-expected monetary tightening in the US, as well as potential benefits from the diversion of trade and investment out of China and into the region, also appeared on the list of top three upside possibilities – both cited by 29 per cent of respondents.

The central bank’s December survey, which was sent out on Nov 22, netted replies from 23 economists who track the Singapore economy. It does not represent the MAS’s views or forecasts.

Philippines Q3 GDP growth slows, misses forecast

THU, NOV 08, 2018 – 11:00

[MANILA] The Philippines’ economic growth slowed in the third quarter due to weaker household consumption and exports, the statistics agency said on Thursday.

Gross domestic product grew 6.1 per cent in the third quarter from a year earlier, below the 6.3 per cent median forecast in a Reuters poll and slower than the previous quarter’s upwardly revised 6.2 per cent growth.

Details on quarterly growth are due to be released later.

REUTERS

Thailand Needs More Skilled Foreign Workers

Thailand needs to attract skilled foreign workers, especially in the industrial technology sector

The minimum monthly income for highly-skilled experts Smart Visa has been changed to 100,000 baht and to 50,000 baht for experts in startups and retired experts

By Olivier Languepin On Dec 5, 2018

Samut Sakhon One Stop Service

A Thai academic says the nation needs to attract skilled foreign workers to work in the country, especially in the industrial technology sector, to overcome a shortage of skilled-workers.

In a seminar held by the Institute for Population and Social Research of Mahidol University, a university researcher, Ms. Sureeporn Phanpueng , revealed that Thailand needs around 2.3 million more skilled employees to work in innovative and technological industries, robotics, and the health and food industries.

The event was attended by academics and those from related fields. Ms. Sureeporn proposed that the government solve the problem by offering work visas to skilled foreign workers who take up positions in Thailand and by creating an attractive living environment for them.

She also wants the government to promote the transfer of technological know-how between foreign experts and Thai workers, as well as international education in Thailand.

RELATED POSTS

Southeast Asia Internet economy to be worth $240bn by 2025

Nov 23, 2018

Thailand’s Smart Visa Requirements Made Easier

Nov 20, 2018

The government is now accepting four-year visa-free grants and free work permits under the “Smart Visa” programme which is targeting industry experts and foreign technology investors.

Thailand’s Smart Visa Requirements Made Easier

The Thai government has improved requirements and conditions for the Smart Visa in order to provide greater convenience for foreign investors and experts

For example, the government has changed the income condition for highly-skilled experts and senior executives from a monthly salary of no less than 200,000 baht to a monthly income that also covers bonuses and other incomes.

The minimum monthly income for highly-skilled experts has also been changed to 100,000 baht and to 50,000 baht for experts in startups and retired experts. The adjustments are aimed at increasing the country’s competitiveness and ability to attract more specialists.

Similarly, the government has improved various conditions in increasing access to capital for startups and strengthening venture capitalists. For example, investments can now be made through venture capital companies.

For the Thailand 4.0 policy to effectively push for digital transformation, Thai manufacturers will need to first improve the skills of their workforce,” said Karel Eloot, senior partner of McKinsey & Company, during an exclusive interview with The Nation.

The Thailand 4.0 policy is intended to modernize the Thai economy by promoting technologically driven industries. The development of the EEC region is a materialization of the Thailand 4.0 policy where the government aims to turn the three provinces of Chon Buri, Chachoengsao and Rayong into special economic zones.

“Re-skilling will be needed for the existing workers. We have identified up to 7 million employees in Thailand who will need to be reskilled for companies to digitally transform,” he said.

The re-skilling is needed because digital transformation will mean new roles and jobs will be created while old ones will be made obsolete, Eloot explained.

Australia’s economy is still booming, but politics is a cause for concern

Political infighting could harm the economy, says Edward McBride

Print edition | Special report

Oct 27th 2018

The last time Australia suffered a recession, the Soviet Union still existed and the world wide web did not. An American-led force had just liberated Kuwait, and almost half the world’s current population had not yet been born. Unlike most of its region, Australia was left unscathed by the Asian crash of 1997. Unlike most of the developed world, it shrugged off the global financial crisis, and unlike most commodity-exporting countries, it weathered the resources bust, too. No other rich country has ever managed to grow so steadily for so long (see chart 1). By that measure, at least, Australia boasts the world’s most successful economy.

Admittedly, as Guy Debelle of the Reserve Bank of Australia (RBA, the central bank) points out, this title rests on the statistical definition of a recession as two consecutive quarters of decline. Had the 0.5% shrinkage of the fourth quarter of 2008 been spread across half a year, he notes, there would be no record. Yet by other measures, Australia’s economic performance is more remarkable still. Whereas many other rich countries have seen wages stagnate for decades, Australia’s have grown strongly, albeit less steadily in recent years (see chart 2). In other words, a problem that has agitated policymakers—and voters—around the world, and has been blamed for all manner of political upheaval, from European populism to the election of Donald Trump, scarcely exists in Australia.

And that is not the only way in which Australia stands out from its peers. At a time when governments around the world are souring on immigration, and even seeking to send some foreigners home, Australia has been admitting as many as 190,000 newcomers a year—nearly three times as many, relative to population, as America. Over 28% of the population was born in another country, far more than in other rich countries. Half of all living Australians were born abroad or are the child of someone who was.

In part, this tolerance for outsiders may be a reflection of another remarkable feature of Australian society: the solvency of its welfare state. Complaints about foreign spongers are rare. Public debt amounts to just 41% of GDP (see chart 3)—one of the lowest levels in the rich world. That, in turn, is a function not just of Australia’s enviable record in terms of growth, but also of a history of shrewd policy making. Nearly 30 years ago, the government of the day overhauled the pension system. Since then workers have been obliged to save for their retirement through private investment funds. The modest public pension covers only those without adequate savings.

Australia’s health-care system is also a public-private hybrid. The government provides coverage for all, by paying clinics and hospitals a set fee for every procedure they perform. Those who want more than the most basic service must pay a premium. The government encourages people to take out insurance to cover the gap between the reimbursement it provides practitioners and the rates most of them charge the public. As with pensions, everyone gets looked after, but the government bears only a relatively small proportion of the cost—an arrangement that remains a distant dream in most rich countries.

Not all is perfect, of course. A common concern is that the economy relies too heavily on China, which is the biggest buyer of Australian minerals, the biggest source of tourists and foreign students, even the biggest consumer of Australian wine. People worry that if the Chinese economy falters, it will drag Australia’s down with it. Another fear, somewhat at odds with the first, is that China might try to use its economic power to blackmail Australia into weakening its alliance with America.

There are glaring domestic problems, too. The appalling circumstances of many Aboriginals are a national embarrassment, and the failure to answer their political grievances compounds the rancor. Even more alarmingly, global warming is making an already grueling climate harsher. Rainfall, never reliable, is scarcer and more erratic in many farming regions. Over the past two years unusually hot water has killed a third of the coral on the Great Barrier Reef, one of the country’s greatest natural treasures.

In theory both the governing Liberal-National coalition (which is right-of-centre) and the main opposition, the left-leaning Labor Party, are committed to cutting emissions of greenhouse gases. But in practice climate change has been the subject of a never-ending political knife-fight, in which any government that attempts to enact meaningful curbs is so pilloried that it either loses the next election or is toppled by a rebellion among its own Members of Parliament (mps).

Some see the failure to settle on a coherent climate policy as a symptom of a deeper political malaise. Australia used to have long-lived governments. Between 1983 and 2007, just three prime ministers (pm) held office (Bob Hawke and Paul Keating of Labor, and John Howard of the Liberals). Yet, since then, the job has changed hands six times. A full term is only three years, but the last time a prime minister survived in office for a whole one was 2004-07. The assassins are usually not voters, but fellow mps who dispatch their leader in hope of a boost in the polls. As part of the research for this special report, your correspondent interviewed Malcolm Turnbull, the prime minister at the time, who insisted his position was secure. He had been sacked by his fellow Liberals before the interview could be written up.

The changes of pm have come so often that Madame Tussauds, a wax museum, has officially given up trying to make statues of the incumbent, who will inevitably have left office before a likeness is ready. The constant revolution is not just fodder for comedians; it also makes consistent policy making much harder. For those who consider Australia’s unequaled economic performance the result, at least in part, of far-sighted decisions made 30 years ago, the current choppy politics seem like a harbinger of decline.

This special report will try to explain Australia’s enviable record, and ask how long its good fortune can last. Is it adopting the reforms needed to keep the economy bounding ahead? Will it have to choose between China and America? Is the current generation of politicians up to the job? Is Australia, in short, as lucky a country as its nickname suggests, or is its current streak coming to an end?