Canada Housing News

The big chill: A five-year house price forecast for 33 Canadian cities

Michael Babad

Published October 3, 2018

New forecasts suggest it’s “time for slower price growth” in Canadian housing markets.

Indeed, Moody’s Analytics and RPS Real Property Solutions have cut their five-year projections for many of the 33 cities studied from earlier forecasts in May.

The predictions from Moody’s Analytics, the sister company of the credit rating agency, which are based on RPS data, indicate federal and provincial policy makers have pulled off what they set out to do when they brought in measures to tame bubbly markets such as those in Toronto and Vancouver.

They also come amid fresh numbers that show the Vancouver-area market still struggling after British Columbia imposed an additional tax on foreign buyers of local real estate in 2016 and new federal mortgage-qualification rules were introduced last January.

At the same time, interest rates are rising, and are expected to continue to do so, further pressuring demand in what had, until recently, been unstoppable housing markets.

“Two macroeconomic projections now dominate housing markets in Canada,” said Moody’s economist Andrew Carbacho-Burgos.

“The first is that the [Bank of Canada] will continue to tighten short-term interest rates through 2020 in order to head off inflation and maintain the value of the Canadian dollar relative to its U.S. counterpart,” he added in his report released today, titled “Canada housing market outlook: Time for slower price growth.”

“With some lag, monetary tightening will pull up mortgage rates. The five-year mortgage rate is now at about 4.4 per cent after bottoming out at 3.6 per cent in mid-2017; the Moody’s Analytics baseline projection is that it will continue to increase until it levels off at about 6 per cent by late 2020.”

Here’s what Moody’s expects over the course of five years:

Source: RPS, Moody’s Analytics

There are other interesting tidbits in the report along with projections, these based on single-family homes:

1: Most Ontario cities “are still significantly overvalued, but this overvaluation has, on average, started to decrease.”

2: Toronto is overpriced to the tune of 51 per cent, compared to 53 per cent in May. Others that have come down even more sharply are the Ontario centres of Barrie, Guelph and Brantford.

3: The overpriced Vancouver market has also cooled off, but overvaluation still tops 40 per cent.

4: Montreal’s market is undervalued, but by less than 4 per cent.

5: Edmonton remains “the most undervalued metro area” in the country, by about 20 per cent, but it should see a faster pace of price growth after mortgage rate hikes end “thanks to a combination of reduced listings and increased opportunistic purchases.”

6: Saskatoon and most Atlantic cities are “moderately undervalued.”

“The national housing market still has a long way to go before it regains the level of affordability it had before 2015, when prices in Toronto and Vancouver took off, but has now taken the first steps to do so,” Mr. Carbacho-Burgos said.

“The important points are, first, that there is no serious projected house price correction,” he added.

“Second, median family income growth will have a good chance of keeping up with and even outpacing house prices in coming years, improving affordability. Third, the lack of a significant house price decline will prevent mortgage debt performance from deteriorating, especially after 2020, when mortgage rates level off.”

But along with that came a few notable warnings. Among them:

1: “Given that most of the house price increases took place in Toronto and Vancouver, there is still the downside risk that higher mortgage rates and the borrower stress tests could push down demand in the Atlantic and Prairie provinces, leading to a full house price correction and a perceptible drop in sales in these regions.”

2: “The main downside risk now is that the measures taken to stabilize housing affordability and mortgage credit quality may prove too strong and may precipitate not just a house price correction, but also an extended decline in sales and possibly a reduction in home ownership. However, the data for July and August indicate that home sales and house price growth have started to rally, so it is too soon to be pessimistic.”

3: While financing is showing little sign of stress, it is “starting to show the first looming danger signs.” Mortgage delinquency rates are at their best since the early 1990s, though those in Alberta, Saskatchewan and eastern Canada are notably above the national average.

“More important, the slow growth of income relative to house prices has led to a steady increase in the ratio of mortgage debt service to disposable income over the past 15 years, and this ratio is likely to keep increasing before the [Bank of Canada] finishes tightening interest rates,” Mr. Carbacho-Burgos said of that last part.

“Although it is possible to disagree over the merits of the new mortgage lending stress tests, the move to make mortgage lending more stringent is not surprising, given this 15-year trend.”

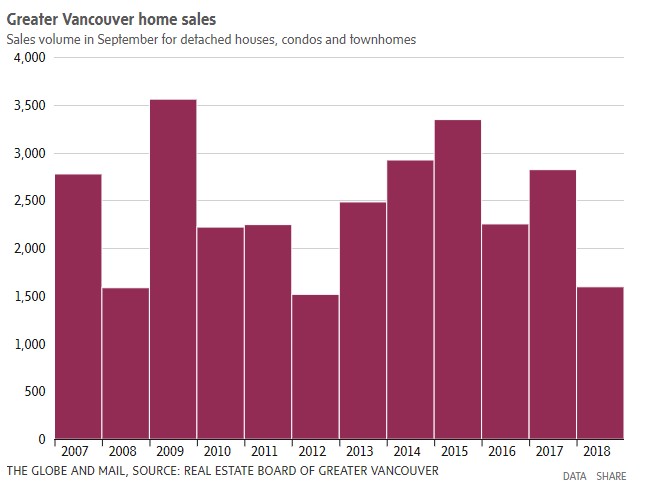

Vancouver, of course, is unique in Canada, with numbers released Tuesday showing a sales plunge of 43.5 per cent in September from a year earlier.

That’s “the steepest decline since the financial crisis and about 35 per cent below typical September activity seen over the past decade,” said Bank of Montreal senior economist Robert Kavcic.

“All the while, new listings jumped strongly in the month. To put it lightly, the market continues to struggle with past policy measures and higher interest rates. Indeed, prices continue to fade.”

The benchmark price is up, but just slightly above 2 per cent from a year earlier, while the cost of a detached home is down 4.5 per cent.

“We would not be holding our breath for a quick rebound in this market,” Mr. Kavcic said.

Greater Vancouver home sales

Sales volume in September for detached houses, condos and town homes

And, as The Globe and Mail’s Janet McFarland reports, Toronto’s housing market chalked up a modest sales gain in September after two much stronger months.

Sales climbed 1.9 per cent from a year earlier, as average prices gained 2.9 per cent in the same period, though dipped 0.5 per cent from August, according to Toronto Real Estate Board numbers released today.

“Looks like the whole market is balancing out about as well as policy makers could have hoped,” Mr. Kavcic said of the Toronto report.

“This could set us up for a period of price stability as solid demographic and job fundamentals are countered by rising interest rates.”

Separately, Mr. Kavcic’s colleague, BMO chief economist Douglas Porter, took a run through the latest Canadian credit numbers, noting they continue to show a slower pace of borrowing.

“The slowdown in credit – most notably, overall mortgages – syncs well with the broader cooling in housing market activity,” Mr. Porter said, citing the fact that the rise in total household borrowing eased in August to 3.7 per cent from a year earlier, while disposable income eclipsed that, at 3.9 per cent.

“The biggest chill has been in mortgage growth (not surprisingly), which has softened to a 3.6-per-cent year over-year clip from an average growth rate of about 6 per cent in the past two years,” he added.

“We are on the cusp of seeing the slowest growth in mortgage balances outstanding since the early 1980s.”

Read more

Janet McFarland: Toronto housing market’s hot rebound cools in September

Poltergeist II: The demons that still haunt Canada’s housing and credit markets

2018 has been unruly for housing markets: What’s ahead for your province

Rob Carrick: How the new NAFTA helps end a generational chance to score big in the housing market

Rob Carrick: It’s officially normal to have a big, fat balance on your line of credit

House price inflation in Canada suddenly trails that of 36 other countries

How $8-billion in added mortgage costs will squeeze Canadians and the economy

‘Cue the comeback’: The reawakening of many Canadian housing markets

Canada’s housing market scores first annual price gain in months

‘Good value for your money’: How downtown condo prices in Canadian cities compare globally

Carolyn Ireland: Sale by trial and error in Toronto’s housing market

Canadian index falls as 8 markets decline

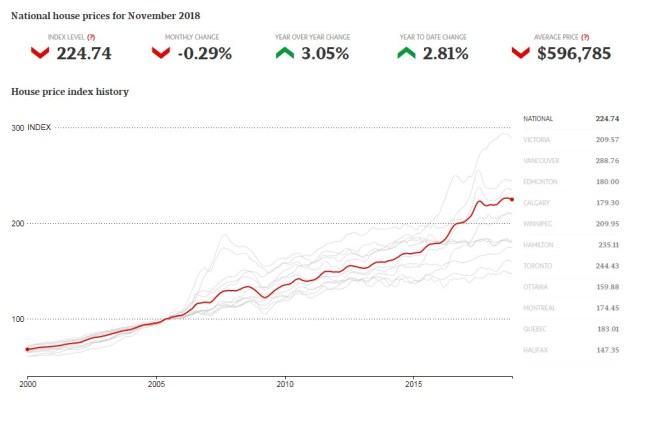

Canada’s home prices dropped 0.3 per cent in November from October, according to the latest numbers from the Teranet-National Bank House Price Index.

The retreat marks only the fourth time in the index’s 20-year history that the national market dipped in November, according to National Bank of Canada senior economist Marc Pinsonneault.

The decline was quite broad-based, Mr. Pinsonneault adds, with eight of the 11 major metropolitan markets in negative territory.

Compared with November of 2017, the composite index rose 3.1 per cent last month to stand at 224.74. The national index is down 0.66 per cent from its peak in September of 2018.

Mr. Pinsonneault says that demand has cooled significantly – particularly in the country’s most expensive real estate markets – because of more stringent mortgage qualification rules and the rise in interest rates.

But Mr. Pinsonneault adds that interest rates appear set to rise more slowly than most economists previously thought. Hopes for a soft landing of the Canadian resale market are therefore still warranted, in his opinion.— Carolyn Ireland

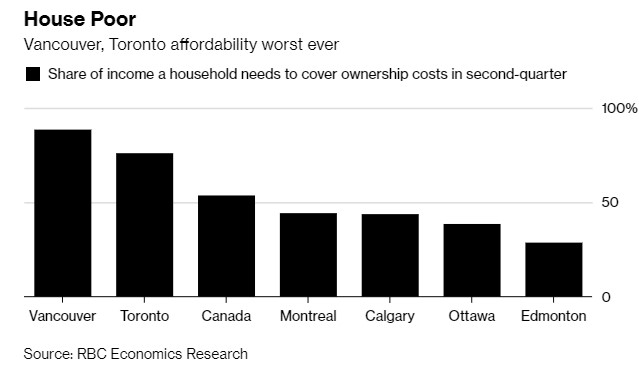

Cost of owning a home in Vancouver, Victoria ‘off the charts’ — and likely to get worse, warns RBC

It now costs 88 per cent of a typical income to carry a home in Vancouver, and 65 per cent of an income in Victoria.

Bloomberg News

Updated: September 28, 2018

The cost of owning a home in Canada is at the highest level in 28 years and likely to get only more onerous as interest rates continue to rise, according to a report from Royal Bank of Canada.

Carrying a home, including the cost of a mortgage, property taxes and utilities, took up 54 per cent of a typical household’s pre-tax income in the second quarter, the Toronto-based bank said in a report on Friday. That’s up from 43 per cent three years ago.

“From overheating to correction to the onset of recovery, we’ve seen pretty much everything in the past three years in Canada’s housing market,” economists at the Toronto-based bank said in the report. “Yet an eye-watering loss of affordability has been a constant.”

Lack of affordability is “off the charts” in Vancouver, Toronto and Victoria, with RBC’s index at 88 per cent, 76 per cent and 65 per cent respectively — the highest in records going back to the mid-1980s. The measure uses an aggregate of all housing categories, including single-family detached homes and condos.

While rising prices had been the culprit behind the loss of affordability between 2015 and 2017, mortgage-rate increases accounted for the entire rise in carrying costs over the past year, the bank said. The country’s central bank has risen interest rates four times since July, 2017.

“We expect the Bank of Canada to proceed with further rate hikes that will raise its overnight rate from 1.50 per cent currently to 2.25 per cent in the first half of 2019,” the report said. “This will keep mortgage rates under upward pressure and boost ownership costs even more across Canada in the period ahead.”

B.C. is in a “mild” housing market recession, with the Lower Mainland shifting from a seller’s market to a “mild” buyer’s market, according to a new housing forecast report.

A recession is usually used to describe a period of significant decline in the economy, but that term also applies to a B.C. housing market marked by a sharp decline in home sales, eroding prices, and a slowdown in housing starts, said Bryan Yu, deputy chief economist of Central 1 Credit Union, which released its B.C. housing forecast for 2018 to 2021 on Tuesday.

“When we look at it through these lens, it’s the first time we’ve seen these slowdowns, a cycle where there’s a decline in the number of transactions, erosion of home prices … and new home construction activity seeing a contraction,” said Yu.

Resales of residential properties dropped 17 per cent from 2017 to 2018, said the report, while housing starts slowed by 10 per cent, with another 18 per cent drop forecast for 2019.

Aggregate sales in the province’s urban centres — the Vancouver, Kelowna, Victoria and Abbotsford-Mission CMAs — fell 40 per cent from the end of 2017, but even medium and small markets were hit with a 10 to 20 per cent reduction in activity.

“When you add all these factors together, from a buyer’s standpoint, you have less access to credit and less confidence in the market as well,” said Yu, who expects these factors to be reflected in prices in the coming year.

A sales slump has cooled B.C.’s red-hot housing market, with the Lower Mainland shifting from a seller’s market to a “mild” buyer’s market, said a new report by Central 1 Credit Union. JONATHAN HAYWARD / THE CANADIAN PRESS

While median resale prices recorded a six per cent increase in 2018 compared to the previous year, it’ll dip a modest two per cent in 2019 to $520,000, said the report.

The trend will be more pronounced in the Lower Mainland/southwest region of B.C., where prices are expected to drop 3.6 per cent next year to $651,000.

But because the downturn is driven by policy measures such as the federal government’s mortgage stress test, the province’s introduction of the speculation tax and school tax, and Vancouver’s empty homes tax, and not by a broader economic slump, economists don’t see a major crash in housing prices.

There’s room for buyers to negotiate, but on the flip side, “the economy is strong enough that there aren’t that many sellers who have to bring down their price,” said Yu. “For most sellers, they don’t have to sell … It puts a cushion under the market.”

The report also examined B.C.’s rental housing market.

It said “renters will continue to experience stressful conditions,” with the province’s low rental vacancy rate of 1.4 per cent expected to hold steady through 2021 as renters struggle rents and continuing strong demand.

“Options are very limited,” said Yu. “There’s not a lot of supply out there.”

to shift into home ownership given tighter mortgage qualification require

United States Housing News

US Housing Starts Up, Permits Down: August 2018

September 26, 2018 Kéta Kosman

U.S. housing starts rose 9.2% in August, driven by an outsize leap in apartment building that masked weakening across single- and multifamily construction.

Single-family housing starts in August rose 1.9% to a seasonally adjusted annual rate of 876,000 units, and multifamily starts soared 27.3% to an adjusted annual rate of 392,000 units, according to the U.S. Department of Commerce’s monthly estimates.

SOURCE: U.S. Department of Commerce via For Construction Pros

U.S. housing starts rose 9.2% in August, driven by an outsize leap in multifamily building that masked softening housing construction conditions.

Monthly housing starts numbers are notoriously volatile, said For Construction Pros September 20. From the first of 2018, multifamily starts had trended down slightly through July. Multifamily starts year to date as of August, however, were 8.5% higher than the first eight months of 2017. The much larger category of single-family starts has been a bit more consistent, and the year-to-date total remains 6.9% above the same period last year.

The number of building permits issued tends to be a more stable measure and can help predict future home construction volume. Total permits dropped 5.7% from July to August, with single-family permits down 6.1% and multifamily permits down 4.9% for the month. The year-to-date totals show single-family permits more-consistently 6.5% above the first eight months of 2017, and multifamily permits 1.8% above last year.

ADN.TO, building, canada export, CFF.TO, construction, export development Canada, HomeBuilding, IFP.TO, lumber trade, madisons lumber reporter, NYSE: DHI, NYSE: HOV, NYSE: KBH, NYSE: LEN, NYSE: PHM, NYSE: RFP, NYSE: TOL, NYSE: WY, OSB.TO, RealEstate, sawmill, SJ.TO, softwood lumber, Softwood Lumber Prices, trade, trade deal, trade forecast, TSE: IFP, TSE: WEF, TSE: WFT, TSE:ADN, TSE:CFF, TSE:OSB, TSE:SJ, US home building, us home construction, US home sales, us house inventory, US house prices, us housing, US housing starts, UShousing, WEF.TO, WFT.TO

Housing Fundamentals Still Supportive For Lumber & Panel Markets- Madison

Preferred Solid Wood Names Remain TSX:IFP and NYSE:LPX

The U.S. housing market has turned in several months of lackluster performance, from slower-than-expected housing starts to weaker existing-home sales to a drop in pending home sales. It’s not exactly clear what is driving the disappointing results, or if they will last beyond the current spell (housing permits remain positive!), but they are of concern for investors in lumber- and OSB-leveraged stocks.

In this report, we review various scenarios for housing and repair and remodeling activity, combined with capacity additions for both lumber and OSB. Our analysis indicates that supply and demand for both lumber and OSB should remain reasonably tight through 2020, even if growth in both new construction and repair & remodeling market activity slows. There will continue to be volatility driven by seasonal factors, transportation, capacity ramp-ups, etc., but over the forecast period we see persistently solid fundamentals.

We caution, however, that headline risk in these names is elevated, as the industry reference forecasters continue to have high annual housing-start forecasts (table below): these numbers will have to come down based on recent housing-market performance and given that home builders are short labour and cannot make up for lost time. Similarly, consensus estimates for OSB names (Norbord in particular) look stretched to us, and we expect they will come in over time. Despite these risks, we anticipate continued strong cash flow generation from the solid wood names. The names have shown good discipline in M&A and balance sheets are in excellent shape. Large capital programs are either winding down or fully funded, and dividends have begun to rise. While we believe near-term peaks in commodity pricing are in (and past!) we see good fundamentals in solid wood for long-term investors. Our preferred route to lumber exposure remains IFP, given the larger relative impact from its capital program and its geographic diversification. In OSB, we favor LPX, with growing diversification into siding in new homes and the R&R market.

The latest data is not encouraging: The housing recovery has slowed from its prior modest pace, with potential for further slowing

Through the first half of 2018, single-family starts were up 8% y/y (not seasonally adjusted), in-line with market expectations. Multi-family starts have been more volatile, up 9% y/y in Q1, up 4% y/y in Q2 (up 7% through the first six months).

Through June and July, however, housing starts have disappointed, with June’s 1.158 (SAAR) falling 5% y/y. The decline was broad-based, with singles down 1% y/y and multis down 17%. In the South, home to about half of all U.S. housing activity, singles were flat y/y. It is worth noting that there were no big adverse weather events or major holidays to blame for the weaker-than-expected June stats.

The refrain we often heard following the June stats was “one month does not make a trend”. Fair enough. But July stats underwhelmed as well, coming in at 1.168MM (million) on a SAAR (Seasonally Adjusted Annual Rate) basis. Singles were up just 3% y/y and multis were down another 12%. The timing of the July 4th holiday did deserve some of the blame for the weaker-than-hoped for result, but clearly there was no catch-up on whatever was holding back June numbers. The one silver lining has been strong permit numbers over the last few months. July permits totaled 1,311MM, up 15% from June, and 4% higher than July 2017. Year-to-date, permits are up 6%.

As we head into the end of the year, there are several plausible paths forward for the U.S. housing market, and strong arguments for each. We summarize the alternatives below, with our housing-start forecast under each scenario and the attendant wood products demand summarized in the table above.

- Low: The U.S. housing recovery has hit an inflection point, and will see slower growth in starts — including single family starts — going forward. This scenario models demand if total housing start improvement fell to 4% and 2% growth in 2019 and 2020. The silver lining in this scenario is that housing could continue to grow at the new, slower pace even if the current torrid pace of U.S. GDP slows or falters, as home builders continue to meter out supply to a chronically under supplied market.

- Base case: June and July were just hiccups…just predictable bumps in the traditionally volatile housing market. Growth in single-family starts returns to its prior 5%–6% y/y growth rate.

- High: The pace of growth in the housing market accelerates through the remainder of the year on pent-up demand. Growth remains above trend at 6%–7% though 2020, taking total housing starts to 1.45MM.

Given we are already seven months into 2018, this year’s wood product demand numbers look very similar in all scenarios. The differences between absolute demand levels are really only meaningful in 2020 (e.g., a 2 Bbf (Billion board feet) difference in lumber demand in High scenario vs. Low). That said, if we see housing activity slow to the pace in the “Low” scenario, the impact on equities (and not just solid wood producers) would be much more significant and immediate.

Primary forecasters’ views are lagging the market; we expect downward revisions

Housing starts are the most watched, and variable, component of the various end uses for wood products. To start this year, consensus estimates for 2018 total housing starts were 1.27MM (table). Surprisingly, forecasts have actually nudged higher since the initial forecasts, with the current figures now just above 1.3MM starts. This comes in spite of lower-than-expected housing start numbers through the summer months. While home builder stocks have under performed and worries have begun to spread to other housing-related names, we have yet to see consensus housing forecasts come down. Likely downward revisions represent headline risks for solid wood stocks.

Factors that will determine the path forward for the housing market

Housing Supply: The supply of new housing is constrained…or is it?

The inventory of new homes for sale is often characterized as being low, but in fact inventories of both new and existing homes have returned to pre-housing crisis ranges (chart). After bottoming at less than 150k (1000) units in 2012, the inventory of new homes for sale has taken six years to return to more normal levels. Inventory of existing homes for sale has also fallen to about the same level as the glut of homes available after the crash has been absorbed. In terms of months’ supply (i.e., the supply measured against the pace of sales), new homes are actually running a little higher than pre-GFC (Global Financial Crisis) levels at ~5.5 months. Months of inventory is a more volatile, backward-looking metric, and we do not weight it heavily in our analysis.

Perhaps the better metric is the supply of lower-priced homes: it is clear that the supply of these homes has lagged the recovery of the more expensive categories. Sales of entry-level homes priced below ~$200k (and particularly below $150k) have seen more declines than increases since the recovery began in 2012.

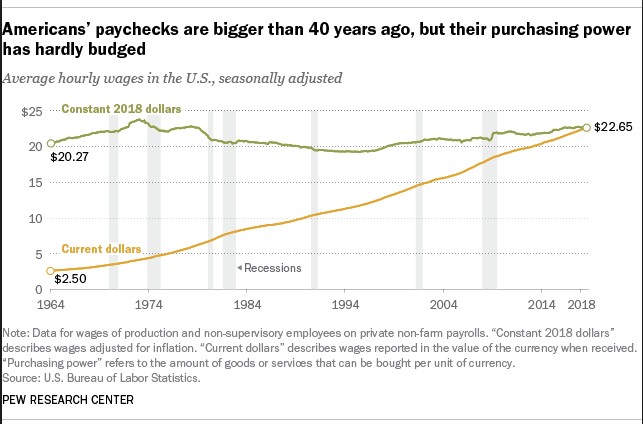

The average cost of a home has also been rising more quickly than average wages (charts, below). In addition, rents have been rising nationally, making it more difficult for prospective buyers to save for a down payment. Coupled with higher levels of student debt relative to prior cohorts, this puts the Millennial generation into a tight spot when looking at buying a first home.

On the home supply side, home builders are only building homes if they can make their 20% gross margin, which is more difficult to achieve on smaller, cheaper starter homes. Gross margins for the biggest home builders including DR Horton, Lennar, DR Horton and Toll Brothers have been remarkably flat right around 20% for the past five years (chart, left). Burned by the fires of the GFC, they now have an iron grip on costs, and no longer build ahead of demand. They have commented that they have not seen adverse impacts from cost escalation in “sticks and bricks” input costs, which likely reflects both their purchasing advantage given their size and their determination to pass costs on to buyers. Similarly, although lumber costs increased significantly in the past twelve months, they still represent just a fraction of overall building costs. A 50% increase in lumber prices, from $350 to $525, would have added roughly $2,625 to the cost of building a median single family home (requiring 15mfbm (Thousand Foot Board Measure) of lumber).

Rising lumber costs have not had an impact on builders’ margins (perhaps with the exception of entry level homes).

Home builders are also facing less competition in pricing from their peers, in part because they have fewer peers than they did in the last housing cycle peak. According to Census Bureau surveys, the total count of home builder businesses fell from just over 98,000 in 2007 to about 49,000 by 2012 (the 2017 survey numbers are not yet available). Industry concentration is greater in primary metro markets, while smaller builders operate in smaller regional markets.

Home builders have consistently indicated that their ability to supply homes (profitably) is constrained by labor and lot scarcity. Unfilled construction job openings hit at a peak of 263,000 in June according to the Bureau of Labor Statistics. This problem has been increasing for some time, and has been exacerbated by the crackdown on undocumented workers in the U.S. (no builder admits to using undocumented workers, but all suggest their competition does). The shortage of skilled builders is not easy to solve, and it will remain a restraint on housing supply for the foreseeable future.

Tight labor markets have also renewed interest in modular and off-site construction (chart). Roof, wall and floor truss manufacturing has expanded over the past few years even if full modular construction remains a tiny sliver of the total market. Increased use of trusses has alleviated some pressure on labor, but will not be sufficient to increase the total supply of housing units. We expect ventures like LPX’s $45MM investment in Entekra will help drive full modular home construction to ~20k units per year, concentrated in dense, costly U.S. metro markets like San Francisco, but will have limited application outside of these areas.

As for lots, big builders have slowly been improving their lot position, but primarily through options on land (large land positions were sold down through the GFC and builders have focused on options this time around). The improvement in access to lots is welcome, but we believe it is unlikely to spur a noticeable pick-up in home building over our forecast horizon.

Housing Demand: The need for housing is there, but the resources may not be, and desire could be flagging

Millennials (born between 1981 and 1996) have been much maligned for not doing their part for rampant consumption, preferring sharing over owning, and apparently preferring to work gigs rather than full-time permanent jobs. But whatever they lack in individual commitment and current resources, they make up in sheer numbers: at 83MM, they are the largest demographic cohort in the US. They are also entering prime home buying years. Even if home ownership rates are lower for this cohort than for prior age groups, we will see increased numbers of potential buyers over the next five years.

Through the GFC, the home ownership rate fell and the “Renter Nation” became a thing. Home ownership rates have been improving since their trough in early 2016, but remain far below pre-recession levels. Vacancy rates have fallen, too, and sit far below pre-recession levels. Tightness in the rental market has allowed rents to rise, which in turn has limited renters’ ability to save for a down payment. In addition, debt burdens — including student debt — have been higher for the current generation of potential homebuyers than for previous generations. An offset to this has been an increase in high loan-to-value lending, which reduces down payment requirements.

Affordability measures remain good relative to long-term trends, but as we all know, interest rates have been heading up, with another two Federal Reserve hikes expected through the balance of 2018, bringing the Fed rate to between 2.25% and 2.50%. Rising interest rates, however, generally only have a fleeting short-term negative impact on home buying. In fact, if accompanied by economic expansion, they are historically correlated with strengthening housing markets. With GDP growth running at 3%–4% in 2018, the rate hikes alone should not be a lasting drag on housing activity.

What does appear to be a drag, however, are home prices. The University of Michigan Consumer Sentiment survey indicates consumers believe it is a “bad time to buy” a home based on current “high” prices. It is interesting to note that consumers do not cite rising interest rates as a disincentive to purchasing a home (although low rates are no longer an incentive to buy a home), and have an overwhelmingly positive economic outlook. It just seems to be sticker shock, which is understandable given that the U.S. Census Bureau data indicates new home prices are twice what they were back in 2000, while real median household income has finally recovered…back up to the same level it was in 2000.

If housing starts do slow or stall out, where does that leave solid wood demand?

Continued steady growth in repair and remodel activity would bolster lumber markets, but the impact on OSB would be less significant. The outlook for R&R remains positive, despite uncertainty in the housing recovery. Harvard’s Leading Indicator of Remodeling Activity (LIRA) is used to project the rate of change in U.S. spending on home improvement and repair spending (R&R) for owner occupied homes.

Spending on R&R has been steadily increasing since Q1/10, climbing from an annualized $223B at that time, to $324B in Q2/18. According to the latest projections from Harvard, recent trends in homeowner spending on R&R will continue. The rate of growth may taper slightly in early 2019, but at 6.9% in Q1 and 7% in Q2, will remain at healthy levels. Annual spending on residential home improvements is expected to cross the $350B mark before the end of 2019, in part reflecting the increasing average age of US housing stock. The prognosis could be even better, but low transactions of existing homes for sale are currently hindering greater gains in remodeling activity, as significant R&R projects often occur around the time of a sale (particularly afterwards). With a slate of capacity expansion projects scheduled (or underway) for both lumber and OSB supply, growth in demand from R&R will play an increasingly significant role.

Solid wood demand: Lumber demand is more is more dependent on Repair & Remodeling activity, while commodity OSB is more leveraged to the U.S. single family housing market

Total U.S. lumber demand has grown steadily since the housing crash crushed consumption. Operating rates are finally returning to levels that can produce price spikes like the epic price run we saw earlier in 2018, which in turn pushed lumber producer EBITDA margins above 20%. Total U.S. demand was 47.6Bbf in 2017, up 1% or 0.6Bbf from the prior year. Since the depths of the housing collapse in 2009, U.S. lumber demand has grown at a CAGR of 5% or about 2.0Bbf per year, although this growth has been far from steady.

The single-largest end market for lumber in the U.S. remains the repair & remodeling market. This end market has been larger than the residential construction market since 2007, and represented 37% of lumber end demand in 2017, while new residential construction represented 32% of end demand (chart below). Given the aging U.S. housing stock and the lower supply of new homes, we expect growth in R&R activity to continue at 6%–7% annually for the next couple of years.

Growth of demand from new residential construction, however, has outpaced R&R since the trough, with a compound annual growth rate (CAGR) of 10% since 2007 against 5% for R&R. Materials handling and non-residential construction end demand have represented 10%–15% of lumber end demand over the past decade, with “Other” markets representing a fairly steady 6%–8%. Demand in non-residential and material markets was flat to marginally down in 2017.

For OSB, the picture is somewhat different. In 2017, total U.S. demand for OSB was 20.3Bsf (Billion Square Feet), up 5% or almost 1.0Bsf from 2016. Demand bottomed in 2010 at 12.8Bsf, and has grown at a CAGR of 7% or about 1.0Bsf annually since then. Unlike lumber, the largest end market for OSB is, by far, residential construction at 55% of 2017 total demand. Repair & remodel demand was less than half of this at 21%, followed by the smaller industrial (15%) and non-residential construction (9%) markets .

Demand growth has been greatest in residential construction, with the same 10% CAGR since 2009 as lumber. Growth in R&R demand has been lower at 4% since 2009.

House size and the multi-family/single-family split are important for wood products usage

While the total volume of solid wood products going into new residential construction has increased over the past 10 years, the intensity of solid wood use per square foot of new floor space has been quite consistent. We have kept our estimates of usage unchanged over our forecast horizon.

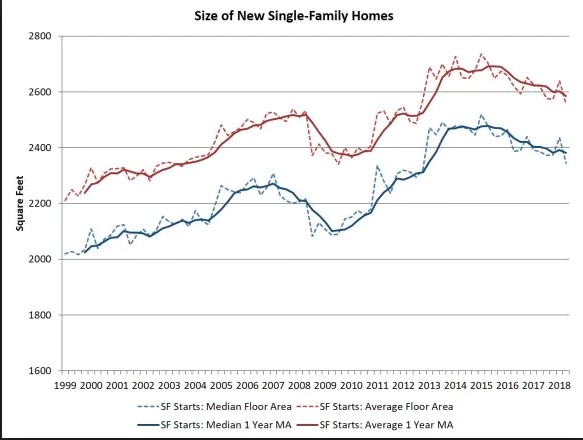

Measures of home size as well as the proportion of single-family versus multi-family starts are therefore the key variables in determining total solid-wood consumption in new residential construction. Housing square footage has ebbed and flowed over time, with median single-family unit size falling to a low of 2,100 sqft in 2009 before returning to 2,435 sqft in Q1/18. At our reference lumber intensity of 6.2 bf per square foot, the 16% increase in median size since 2009 corresponds to 2m bf implied incremental wood demand per unit. The increase in median unit size has amplified the effect of the 91% increase in single-family starts between 445k in 2009 and 849k in 2017 (adding roughly 1.7Bbf of demand).

The gains in single-family unit size are not uniformly good news, however. The housing recovery has been most robust in the upper end of the housing market price categories, while the smaller, cheaper, entry-level gains have lagged. Potential new home buyers are more likely to be shut out of home ownership (or have to postpone purchases) if affordable housing stock is not more readily available. We note median single-family square footage has been trending down — albeit unevenly — since peaking at 2,490 sqft in Q3/15, suggesting that smaller, more affordable homes are finally gaining market share.

Multi-family units are about half the size of single-family units. Multi-family units have occasionally hit 1,200 sqft, but have mostly bounced around 1,100 sqft. There has been some concern that Millennials (and other demographic cohorts) would forgo the traditional shift to a single-family unit in the suburbs and instead chose to remain in urban multi-family units as they form households. We would have expected to see an increase in the median size in multi-family units if this were the case, but we see no evidence of it in the stats (charts below).

Solid wood supply: lumber additions will be smaller, slower and have some offsets, while more net OSB supply is coming

Upcoming lumber projects will add 5Bbf lumber capacity (or about a 20% increase) in the U.S. South, but bottlenecks with contractors and equipment vendors, declining output from Western Canada, and continued growth in R&R demand means that new supply should be gradually added and easily absorbed.

We expect to see upward of 5Bbf of new lumber capacity in the U.S. South over the next three years — 1.1Bbf in 2018, a further 2.3Bbf in 2019, and 1.9Bbf in 2020 (which would represent 1.8%, 3.7% and 3.0% of total 2017 North American output, respectively). Nine proposed greenfield projects will account for just over 2.1Bbf of the incremental capacity, while the balance will be made up by a host of rebuilds and upgrades.

Taking our most conservative or “Low” scenario from the “Potential paths of U.S. housing” and comparing it to the total U.S. lumber demand from residential construction in 2017, lumber demand from residential housing and R&R would grow by roughly 4.5Bbf through 2020. With our “Base” housing outlook, 6.8Bbf of new demand would be created, and finally, under our “High” scenario for housing, an incremental 8.3Bbf of lumber demand would be created.

On the supply side, our “Low” scenario entails ~125% of announced new capacity making it to market (i.e., all recently announced projects, plus a few extra, are successfully completed), adding 7.8Bbf of new supply. Our “Base” case involves all of the projects announced to-date being completed by 2020, and would add 6.3Bbf of new capacity. Finally, the “High” case would see roughly 75% of announced capacity make it to market by 2020, adding 5Bbf of new supply.

Though there could be some short term loosening of markets or regional pricing weakness depending on the timing and location of capacity additions, as the table above shows, in all but the “low” scenario, new supply is absorbed by incremental demand, keeping lumber markets strong through at least 2020.

Tightly bunched OSB capacity additions are expected to overwhelm markets if the housing recovery doesn’t deliver

There are currently five new mills, representing ~2.7Bsf of capacity (almost 12% of North American production in 2017), in the process of ramping up. We expect to see between one and three further restarts in the next three years. A restart at Norbord’s 550MMsf Chambord, QC mill is more likely than not (we expect to see activity begin in earnest in H1/19 and meaningful production by H1/20), and start-ups at Louisiana Pacific’s Val D’Or, QC and Cook, MN mills could come the year after.

Our range of estimates for housing shows OSB demand from residential construction and R&R increasing by between 2.4Bsf and 3.9Bsf through 2020, with between 1.9Bsf and 3.2Bsf of additional supply set to ramp up over that time frame. Unlike lumber, supplemental demand from R&R growth won’t add massively to demand.

In our low scenario, new supply exceeds forecast demand growth, but not by much. We would expect incremental pressure on OSB prices, but no collapse. Our current benchmark NC OSB price forecast is $310 for 2019 and $307 for 2020, down from highs of $353 in 2017 and a forecast $379 average in 2018.

Investment recommendation: Opportunity for volatility will no doubt continue, but supply and demand look balanced

US HOUSE PRICES, CONSTRUCTION JOBS: SEPT 2018

CoreLogic® Thursday released the CoreLogic Home Price Index (HPI™) and HPI Forecast™ for September 2018, which shows US home prices rose both year over year and month over month. Home prices increased nationally by 5.6 percent year over year from September 2017. On a month-over-month basis, prices increased by 0.4 per cent in September 2018. (August 2018 data was revised. Revisions with public records data are standard, and to ensure accuracy, CoreLogic incorporates the newly released public data to provide updated results each month.)

Looking ahead, the CoreLogic HPI Forecast indicates home prices will increase by 4.7 per cent on a year-over-year basis from September 2018 to September 2019. On a month-over-month basis, home prices are expected to decrease by 0.6 per cent from September to October 2018. The CoreLogic HPI Forecast is a projection of home prices calculated using the CoreLogic HPI and other economic variables. Values are derived from state-level forecasts by weighting indices according to the number of owner-occupied households for each state.

The CoreLogic Year-over-Year increase has been in the 5 per cent to 7 per cent range for the last few years. This is still near the middle of that range. The year-over-year comparison has been positive for over six consecutive years since turning positive year-over-year in February 2012

Read more at https://www.calculatedriskblog.com/2018/11/corelogic-house-prices-up-56-year-over.html#GQZXfhfSFA7JMAwU.99

SOURCE: Upfina.com

Elsewhere, according to the US Bureau of Labor Statistics Job Openings and Labor Turnover Survey (JOLTS) and National Association of Home Builders analysis, released November 6, the count of unfilled jobs in the US construction sector pulled back in September, off a upwardly revised August estimate that marked a post-recession high.

the number of open construction sector jobs decreased to 278,000 in September. The August estimate of open construction jobs was revised up to 317,000, the largest count since the Great Recession.

The open position rate (job openings as a percentage of total employment plus current job openings) fell back to 3.7 per cent in September. The rate was 2.5 per cent last September. On a smoothed, twelve-month moving average basis, the open position rate for the construction sector increased slightly to 3.3 per cent, a post-recession high. The peak (smoothed) rate during the building boom prior to the recession was just below 2.7 per cent. For the current cycle, the sector has been above that rate since November 2016.

SOURCE: NAHB Eye on Housing

US HOME PRICE APPRECIATION AND PRICE-TO-RENT RATIO: AUGUST 2018

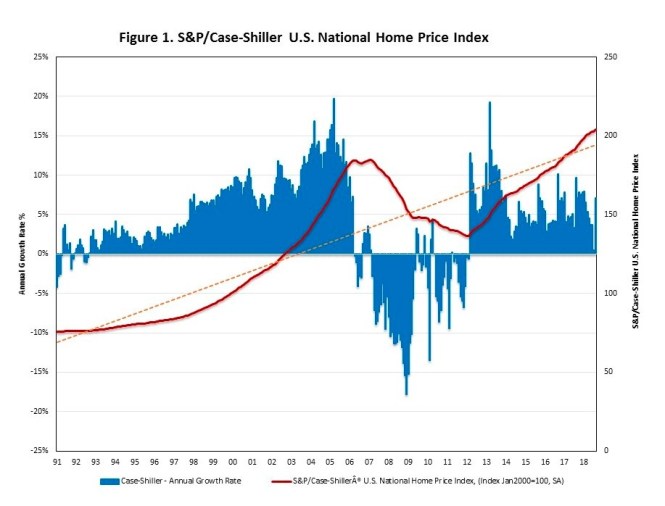

Nationally, home price appreciation continued in August. Based on a seasonally adjusted annual growth rate, home prices in Seattle, New York and San Diego declined faster in August than in July. Home prices in New York has decreased for the fifth consecutive month.

The S&P CoreLogic Case-Shiller U.S. National Home Price Index, reported by S&P Dow Jones Indices, rose at a seasonally adjusted annual growth rate of 7.2% in August, following an unusual 0.5% annual rate in July. On a year-over-year basis, the S&P Case-Shiller U.S. National Home Price NSA Index rose by 5.8%, the lowest annual gain in the past twelve months. The Home Price Index, released by the Federal Housing Finance Agency (FHFA), rose at a seasonally adjusted annual rate of 3.1% in August, slower than the 4.4% increase in July.

Elsewhere, in October 2004, Fed economist John Krainer and researcher Chishen Wei wrote a Fed letter on price to rent ratios: House Prices and Fundamental Value. Krainer and Wei presented a price-to-rent ratio using the OFHEO house price index and the Owners’ Equivalent Rent (OER) from the BLS, said Bill McBride on Calculated Risk Wednesday.

Here is a similar graph using the Case-Shiller National and Composite 20 House Price Indexes.

This graph shows the price to rent ratio (January 2000 = 1.0).

On a price-to-rent basis, the Case-Shiller National index is back to February 2004 levels, and the Composite 20 index is back to November 2003 levels.

In real terms, prices are back to mid 2004 levels, and the price-to-rent ratio is back to late 2003, early 2004.

Read more at https://www.calculatedriskblog.com/2018/10/real-house-prices-and-price-to-rent.html#p8ux2OwKepTE2vRy.99

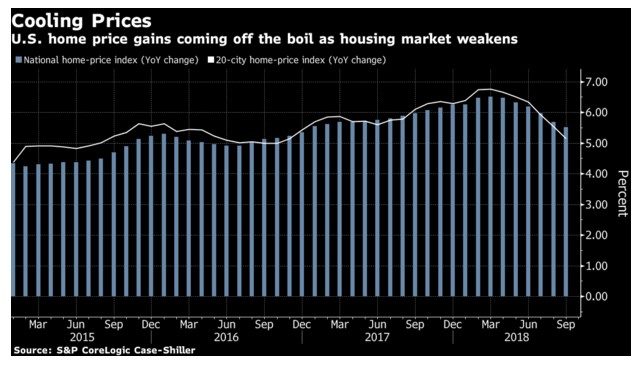

Home Prices in 20 U.S. Cities Rise Least in Almost Two Years

By

November 27, 2018, 7:00 AM MST Updated on November 27, 2018, 7:39 AM MST

Home-price gains in 20 U.S. cities grew in September at the slowest pace in almost two years, adding to signs that buyer interest is waning amid higher mortgage rates and elevated property values.

The 20-city index of property values increased 5.1 percent from a year earlier, the least since November 2016, after rising 5.5 percent in the prior month, according to S&P CoreLogic Case-Shiller data released Tuesday. The median estimate in a Bloomberg survey of economists called for a gain of 5.2 percent. Nationally, home prices were up 5.5 percent from September 2017.

Key Insights

- The report marks the sixth straight deceleration in price gains. It’s the latest in a spate of reports indicating housing is in a broad slowdown, with sales and home-building also showing signs of weakness.

- While the 0.3 percent monthly increase in the seasonally adjusted 20-city index was slightly above projections for 0.2 percent, economists look at the year-over-year gauge for a better indication of trends.

- The results also indicate more prospective buyers may be able to enter the market in coming months, though property values remain elevated, mortgage rates are near an eight-year high and the supply of affordable properties is still limited.

- The respite on price appreciation may be especially attractive for younger buyers or those purchasing a house for the first time; on the flip side, softer price gains also mean smaller advances in equity for owners.

- “Home prices plus data on house sales and construction confirm the slowdown in housing,” David Blitzer, chairman of the S&P index committee, said in a statement.

Get More

- All 20 cities in the index showed year-over-year gains, led by a 13.5 percent increase in Las Vegas and 9.9 percent in San Francisco.

- Prices in Seattle fell 0.3 percent from the prior month; annual gains have slowed to 8.4 percent from double digits earlier this year. San Diego was the only other city to record a monthly drop, at 0.1 percent.

- New York, hit by new federal limits on mortgage and property-tax deductions, had the weakest annual price gain at 2.6 percent, while Washington was second-lowest at 2.9 percent.

- Separate figures released Tuesday by the Federal Housing Finance Agency also showed prices climbing at a slower pace. The agency’s index rose 6.3 percent in the third quarter from a year earlier, compared with a 6.8 percent in the second quarter. For September, prices rose 0.2 percent from the prior month.

— With assistance by Jordan Yadoo, and Christine Maurus

(Updates with FHFA index in last bullet point.)

US CONSTRUCTION SPENDING: SEPTEMBER 2018

A very good indicator of current construction activity, thus future lumber prices, is US construction spending. New data out this week from the US Commerce Department shows construction spending flat in September 2018 after a 0.8 per cent rise in August, said the New York Times Thursday. Spending on US construction projects was essentially unchanged in September, the weakest showing since June, as an increase in home construction was offset by a slide in spending on government projects.

The strength last month was driven by a 0.6 per cent increase in residential construction and a smaller 0.1 per cent increase in nonresidential activity, which pushed this category to an all-time high. However, these gains were offset by a 0.9 per cent drop in spending on government projects.

The increase in residential construction featured an 8.7 per cent jump in apartment construction, which offset a 0.8 per cent drop in single-family homes.

SOURCE: NAHB Eye on Housing

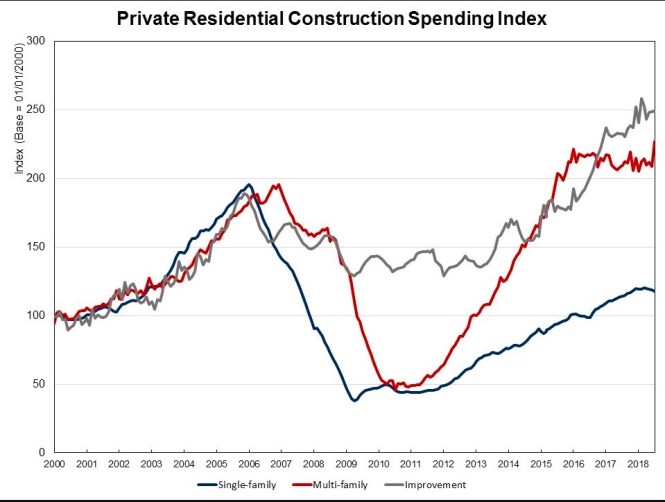

Drilling down to more detail, the National Association of Home Builders said it’s analysis of Census Construction Spending data shows that total private residential construction spending inched up 0.6 percent in September, after a dip of 0.4 percent in August. On a quarterly basis, private residential construction spending climbed 0.9 percent in the third quarter. Private residential construction spending increased in September, despite the decline of the total housing starts amidst the shortage of construction labor and land, rising mortgage rates, and ongoing building material price volatility.

The monthly gains are largely attributed to the strong growth of spending on multifamily.

Why Have Lumber Prices Fallen?

Posted by Pete Stewart on December 10, 2018

The US housing sector—a bellwether for economic health—has showed signs of stagnation (and even the prospect of reaching peak housing in this market cycle) in recent months. As I wrote last month, forecasts for housing starts are simply overblown, as there isn’t much room for an increase beyond the 2018 level of 1.266 million units.

As a commodity largely tied to housing starts and broader building and construction activity, lumber prices also reflect the general health of this market via supply and demand metrics. After steady increases beginning in 4Q2017, lumber prices skyrocketed to new record highs in 2Q2018 before dropping precipitously across the board over the last four months. Southern yellow pine (SYP) lumber prices recently hit their lowest point since August 2017; Forest2Market’s SYP composite index price for mid-November was $376/MBF—a 35% drop from the record high of $576/MBF achieved in May.

Despite the one–two hurricane punch that recently impacted the US South and the continued wildfires in the Pacific Northwest (PNW)—extreme weather events that have significantly impacted forest inventories, harvests and supply—the drop in lumber prices over the last six months is largely, though not entirely, demand driven. Fewer new-home builds = less lumber.

The sudden reversal begs a serious question: Did the lumber market simply over drive its headlights in the price run-up earlier this year, or are there more structural forces at work? Several dynamics are combining to impact housing starts and, by extension, the North American lumber market.

Supply Analysis

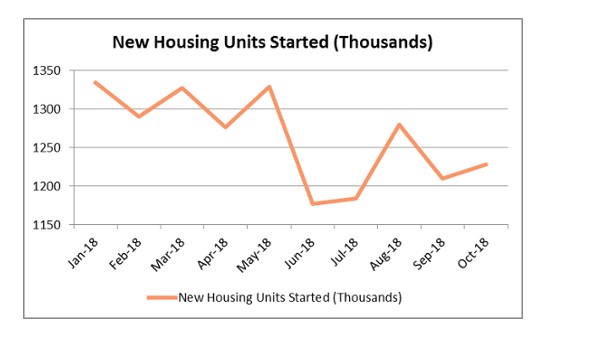

Housing starts kicked off 2018 with a bang, leading many to believe that there would be a gap in supply once the busy part of the building season hit. January starts were up 9.7 percent over December 2017 to a seasonally adjusted annual rate (SAAR) of 1.326 million units, and speculation began to drive lumber prices ever higher.

But as the meat of the building season came and went and housing starts failed to live up to expectations (now on pace at a SAAR of 1.228 million units), lumber production numbers confirm that any supply concerns were exaggerated. Both US softwood lumber production and total softwood imports have increased year-over-year (YoY). Through August 2018, US production was 23.8 Bbf (+4.8%) and total imports were 10.3 Bbf (+1.3%). Despite the tariffs on Canadian product, imports from Canada were only off 1.4% YoY to 9.3 Bbf through August. Latin America (primarily Brazil) and European producers more than made up for the difference in Canadian volume; LatAm shipments to the US totaled 306 Mbf (+8.3%) while European shipments totaled 589 Mbf (+65%) through August.

We may see this trend reverse course when full 3Q and 4Q trade statistics are reported; however, those numbers will be immaterial to this analysis. The data show that domestic and import supply was ample through the price run-up that began in 1Q2018 and peaked in 2Q. Neither US production nor imports through August suggest any supply-side disruptions that would account for such a dramatic surge in price.

Decreasing Demand for Homes

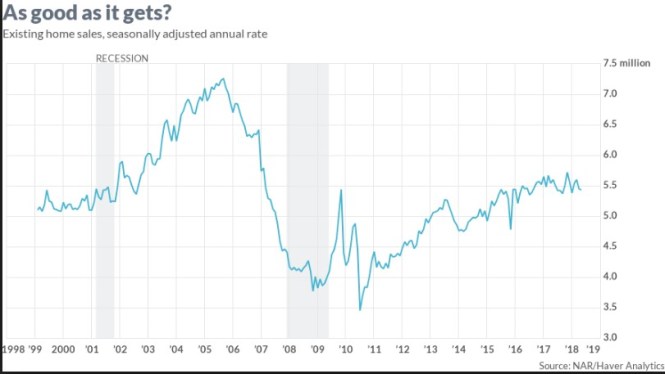

“Housing is no longer a tail wind for the economy, but [so far] the headwinds are blowing very gently,” wrote Michelle Meyer, a Bank of America Merrill Lynch economist, in October. One sign of a shifting housing market is slowing demand—including buyer traffic—for existing homes. Resales earlier this fall suffered the largest drop in 2½ years to the slowest pace since November 2015. Though still high, resale price appreciation has been decelerating (below +6% YoY for the first time in 12 months) and the supply of existing homes, while still low, is gradually expanding; there were 4.4 months of supply in September, up from the year-earlier 4.2 months.

Based on the behavior of the exchange-traded fund iShares US Home Construction (ITB), which tracks a basket of 47 US home builders and construction-related companies, investors apparently agree with Meyer’s sentiment. As of mid-November, ITB’s share price had fallen over 34% from its mid-January peak. Builders are in a tough spot, as they have been hit with a number of challenges this year including an increase in materials costs, land and labor shortages and a shrinking appetite of prospective buyers who are willing pay up.

Real private residential investment (PRI) declined for a third quarter in 2Q2018; as a percentage of total GDP, the decline has been in place since 1Q2017. Although both metrics have receded only modestly from their corresponding recent peaks, they nonetheless paint a potentially disconcerting picture for the sustainability of this market cycle.

Increasing Inventory of Homes

Interestingly, especially since there is a consensus that more new-home supply is needed, rising inventory is even more pronounced in newly-built homes. After meandering around an average of 5.3 months between July 2013 and December 2017, new-home inventory has trended higher in 2018 (to September’s 7.1 months of supply). In addition, the ratio between starts and new-home sales reached 1.5 in September, which is in the top 14% of monthly ratios since January 1995. The implication is that unless the pace of new-home sales picks up, starts will ultimately be forced lower.

With long-term Treasury yields helping to push mortgage rates upward, the median new-home prices less than 7% off November 2017’s record high, and resale appreciation only gradually slowing, it is entirely possible that housing demand could weaken further in coming months. Despite sustained high home prices (and surging prices in some markets) some regions are now drifting into the “buyer’s market” column.

Interest Rates

With home appreciation and mortgage rates trending higher, the reality is that many potential borrowers simply can’t make the mortgage numbers work. One way to measure the impact of inflation, mortgage rates and home prices on affordability over time is to use CoreLogic’s “typical mortgage payment,” which is a mortgage-rate-adjusted monthly payment based on each month’s US median home sale price. The number is calculated using Freddie Mac’s average 30-year fixed-rate mortgage rate with a 20% down payment, and it doesn’t include taxes or insurance. As such, the typical mortgage payment is a good measure of affordability because it shows the monthly amount that a borrower needs to purchase a median-priced US home.

The US median home sale price in August 2018 ($226,155) was up 5.7% YoY, while the typical mortgage payment was up 14.5% YoY due to a nearly 0.7-percentage-point rise in mortgage rates over that period. Tight housing inventories coupled with rising home costs are a real barrier for potential homebuyers, but a typical mortgage payment that is rising at over twice that pace is a much more serious concern, and a number of forecasts call for even higher rates next year.

Moody’s Investors Service has observed the deteriorating quality in mortgage loans noting that “The broad conditions under which loans are being granted have grown less favorable for future mortgage performance. For instance, home prices are no longer very affordable and rising interest rates are reducing refinancing incentives and prepayments.” Hence, “mortgages being originated today appear more likely to face a stressed environment within only a few years, [compared to] loans originated earlier during this long period of economic growth.”

And that’s just mortgage rates, which function independently of the federal funds rate instituted by the Federal Reserve (Fed). Though speculative at this point, the Fed is expected to raise interest rates once more this year and, potentially, three to four times next year, which will impact short-term and variable (adjustable) interest rates. Strategists warn that if the Fed tightens too much, economic growth could slump and trade wars could intensify, destroy demand and negatively impact earnings.

The potential scenarios in the wake of these rate hikes are many. However, the impacts of continued increases would most certainly discourage any expansion in new home ownership that would drive an increase in housing starts and additional demand for lumber.

Home Size

Not only have housing starts been decelerating since 2013, but home size has also been shrinking. Median floor area of new single-family completions peaked at 2,647 square feet (SF) in 2015 and has subsequently been declining on trend (to 2,426 SF in 2017). The median new home cost a record $133/SF in 2017, +30% relative to 2010. Apartments, by contrast, have been gradually expanding (2017 median: 1,096 SF) from 2013’s 1,059 SF. If these trends continue, net changes in demand for lumber and other building materials could well be negative. While the trend of slightly-shrinking single-family home sizes may seem minimal, the cumulative impact of fewer builds using less lumber is resulting in diminished demand.

Analysis of Economic Health: Forecasting Gross Domestic Product

Posted by Forest2Market on November 26, 2018

- inShare

Every month, Forest2Market publishes updated forecasting products designed specifically for participants in the forest value chain. The Economic Outlook is a macroeconomic indicator forecast that supplies critical information, context and insight about general economic trends and direction, and the 4Cast supports regional operational decision making for those who buy and sell timber. With an understanding of economic indicators, future stumpage prices and insight into buying and selling windows (periods in which buyers or sellers hold relative market advantage), subscribers are better able to time sales or purchases, negotiate prices, manage workloads and control inventory levels. The following commentary is just a sampling from the most recent Economic Outlook for November, 2018.

The robust economic momentum we’ve seen over the last several months may be slowing against the backdrop of a strong dollar and cooling global growth, which is restraining exports. There are few signs so far that US-China trade tensions are disrupting factory production, but manufacturers argue future output could be hurt as tariffs disrupt supply chains. Further, more than 70% of US firms operating in China and polled by the American Chamber of Commerce in South China are considering delaying further investment there and moving some or all of their manufacturing to other countries as a way to avoid the tariffs.

Trends in GDP

In its first estimate of 3Q2018 gross domestic product (GDP), the Bureau of Economic Analysis (BEA) pegged growth of the US economy at a seasonally adjusted and annualized rate (SAAR) of +3.50% (3.3% expected), down 0.65 percentage point (PP) from 2Q2018’s +4.15%. Three groupings of GDP components—personal consumption expenditures (PCE), private domestic investment (PDI), and government consumption expenditures (GCE)—contributed to 3Q growth. Net exports (NetX) detracted from growth.

On a year-over-year (YoY) basis, which should eliminate any residual seasonality distortions present in quarter-over-quarter (QoQ) comparisons, GDP in 3Q2018 was 3.04% higher than 2Q2017; that growth rate was slightly faster (+0.17PP) than 2Q2018’s +2.87% relative to 2Q2017.

Despite moderating from 2Q’s torrid pace, 3Q growth appeared quite solid—at least at the headline level; taken together, the 2&3Q GDP results also represent the strongest back-to-back quarterly growth rates since 2&3Q2014. Glancing below the headline of the latest report revealed some less appealing details, however. In contrast to relatively steady contributions from PCE (growth in goods and services spending: +0.11PP from 2Q) and GCE (+0.13PP from 2Q), commercial fixed investment was shown to be contracting at a 0.04% annualized rate (-1.14PP from 2Q); exports: -0.45% (-1.57PP from 2Q), and imports: -1.34% (-1.44PP from 2Q).

Inventories propped up 3Q’s result by contributing nearly 60% of the 3Q headline GDP number (+3.24PP from 2Q). Reflecting that influence, the BEA’s real final sales of domestic product, which excludes the effect of inventories, tumbled to +1.42% (-3.91PP from 2Q).

“The economy has reverted back to the ‘same old’ model of consumers accounting for most of the growth,” commented Bloomberg’s Carl Riccadonna, referring to the 2.7% PCE number. “Supply-siders will be disappointed to see business fixed investment essentially stalling out after a robust first half.

The implication is that the surge in growth is not the onset of the economy evolving toward a new speed limit,” concluded Riccadonna, looking forward; “rather, the frothiness in 2&3Q really does appear to be largely due to a sugar high from tax cuts. Unfortunately this is not sustainable barring tax cuts 2.0.”

“When we got the 2Q number,” concurred economic consultant Joel Naroff, “I suggested it could be the high water mark for this expansion. It is looking more and more like it will be. Household incomes are just not expanding fast enough to sustain the rapid spending paces posted in 2&3Q… [Also,] most business leaders have become somewhat cautious about the future and are holding off… major investment plans.”

“The fate of the consumer rests with the willingness and ability of businesses to keep hiring,” echoed former Federal Reserve researcher Julia Coronado. The slowdown in business spending “came earlier and was more than we expected, given where the [tax-cut] stimulus is,” Coronado said. “That suggests some of this stimulus won’t last, it’s not going to turn into higher-trend growth through the channel of investment and greater capacity and greater potential growth.”

“Don’t expect 4Q growth to be anywhere near what we have seen over the past two quarters,” Naroff concluded. “The economy is not faltering, it’s just that we are moving back toward more sustainable growth.”

The impacts on GDP of inventories and imports will bear watching as tariffs on $250 billion of Chinese products percolate through the economy. US companies appear to have “front-loaded” orders from China to beat the September 24 tariff deadline. Hence, it is possible the contributions to 4Q’s GDP headline from inventories and imports may flip relative to 3Q.