Japan’s Prime Minister and leader of the ruling Liberal Democratic Party (LDP) Shinzo Abe attends a debate with rival party leaders ahead of July 10 upper house election in Tokyo, Japan, June 21, 2016. (THOMAS PETER/REUTERS)

Japan’s cabinet launches stimulus package to boost growth

Tetsushi Kajimoto

TOKYO — Reuters

Published Tuesday, Aug. 02, 2016 5:31AM EDT

Last updated Tuesday, Aug. 02, 2016 7:59AM EDT

Japanese Prime Minister Shinzo Abe’s cabinet approved 13.5 trillion yen ($132.04-billion) in fiscal measures on Tuesday as part of efforts to revive the flagging economy, with cash payouts to low-income earners and infrastructure spending.

The package includes 7.5 trillion yen in spending by the national and local governments, and earmarks 6 trillion yen from the Fiscal Investment and Loan Program, which is not included in the government’s general budget.

Japan cabinet approves $132-billion spending boost (Reuters)

The stimulus spending is part of a renewed government effort to coordinate its policy with the Bank of Japan, but growing concerns that the BOJ policy has reached its limit triggered the worst sell-off in government bonds in three years.

“We compiled today a strong economic package draft aimed at carrying out investment for the future,” Abe told a meeting of cabinet ministers and ruling party executives on Tuesday morning.

“With this package, we’ll proceed to not just stimulate demand but also achieve sustainable economic growth led by private demand.”

The headline figure for the package totals 28.1 trillion yen, but it includes public-private partnerships and other amounts that are not direct government outlays and thus may not give an immediate boost to growth.

Abe ordered his government last month to craft a stimulus plan to revive an economy dogged by weak consumption, despite three years of his “Abenomics” mix of extremely accommodative monetary policy, flexible spending and structural reform promises.

The package comes days after the Bank of Japan eased policy again and announced a plan to review its monetary stimulus program in September, which has kept alive expectations for “helicopter money,” printing money for government debt.

The review has spooked investors, who are unsure how BOJ policy will change in the future. The price of 10-year JGB futures closed down 0.91 point on Tuesday to 151.33, having fallen 2.47 points in the last three sessions, their biggest three-day fall since May 2013.

The expected appointment of Toshihiro Nikai, an advocate of big public works spending, to the No. 2 post of Abe’s ruling party in tandem with a cabinet reshuffle on Wednesday underscores Abe’s shift toward his “second arrow” of fiscal policy amid concerns monetary easing is reaching its limits.

Precisely how the spending will be financed is unclear, although the government is considering issuing construction bonds when compiling a supplementary budget later this year. The stress on fiscal steps is raising doubts about Japan’s ability to fix its already massive debt.

The government estimates the stimulus would push up real gross domestic product (GDP) by around 1.3 per cent in the near term. The package will be implemented over several years, officials added.

SMBC Nikko Securities’ analysts expect the package will push up real GDP growth by just 0.4 percentage point this fiscal year to March 2017 and 0.04 percentage point next year.

“As effects of public works and cash payouts fade later in fiscal 2017, Japan will likely face a fiscal cliff,” said Koya Miyamae, senior economist at SMBC Nikko Securities, referring to the contraction in spending after the package wears off.

“To prevent a fiscal cliff, the government will likely repeat large-scale stimulus. Considering that a general election must be held by late 2018, direct government spending would become larger, which could further delay Japan’s fiscal consolidation goal.”

A currency dealer smiles in front of an electronic board showing the exchange rates between Euro and Japanese yen at Ueda Harlow, a foreign exchange trading company in Tokyo June 29, 2016.

(Shuji Kajiyama/AP)

Bonds shaken by BOJ stimulus doubts; dollar in decline

Wayne Cole

SYDNEY — Reuters

Published Tuesday, Aug. 02, 2016 8:59PM EDT

Last updated Tuesday, Aug. 02, 2016 9:05PM EDT

Asian shares bowed lower on Wednesday while the yen lorded over a weakened U.S dollar as talk the Bank of Japan may retreat from its massive bond-buying campaign twigged a shakeout in debt markets globally.

Worryingly for energy shares, the broad-based decline in the dollar was still not enough to spare U.S. crude oil from its first finish under $40 a barrel since April.

Adding to the jittery mood was a renewed selloff in bank stocks following stress-tests in Europe.

MSCI’s broadest index of Asia-Pacific shares outside Japan slipped 0.4 percent, backing away from its recent one-year peak. Japan’s Nikkei lost 1.4 percent as the rising yen pressured exporter stocks while financials slid 2.7 percent.

The sharpest moves were in sovereign bond markets where a sudden spike in yields stirred speculation that a multi-year bull run in prices might finally be nearing its end.

Japanese bonds have suffered their worst sell-off in more than three years as investors feared the BoJ was out of easing ammunition and might leave it to fiscal policy to stimulate the economy.

Tokyo on Tuesday approved 13.5 trillion yen ($132 billion) in fiscal measures and the IMF urged Japan to better coordinate fiscal stimulus with central bank action.

Bond bulls were now worried the Bank of England might also under-deliver at its policy meeting on Thursday, putting the onus on debt-funded government spending to support growth.

“With Japan and the UK set to ease fiscal policy, it will be important to watch whether we are at the beginning of a global policy re-pivot away from monetary easing,” wrote analysts at ANZ in a note.

The ripples spread all the way to U.S. Treasuries where 30-year yields hit their highest since July 21 even though domestic data were generally soft.

Disappointing auto sales slugged shares in Ford and General Motors, which both dropped more than 4 percent.

The Dow Jones Industrial Average fell 0.49 percent, while the S&P 500 lost 0.64 percent and the NASDAQ 0.9 percent.

The recent spate of weaker U.S. data has further pushed back expectations for when the Federal Reserve might hike its rates — the market is not fully priced for a move until 2018 — and taken a heavy toll on the dollar.

The dollar touched a five-week trough against a basket of currencies, while the euro reached its highest since mid-July around $1.1230.

Against the yen, the dollar fell to 101.16 yen having fled from 105.33 in just four sessions.

In commodity markets, oil prices were undermined by worries about a glut in both crude and refined product.

Brent crude was near four-month lows on Wednesday at $41.86 a barrel. NYMEX crude edged up 15 cents but at $39.66 was still under the psychological $40 level.

Japan household spending stubbornly weak even as jobless rate hits 21-year low

Shoppers line up in front of cashiers at the Don Quixote’s central branch store in Tokyo May 28, 2014. REUTERS/Yuya Shino/File Photo

By Sumio Ito and Leika Kihara | TOKYO

TOKYO Japanese household spending fell less than expected in July and the jobless rate hit a two-decade low, offering some hope for policymakers battling to pull the world’s third-largest economy out of stagnation.

But with the economy barely growing and inflation sliding further away from the Bank of Japan’s 2 percent target, a majority of economists expect the bank to ease further next month, when it conducts a comprehensive review of the effects of its existing stimulus program.

Household spending fell 0.5 percent in July from a year earlier, less than a median market forecast for a 0.9 percent drop and much smaller than a 2.3 percent decline in June, data from the Internal Affairs Ministry showed on Tuesday.

Separate data showed retail sales slid 0.2 percent in July from a year earlier, less than a median market forecast for a 0.9 percent drop.

The jobless rate fell to 3.0 percent in July from 3.1 percent in June, hitting the lowest rate in more than 21 years and hovering near levels considered to be full employment.

“Consumption is showing signs of a pickup, though it’s too early to judge whether the trend has changed,” said Yoshika Shinke, chief economist at Dai-ichi Life Research Institute.

“While today’s data may encouraging for the BOJ, that doesn’t necessarily mean it can stand pat as inflation remains weak,” he said.

Japan’s economy ground to a halt in April-June and analysts expect any rebound in the current quarter to be modest as weak global growth and the yen’s 20 percent rise against the dollar this year hurt exports and capital expenditure.

Consumption has stagnated even as a shrinking working-age population and gradual improvements in the economy led to a tightening job market, as companies remain wary of boosting wages for permanent workers for fear of irreversibly increasing fixed costs.

That reluctance has proved a hindrance for policymakers struggling to end two decades of deflation with aggressive monetary and fiscal stimulus measures, hoping these policies would spur expectations of future inflation and prompt households to spend more now rather than save.

Despite three years of heavy money printing by the BOJ, soft household spending and a strong yen pushing down import costs have kept inflation distant from the bank’s 2 percent target.

Core consumer prices fell in July by the most in more than three years as more firms delayed price hikes due to weak consumption, keeping the BOJ under pressure to expand an already massive stimulus program.

(Additional reporting by Izumi Nakagawa, Editing by Chang-Ran Kim; Editing by Shri Navaratnam and Eric Meijer)

By ![]()

Published: 13:14 GMT, 4 October 2016 | Updated: 13:14 GMT, 4 October 2016

The International Monetary Fund Tuesday lifted its outlook for Japan’s economy this year and in 2017, pointing to huge government stimulus spending, but warned the country’s longer-term prospects were bleak.

The Washington-based IMF upgraded its growth projections for the world’s number three economy to 0.5 percent in 2016 and 0.6 percent next year, up from a July forecast of 0.3 percent and 0.1 percent, respectively.

But the upgrade was largely due to an expected shot in the arm from a whopping 28-trillion yen ($273 billion) government spending package announced in August, as well as a decision to delay a consumption tax hike, the Fund said.

Business District Tokyo

The International Monetary Fund has lifted its outlook for Japan’s economy this year and in 2017 but warns the country’s longer-term prospects are bleak

©Kazuhiro Nogi (AFP/File)

“Japan’s medium-term prospects remain weak, primarily reflecting a shrinking population,” the IMF said in its latest World Economic Outlook.

“The probability of deflation has increased in Japan owing to weak momentum in consumer prices and the recent appreciation of the yen,” it added.

Officials are under intense pressure to deliver a boost to the economy as economists increasingly write off Prime Minister Shinzo Abe’s spend-for-growth policies, dubbed Abenomics.

Weakness in economies overseas and a strong yen, which is bad for Japan’s exporters, are weighing down growth, the Fund said.

The Bank of Japan’s huge monetary easing — a cornerstone of Abenomics — will help prop up growth for now, but would do little to fix broader problems, it added.

Among them, Japan is grappling with low birthrates and a shrinking labour force while a soaring population of old people squeezes the public purse.

Wages are stagnant, spending is faltering, and consumer prices are way below the central bank’s two-percent inflation target.

The Fund said it expected consumer prices to stay “well below” the BoJ’s inflation target for the time being.

It repeated calls for reforms including bringing more women into the workforce, boosting near-zero immigration, and trying to convince cautious firms to start spending their massive cash piles.

The Fund also called for Tokyo to rein in a national debt that is now more than two times the size of the economy — one of the world’s biggest debt loads.

A stronger yen could make emerging Asian assets relatively less attractive

© Bloomberg

October 3, 2016

Anyone who believes that the rower of the boat cannot rock it as well has not met those who run Japanese shipbuilder Kawasaki Heavy Industries.

Late last week, as part of a sharp downward revision in future earnings, the company hinted that it would shut its offshore vessels division. This would be big news — Shozo Kawasaki founded KHI 138 years ago to build ships — but it will not make a big difference. Moving more operations outside of Japan will.

KHI makes not just ships but machinery such as aerospace equipment, gas turbines and motorcycles. More than half of profits come from aerospace; shipbuilding was expected to lose money this year.

Looking at the revision — operating profits cut in half from ¥70bn — the damage from a stronger yen represents the primary cause. Almost 60 per cent of revenues come from outside Japan. Those from the US and Europe have been rising at mid-teen percentage rates annually, far better than the 1 per cent KHI gets from its home country.

KHI does make some of its goods abroad, such as rolling stock and jet skis, but it needs to do more to balance its currency risks. To be fair, its joint venture in Brazil to produce offshore drilling equipment may have been agreed with this goal in mind. Instead, a global depression for oil services coupled with the Petrobras corruption scandal killed off any hopes for a profitable business.

The Japan-based offshore marine division has become the target for change, even though the unit’s drag on profits is small. Decade-high profits in shipbuilding evaporated in 2013. Group profits, driven by aerospace, have doubled since then. Even so there is little love for KHI. That is partly because of its shipbuilding unit, which on Nomura’s forecasts will lose money until at least March 2019.

Whether KHI scuttles its offshore division is unimportant. What it really needs is to diversify its manufacturing base to more overseas locations.

Abe vows economic support to Russia; Putin to visit Japan Dec 15

Politics Sep. 03, 2016 – 06:30AM JST ( 26 )

Russian President Vladimir Putin, right, and Japanese Prime Minister Shinzo Abe shake hands as they pose for a photo during their meeting in Vladivostok, Russia, Friday. Kremlin Pool Photo via AP

VLADIVOSTOK, Russia —

Japanese Prime Minister Shinzo Abe vowed economic support to Russian President Vladimir Putin on Friday, in the hope of advancing a decades-old territorial dispute that has prevented the two countries from signing a post-World War II peace treaty.

Putin will make an official visit to western Japan’s Yamaguchi, Abe’s home prefecture, on Dec 15, Abe told reporters following his meeting with Putin on the sidelines of the Eastern Economic Forum in the Russian Far East port city of Vladivostok.

Abe, seeing his talks with Putin as the only way to achieve any breakthrough in the isles row, added they plan to meet again on the sidelines of the Asia-Pacific Economic Cooperation summit in November in Peru.

“I had substantially deep discussions about a peace treaty (with Putin),” Abe said. “To achieve a breakthrough in the abnormal situation where a peace treaty has never been concluded for over 70 years, there is no other way than finding a solution based on the leaders’ trust.”

Abe’s trip to Vladivostok was a rare visit to Russia by a leader from the Group of Seven economies, which continue to impose sanctions on Moscow, condemning Russia’s annexation of Crimea and its military intervention in the eastern part of Ukraine.

Putin’s visit to Japan was initially eyed for 2014 but was postponed after Russia’s annexation of Crimea, deteriorating ties with Western countries and Japan.

With Tokyo hoping an economic cooperation offer will prompt the Kremlin to soften its stance in the dispute over a group of Russian-controlled isles off Japan’s main northernmost island of Hokkaido, Abe laid out details of the eight-point Japanese economic cooperation plan he presented to Putin in May in the Russian Black Sea resort city of Sochi.

“I believe the development of the Far East region with big potential is Russia’s top priority issue,” Abe said at the outset of his meeting with Putin. “The growth of the Asia-Pacific leads the global economy. Japan, as Russia’s neighbor, will promote Japan-Russia cooperation in the region strongly.”

Putin said, “It is important that the governments support the initiatives of the private sector.”

The plan focuses on Japanese assistance in developing the Russian Far East, a resource-rich but underdeveloped region to which Putin attaches importance to spur growth. The Russian economy has been sluggish, hit by sanctions by Western countries and falling oil prices.

As part of the Abe government’s initiative for economic cooperation, the government-backed Japan Bank for International Cooperation and Japanese trading house Mitsui & Co signed a memorandum of understanding on Friday to acquire a 4.88% stake in Russia’s state-owned power utility RusHydro.

The move is hoped to expand opportunities for Japanese firms to make infrastructure and other deals with the Russian power sector.

In their previous meeting in Sochi, Abe said he and Putin agreed on achieving a peace treaty with a “new approach, free of any past ideas.” He did not, however, reveal any specifics regarding the path ahead.

Japanese officials said the “new approach” did not mean a change in Tokyo’s stance of claiming all of the disputed isles—Etorofu, Kunashiri, Shikotan and the Habomai islet group. The isles are called the Northern Territories in Japan and the Southern Kirill’s in Russia.

Putin has previously admitted the validity of the 1956 Japan-Soviet Joint Declaration that says Russia will return the two islands—Shikotan and the Habomai—after concluding a peace treaty with Japan.

Japan and Russia are far apart over the territorial issue. Tokyo maintains that ownership of the isles must be resolved before a peace treaty can be concluded.

Russia says the territorial and peace treaty issues are not directly connected and that it took control of the isles legitimately at the end of World War II. Moscow has strengthened its control of the islands and developed their infrastructure.

In April 2013, Abe, who took office in December 2012, became the first Japanese prime minister to officially visit Russia in 10 years, agreeing with Putin to revive territorial talks.

Since then, while Abe has made several trips to Russia, there has been no reciprocal visit by the Russian leader to Japan.

Among other matters, the two leaders also discussed issues related to the humanitarian crisis in Syria, implementation of a cease-fire agreement in Ukraine and North Korea’s missile and nuclear threats, according to a Japanese government official.

© KYODO

And when it all falls apart, some creative finger-pointing will take place. Abe can just shrug and cite sanctions if he does not get everything he wants and at bargain prices. Unless Putin does something truly daring, he will come out of this looking worse. But hey, at least he can keep hopes up through December by doing absolutely nothing. That is good work for a politician, if you can get it, and I would imagine that things have been getting a little uncomfortable for Putin lately.

Putin’s best move? Give back Habomai and Shikotan to Japan unconditionally, for free. No strings. No explanation. Just as a grand gesture of goodwill and friendship. It would literally change the world and improve EVERY SINGLE dispute and problem that Russia has today. It would literally be a new beginning for Russia.

Japan Economy, Housing Starts & Lumber Shipments

By Shawn Lawlor

Director, Canada Wood Japan

October 11, 2016

Posted in: Japan

Japan Economic Update

On the surface, with 1.37 jobs available for every worker and an unemployment rate of 3.1%, Japan’s labour market is in a relatively sweet spot globally. But the growth of temporary non-regular employment since the end of the “salaryman” lifetime employment model in the early 1990s is one of the key factors in explaining chronic sluggishness in Japanese consumption. Despite government efforts to spur growth, household consumption fell 4.6% in August – for the sixth consecutive month.

Today part-timers and non-regular contract workers represent 40% of Japan’s workforce. While average wages for private sector regular workers average 4.8 million yen annually, part-time and contract non-regular annual wages average 1.7 million. Remediating the gap in regular versus non-regular employment is key to rebuilding Japanese consumer confidence. A government panel of labour reforms is now looking at drafting recommendations for labour market reform to address this gap in benefits as well as measures to increase workforce participation of women, the elderly as well as skilled foreign laborers such as nurses and construction workers. The panel tabled its recommendations to the end of the fiscal year.

Japan Housing Starts Summary

In July, total housing starts increased 8.9% to 85,208 units. Single family owner occupied housing increased 6.0% and rental housing jumped 11.1%. The mansion condominium market improved 5.9%.

Total wood housing increased by 11% to 48,693 units. Post and beam starts improved 10.9% to 36,206 units. Wood pre-fab starts were up 11.4% to 1,383 units. Thanks to particular strength in multi-family, platform frame starts posted an 11.3% gain to 11,104 units. By housing type 2×4 custom ordered single family homes edged up 2.2% to 2,945 units; rentals surged 18.3% to 6,956 units and built for sale 2×4 spec housing declined 0.3% to 1,192 units.

BC Wood Exports Summary BC Investment and Innovation

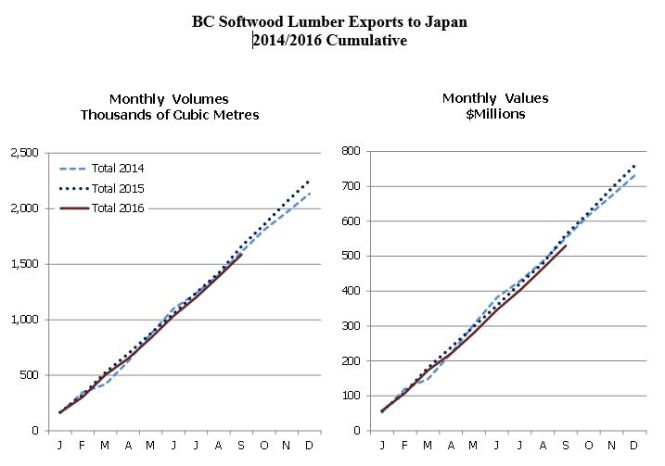

As of the end of August, British Columbia year to date softwood lumber exports to Japan totaled 1,389,931m3: an increase of just under 1%. By value, year to date exports totaled $465.1 million – a decrease of 2.14% compared to year prior results. By species groups, SPF fared comparatively well. Between January and August, SPF shipments increased 6.2% to 1,088,275m3; Hemlock decreased 4.1% to 174,098m3, Douglas Fir fell 15.6% to 138,184m3 and Yellow Cedar fell 22.1% to 41,474m3.

China’s Macroeconomy: Time Series Data from Center for Quantitative Research

Federal Bank of Atlanta https://www.frbatlanta.org/cqer/research/china-macroeconomy.aspx?panel=1

Since the late 1990s, China’s investment share of gross domestic product (GDP) has increased while the corresponding shares for consumption and both labor and household income have declined (Chart 1). These changes in trends have been accompanied by sharp changes in cyclical patterns as well; as shown in Chart 2, the strong positive correlation between investment and household consumption broke down in the late 1990s. The model laid out in “Trends and Cycles in China’s Macroeconomy,” by Chun Chang, Kaiji Chen, Daniel F. Waggoner, and Tao Zha, can account for these facts. The authors argue that these changes began in March 1996, when the Eighth National People’s Congress passed a historic long-term plan to adjust the industrial structure for the next 15 years in favor of strengthening heavy industries. Preferential credit policies to heavy industries—where local governments have made implicit guarantees of long-term bank loans to that sector—have crowded out short-term loans to smaller firms. Consistent with this crowding-out effect, Chart 3 shows that the correlation between short-term loans and medium- and long-term loans as shares of GDP has been negative since the early 1990s.

This webpage hosts the annual and quarterly macroeconomic datasets for China used by Chang, Chen, Waggoner, and Zha. Technical details on sources and methods used to construct the datasets are described in the manuscript “China’s Macroeconomic Time Series: Methods and Implications,” by Patrick Higgins and Tao Zha. A readme file includes variable names and descriptions as well as instructions on how to use the datasets. We plan to make regular semi-annual updates to the datasets and maintain earlier vintages.

Related Resources

- Current data – March 16, 2016 (Zip File)

- April 15, 2015 Vintage, Used in NBER Paper (Zip File)

- The China Time Series Manuscript

- Working Paper 2015-5

- VOX article: “Trends and Cycles in China’s Macroeconomy”

- Tao Zha’s web page

- Patrick Higgins web page

- Daniel Waggoner’s web page

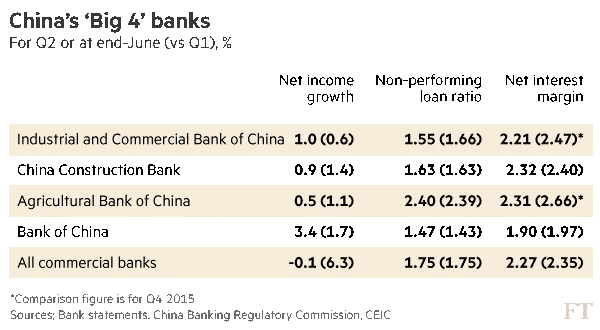

Bad loan growth slows at China banks as write-offs accelerate

Big lenders brace for fallout from government efforts to rein in debt

August 30, 2016

by: Gabriel Wildau in Shanghai

Growth in bad loans slowed at Chinese banks in the second quarter as lenders stepped up writedowns and the economy of the country’s prosperous east coast showed signs of stabilising.

After years of fast profit rises driven by aggressive lending in support of China’s manufacturing and construction booms, the big four lenders are pulling in their horns as they brace for fallout from government efforts to rein in debt and cut rampant overcapacity in basic material sectors.

Industrial & Commercial Bank of China, the country’s largest lender by assets, on Tuesday reported net profit growth of 1 per cent for the second quarter, little changed from 0.6 per cent growth in the first quarter.

Industry-wide profits fell 0.1 per cent in the second quarter from a year earlier, compared with 6.3 per cent growth in the first quarter and 2.4 per cent in 2015. Small banks have maintained fast profit growth as they expand assets more aggressively than larger rivals.

But growth in non-performing loans moderated. The NPL ratio for China’s commercial banking system was 1.75 per cent at the end of June, unchanged from three months earlier, while ICBC’s ratio actually fell to 1.55 per cent from 1.66 per cent three months earlier. (A nonperforming loan (NPL) is the sum of borrowed money upon which the debtor has not made his scheduled payments for at least 90 days. A nonperforming loan is either in default or close to being in default.)

China’s three other largest banks — Bank of China, Agricultural Bank of China and China Construction Bank — each reported NPL ratios at end-June that were little changed from three months earlier. Bad loans continued to rise in volume terms, hitting 1.44tn ($215bn) for all commercial banks at end-June, up by Rmb44bn since March.

“The NPL formation rate was slower than people thought. That’s the biggest surprise in these figures,” said Ma Kunping, banks analyst at China Merchants Securities in Shanghai. “The economy in the east coast has basically hit bottom. Most of the problem companies have already been exposed.”

Banks’ net interest margin — which measures the difference between what lenders pay for deposits and what they collect on loans — fell to the lowest on record in the second quarter at 2.27 per cent. China’s benchmark lending rate is at an all-time low of 4.35 per cent for one-year loans, and interest rate deregulation has also forced lenders to compete with each other on deposit and loan pricing.

Analysts warn that NPLs will probably resume rising in the coming quarters, with north-east China’s coal and steel industries a major source of delinquencies. That will show up not only in rising NPLs, but also in loan restructurings and debt-for-equity swaps that will help troubled companies but impair bank balance sheets.

In addition to slower NPL formation, lenders have become more aggressive in writing down and selling off bad loans.

AgBank, the country’s third-largest, said on Friday that it had disposed of Rmb60bn in bad loans in the first half, which is equivalent to 28 per cent of the bank’s outstanding NPLs at the end of 2015.

“Though credit quality pressure is likely to persist for some time … [AgBank’s] strong capacity in NPL digestion should help to alleviate concerns about book impact from NPLs,” Richard Xu, China financials analyst at Morgan Stanley, said in a note.

Investors remain concerned about a further rise in NPLs, with shares of all of the big four banks currently trading below book value in both Hong Kong and Shanghai, reflecting scepticism about the reported numbers.

Regulators are preparing new rules to curb banks’ ability to package loans into wealth management products, which will help to reduce systemic risk but add to pressure on bank profits.

NSG, China-Pakistan economic corridor on table during Narendra Modi-Xi Jinping meeting

By IANS | Sep 03, 2016, 01.41 PM IST

Narendra Modi will once again try to persuade Xi Jinping to back India for membership of the 48-member NSG — an exclusive grouping that controls global nuclear trade.

HANGZHOU: India’s entry into the Nuclear Suppliers Group (NSG) and its concern over the China-Pakistan Economic Corridor (CPEC) are expected to be raised by Prime Minister Narendra Modi when he meets with Chinese President Xi Jinping on the sidelines of the G20 Summit in Hangzhou here on Sunday. Though India is set to push for structural reforms to shore up the flagging global economy, poverty and green finance among others in the forum of the world’s largest 20 economies, Modi will once again try to persuade Xi to back India for membership of the 48-member NSG — an exclusive grouping that controls global nuclear trade. In June, Modi had, during a meeting with Xi in Tashkent on the sidelines of the Shanghai Cooperation Organisation summit, asked for China’s backing for India’s NSG membership. But China, leading a group of 10 countries, blocked India’s entry at the plenary of the NSG in Seoul in June, citing New Delhi’s non-signatory status to the Nuclear Proliferation Treaty. Beijing has, however, been a keen backer of Islamabad’s entry to the bloc. Intransigent then, Beijing now looks amenable to India’s admission into the elite grouping. Modi is to reach Hangzhou, the capital and most populous city of Zhejiang Province in east China, on Saturday evening to attend the two-day summit that begins on Sunday.

Chinese experts hope the meeting between the two leaders would be “good”. “We are not against India’s entry into the NSG. After the Chinese Foreign Minister’s (Wang Yi) visit to India (in August), the two sides have agreed to establish a new channel to touch upon all these kind of issues,” Hu Shisheng, director, Institute of South and Southeast Asian and Oceanian Studies at the China Institute of Contemporary International Relations, a government think tank, told IANS. He was referring to the new “mechanism” between India and China under which Joint Secretary of Disarmament Division Amandeep Singh Gill and Ambassador Wang Qun, Director-General of the Arms Control Division of the Chinese Foreign Ministry, will discuss the NSG issue. “It’s because not to let these issues bother the top leaders (Modi and Xi). Earlier, they could not reach understanding because of lack of information. I hope the meeting would be good,” he added. Asked if China would be more open to India’s admission to the NSG, Hu said: “Of course”. The change in Beijing’s stance may also have to do with a UN court ruling on the South China Sea dispute in July. The rejection of Beijing’s claims over the so-called Nine Dash line — almost 90 per cent of the disputed South China Sea — was a blow to China in its dispute with the Philippines, as also Vietnam, Malaysia, Taiwan and Brunei. China has rejected The Hague Court’s ruling. India asking the “parties concerned to show utmost respect to the UN Convention on the Law of the Sea (UNCLOS) has sort of miffed China”, which is worried about its image being sullied in the world. It has been suggested that Chinese Foreign Minister Wang Yi’s visit to India last month was to ensure that New Delhi does not raise the South China Sea issue at the G20, in a sort of quid pro quo deal — which could see Beijing giving its backing for the NSG membership. However, even if India keeps quiet on the issue, the US and Japan are highly likely to bring it up, much to the embarrassment of China which has said an emphatic no to “political discussion” at the G20. The $46 billion China-Pakistan Economic Corridor is also likely to figure in the meeting between the two leaders. India has strongly opposed the proposed economic corridor which will pass through Pakistan-held Kashmir and Gilgit-Baltistan, which New Delhi claims as its own. Modi’s reference to the two regions, as well as Baluchistan, in his Independence Day speech has Beijing worried. Beijing fears New Delhi’s tacit support to the separatist sentiment in the region — a charged levelled by Islamabad and denied by New Delhi — may hit the already-delayed project. Chinese experts have warned that China may come to Pakistan’s aid if India creates trouble in these regions. Besides, global structural reforms, inclusive growth and climate financing will be the major issues to be brought up by India at the summit. “There will be emphasis on appealing to the countries to carry forward the commitment to the issue of climate change and climate change finance. There was a $100 billion commitment which has been made by developed countries — that $100 billion is nowhere near sight. We would like to again stress the importance of developed nations making available that $100 billion,” Shakitanka Das Economic Affairs Secretary told IANS earlier.

China’s Southern Megacities Roll Out Measures to Cool the Property Market

China’s southern megacities of Guangzhou and Shenzhen are the latest centers to impose new measures to cool their overheated real estate markets, including higher mortgage down payments and home purchase restrictions.

A property boom has given a welcome boost to China’s economy this year, fueling demand for everything from construction materials to furniture, but a growing buying frenzy is adding to worries about ever-rising debt and risks to the banking system.

The new measures are the latest steps to tighten credit flowing into the property sector as the government tries to balance the need to prevent bubbles while stimulating economic growth.

Prices for new homes in the booming tech centre of Shenzhen rose 36.8% from a year ago in August, while Guangzhou’s new home prices rose 21.1% over that period, National Bureau of Statistics (NBS) data showed.

Other cities including Chengdu, Jinan, Wuhan and Zhengzhou have already announced new restrictions on property purchases as the government tries to dampen prices stoked by property speculators in second- and third-tier cities across the country.

The average new home price in 70 major cities climbed an annual 9.2% in August, up from 7.9% in July, according to the National Bureau of Statistics.

Nomura analysts said the new measures were expected to help cool frothy prices in the biggest cities and should prevent the market frenzy from spilling over into smaller cities.

“We also believe it unlikely that the latest tightening measures will cause the bubble to burst, sparking a collapse of home prices. We envision a more likely scenario to be a mild retreat or prolonged flattening of home prices in tier-1 cities,” they said in a note on Tuesday.

First-time home buyers in Shenzhen will face minimum down payments of 30%, but deposits for others will be raised to no less than 50%, state news agency Xinhua quoted a government document as saying.

Down payments for second-home buyers in China’s southern Guangdong province near Hong Kong will be increased to no less than 70%, Xinhua said without giving further details.

For more on real estate, watch Fortune’s video:

China’s southern city of Guangzhou has limited local residents to purchasing a maximum of two properties, according to a statement posted late on Tuesday on the Guangzhou government’s website.

Non-local residents will be allowed to buy one property, if they can prove they have paid appropriate levels of tax or social security.

Separatel

Risk of hard landing persists

By Brad Spencer

Senior Director, Support Services

October 13, 2016

Posted in: China

Economic forecasting is a challenging task at the best of times. For a non-standard economy like China, it is even more difficult; the government has more levers of influence, policy changes are not part of the public dialogue and indicators are less transparent.

Some of the best insights we have available come from the Economist Corporate Network and the affiliated Economist Intelligence Network. We recently attended several events in Shanghai, where analysts from the Economist explained their views on China’s GDP growth, the property markets and exchange rates.

GDP Growth

The Economist trimmed their prediction for 2016 from 6.7% to 6.6%. They see growth slowing further in 2017 and again in 2018. The reason for this pessimistic forecast is that China has not implemented the promised economic or political reforms. These reforms are necessary to buoy productivity. In particular, reform of state owned enterprise (SOE) has not taken place nor is it likely to happen with so many political obstacles. SOE’s control and limit the opportunities for private investment. Private investment always has better ROI than government investment. Debt is another factor, and over investment in property and in steel are yet another factor.

China’s economy is growing at two speeds: the manufacturing sector is struggling to expand, but the consumer driven services sector is thriving. As the engine of growth shifts from manufacturing to services further periods of volatility are certain. The Economist puts the risk of a hard landing at some point in the next five years at 40%. A hard landing is defined as a drop of 2 + percentage points in annual economic growth compared to the previous year.

Economic activity so far in 2016 has been driven by strong housing market activity and investments in SOE’s, but neither driver is expected to perform strongly in the second half of the year.

Property

Top tier cities continue to boom while smaller cities are flat. Rising values in Shanghai and Beijing are driven by demand for investments, not demand for accommodation. This is not a new trend, but the trend has continued beyond what was expected.

Bank lending is increasing, as is the level of speculation and risk. Some analysts are expecting government intervention to calm the over-heated markets. In the meantime, this investment is driving property development growth in select cities.

Exchange rate

The RMB is expected to weaken between now and 2020. There are interesting forces at play with new policies in place to prevent currency from flowing out of the country, and resourceful investors constantly seek loopholes. The government aims to maintain a stable currency, but the forces of gravity are pulling at the RMB.

2016 forecast RMB/USD 6.55

2017 forecast RMB/USD 6.76

China just made a key preparation for disaster in its economy

September 23, 2016

china bunker

(Reuters) China has given its bond traders the go-ahead to begin trading credit default swaps, an indication that the government is preparing for more big corporate bankruptcies, Bloomberg reports.

Credit default swaps allow investors to insure themselves against the default of a given security.

Earlier this month, the government for the first time allowed a major state-owned organization, Guangxi Nonferrous Metals Group, to make preparations for bankruptcy.

It was a special moment. Never before had the country allowed a big, state-run industrial company to go bust. Past bankruptcies involved only bank or corporate debt — this one involves 108 creditors.

That news, combined with the trading of credit default swaps, has analysts believing that many so-called zombies — China’s unproductive, massive industrial companies that need debt to survive — may soon be put out of their misery.

Credit default swaps “will help investors mitigate the risk and alleviate market sentiment if investors face more defaults or suffer more losses after defaults,” Ivan Chung, head of Greater China credit research at Moody’s Investors Service, told Bloomberg.

In other words, investors can now bet on whether a zombie is about to go bankrupt, giving themselves a little extra protection if a company fails. And the government opening up the market for credit default swaps suggests more willingness to let zombies die.

China has had the zombies in its crosshairs for some time now. In 2015, the government said supply-side reform would become central to its economic policy. This is because China is trying to take its economy through the delicate transition from one based on industry and manufacturing sectors to one based on domestic consumption and services like banking and retail.

That means indebted companies in flailing industries like coal and steel must be restructured and their overcapacity dealt with. Unleashing a market for credit default swaps means that investors can hedge this transition and better navigate a world of rapidly deteriorating corporate credit quality.

We might be about to see some real winners and losers here, people.

China economy, construction & lumber shipments

By Eric Wong

Managing Director, Canada Wood China

November 9, 2016

Posted in: China

CHINA ECONOMIC UPDATE

September economic highlights

- China’s economy remained steady in September

- Real estate investments up compared to same period last year

- In September, China’s overall wood imports increased compared to the same period last year, but Canadian imports fell.

China economic overview

The Chinese GDP growth rate in Q3 2016 remained at 6.7%, meeting market expectations, which pegged GDP growth at 6.6%. Analysts believe steady growth was spurred by increased government spending (12.5% growth year-on-year), larger asset investments (8.2% growth year-on-year) and an increase in retail sales (10.7% growth year-on-year).[i]

China Caixin PMI increased to 51.2 in October 2016 compared to 50.1 in September, marking the fourth consecutive month of growth and the highest number since July 2014[ii]; this was also the fastest improvement since March 2011. The government’s official services PMI reached 54.0 in October, showing a steady increase compared to September (53.7) and August (53.5). It appears China’s economic performance is currently surpassing expectations.

China exports declined 10% year-on-year to USD 184.51 billion[iii] and imports fell 1.9%; this set the September trade surplus at USD 41.99 million. In Yuan terms exports declined 5.6% compared to the same period last year and imports were up 2.2%. “Domestic demand is equally weak as global demand,” said Yifan Hu the chief investment officer at UBS Wealth Management, mentioned without the increase in the price of oil from USD 30 a barrel in September 2015 to USD 50 last month imports could be even weaker, and a small depreciation does not help China’s exports.[iv]

China’s September Consumer Price Index (CPI) bounced back to average levels at 101.90 Index Points after August (101.30), which marked the lowest in a year.

The USD exchange rate against the RMB decreased 0.08% to 6.7673 on November 4th 2016 from 6.7729 in the previous trading session. Overall USD/CNY increased steadily this year, starting from 6.58 (January) and decreased slowly to 6.47 (April) and then brought back to 6.77 (October)[v], it added 6.82% during the last year.[vi] On the other hand in 2016 CADCNY kicked off by 4.71 (January) and reached all the way to 5.16 (April) but then dropped almost continuously to 5.09 (July and August) and 5.05 (October)[vii].

REAL ESTATE CONSTRUCTION MARKET

The first three quarters of 2016 reached RMB 7,460 billion, marking a 5.8% growth (year-on-year) in real estate investments. Investments in residential were RMB 4,993 billion (+5.1% year-on-year), accounting for 66.9% of total real estate investments. In September 2016, RMB 1,021 billion was invested in national real estate industry including RMB 686 billion for residential sector.

Construction: floor area started

From January to September 2016 floor area of newly built buildings (floor area started) reached 1.23 billion m2 (+6.8% year-on-year), of which 847 million m2 was in residential sector (+6.7% year-on-year).[viii] In the same period, total floor area of finished buildings grew to 571.12 million m2 (+12.1% year-on-year), of which 420.68 million m2 was in the residential sector (+11.3% growth year-on-year).

In September floor area of newly built buildings (floor area started) nationwide reached 158 million m2 including 111 million m2 for residential buildings. In the same month floor area of finished buildings nationwide increased to 65 million m2 including 48 million m2 for residential buildings.

Policy developments

China’s housing frenzy is still on, concluded by Business Insider in September 2016. Even though 53.7% respondents in a survey conducted by People’s Bank of China believed home prices in China are “high and hard to accept” the percentage of residents willing to buy a place in the next three months still increased 1.3% from the third quarter and reached 16.3%.[ix] The property price of China’s 100 major cities rises 14% year-on-year which is above GDP growth or urban income growth in the past 12 months, not all of those cities have many new migrants to consume new housings either.[x]

China’s Central Economic Work Conference will hold a meeting in December 2016 to provide further signal of policy direction, may be an answer to the extent China can tolerate continuously rising housing prices. There might not be any major intervention in the property market in the next several months until the late 2017 when the 19th Party Congress Session begins. The plan drafted by policy makers from Beijing to expand investment channels to transfer investment away from property market may not work because hard correction could cause a major financial crisis. The Economist Intelligence Unit predicts China property market will grow much slower in 2018 declining to 4.2%.[xi]

Building material prices

Regarding common building materials, price for cement in China increased 2.32% from RMB 279.83 per metric ton on October 1st to RMB 286.33 per metric ton on October 31st [xii]; rebar steel was worth RMB 2,336 per metric ton on October 1st and then increased 4.08% to RMB 2,431.33 per metric ton on October 31st [xiii].

WOOD EXPORT TO CHINA

In September, China’s wood imports increased compared to the same period last year, including:

- In September log imports were 4.26 million m3 (+15.41% year-on-year); the total for January to September was 36.59 m3, which marks a 6.95% increase compared to the same period last year.

- September imports of lumber amounted to 2.53 million m3 (+17.4% year-on-year). Total imports of lumber January to September amounted to 23.73 million m3, marking a 19.43% increase compared to the same period last year. However, imports of Canadian softwood lumber are down 10.99%.[xiv]

WOOD MARKETS predicts that the total volume of China softwood lumber imports will be 14,098,000 m3 in 2016 with 20.2% change YTD; 42.4% change YTD for Russian softwood lumber and -11.6% change YTD for Canadian softwood lumber. Regarding the price of SPF lumber (S4S, KD) CIF Taicang (Shanghai), #2 grade in 2X4 stays at $201/ m3 to $206/ m3 for over 4 months but Utility grade (#3) and #2 grade both in 2X6 increased $17/ m3 and $20/ m3 to $187/ m3 and $216/ m3 respectively dramatically in just one month.[xv]

[i] Trading Economics (October 2016). China GDP Annual Growth Rate

[ii] Trading Economics (October 2016). China Caixin Manufacturing PMI

[iii] Trading Economics (October 2016). China Exports

[iv] Leslie Shaffer (October 12th, 2016). China’s September exports and imports tumble amid weak demand, yuan decline.

[v] Finance Sina (October 2016). USDCNY

[vi] Trading Ecnomics (October 2016). Chinese Yuan

[vii] Finance Sina (October 2016). CADCNY

[viii] National Bureau of Statistics ( October 19th, 2016)

[ix] Business Insider (September 25th, 2016). China’s housing frenzy is still on.

[x] Economist Corporate Network 2016 (October, 2016). Up in the air, China’s property market

[xi] Economist Corporate Network 2016 (October, 2016). Up in the air, China’s property market

[xii] Sunsirs (October 2016). Spot Price: Monthly for Cement

[xiii] Sunsirs (October 2016). Spot Price: Monthly for Rebar

[xiv] BOABC (November 4th, 2016). China Wood and its products market monthly report Issue 213

[xv] WOOD MARKETS (October 2016). China Bulletin

BC Forest Investment and Innovation China Data to September 2016 compared to 2014, 2015 1nd 2016

IMF cuts GDP growth forecast for Taiwan

2016/10/04 22:33:09

CNA file photo

Washington, Oct. 4 (CNA) The International Monetary Fund (IMF) has adjusted downward its economic growth forecast for Taiwan for this year and next, to 1.0 percent and 1.7 percent, respectively. In its World Economic Outlook (WEO) released Tuesday, the IMF cut its 2016 and 2017 forecast for Taiwan by 0.5 percent from its previous respective forecasts of 1.5 percent and 2.2 percent, which was released in April. With such lackluster performance, Taiwan’s economy will do better than only Japan and Macau in Asia, while lagging behind its former “Asian Dragon” rivals — South Korea, Hong Kong and Singapore. The IMF’s forecasts for these Asian Dragons this year and next are 2.7 percent and 3 percent for South Korea, 1.4 percent and 1.9 percent for Hong Kong, and 1.7 percent and 2.2 percent for Singapore. Japan’s economy will grow only 0.5 percent and 0.6 percent this year and in 2017 mainly because of its shrinking population, according to the IMF. The WEO report noted that the Philippines will outshine its Association of Southeast Asian Nations partners by achieving growth of 6.4 percent and 6.7 percent in 2016 and 2017, outdoing Indonesia, Thailand, Malaysia and Vietnam. (By Rita Cheng and S.C. Chang) ENDITEM/J

Australia’s economy

Good on you

Australia has weathered the China slowdown and commodities slump well. What has it done right?

Sep 3rd 2016 | SYDNEY | From the print edition

Girder on you, too

THE last time Australia was in recession, Mikhail Gorbachev led the Soviet Union and Donald Trump had filed for Chapter 11 only once. Barring unforeseen catastrophe, late next year Australia will pass the Netherlands’ modern record of 26 years of consecutive growth—despite the slowdown of its biggest trading partner, China. Unlike most of the rich world, it sailed through the global financial crisis, and unlike most commodity exporters, it has weathered the raw-materials price slump. Its GDP growth rate of 3.1% dwarfs that of America and the euro zone.

Australia is often called “the lucky country”, and luck, particularly in geology and geography, has played a part in its success. But it has deftly played both sides of the China boom: the surging demand for raw-material imports while that lasted; more recently, the desire of the Chinese middle-class to eat well, travel and educate their children in English. Yet every silver lining has a cloud. Not only does Australia have one of the most expensive housing markets in the world, it remains overexposed to the fortunes of China.

The story of Australia’s success starts with what its government did not do: spend beyond its means. Tight budgets in the late 1990s and early 2000s, combined with improving terms of trade, meant that when the financial crisis hit, the government was running budget surpluses (though the country as a whole has a long-running current-account deficit). It could thus afford stimulus packages in late 2008 and early 2009 worth more than A$56.6 billion ($42.8 billion). Only China provided greater stimulus as a share of GDP.

Australia was then in the middle of the biggest mining boom in its history, stemming from increased demand in China. In the decade to 2012, the value of its mined exports tripled; mining investment rose from 2% of GDP to 8%. From January 2003 to February 2011 the price of iron ore, which these days comprises 17% of Australia’s exports by value, rose from $13.8 to $187.2 a tonne. Australian thermal coal, which accounts for 12% of its exports, rose from $26.7 to $141.9 (down from a peak in 2008 of $192.9).

The Reserve Bank of Australia (RBA) estimates that, during that period, mining raised real disposable household income by 13% and wages by 6%, boosting domestic purchasing power. Saul Eslake, an independent economist, argues that “except for the Chinese people, no country derived more benefit from the growth and industrialization of China” than Australia. The value of the Australian dollar also rose, which dented non-mining exports. But since demand from Asia kept prices high for Australia’s agricultural commodities (such as beef and wheat), and because it exports relatively few manufactured goods, the damage was contained.

As China rebalanced and commodity prices tumbled, other exporters such as Russia, South Africa and Brazil fell into recession. In Australia, although business investment has fallen sharply, GDP growth remains near its 25-year average of 3% (and as a side benefit, the commodity-price fall quelled rising inflation).

For that, thank two factors. First, the rise in mining investment during the fat years led to increased production. Commodity exports have continued to grow (albeit modestly and less profitably). Though prices of iron ore and coal are well below the past decade’s peaks, they remain above pre-boom levels.

More important, Australia let the dollar depreciate, which made its exports more appealing. Today Australia benefits from a growing number of Chinese consumers, who buy Australian food products that are widely seen as safer than their home-grown equivalents.

Middle-class Asian students have been flocking for English-language education to Australian universities, which are closer and cheaper than their American and British counterparts. Between June 2015 and June 2016 the number of international students enrolled in Australian colleges and universities rose by 11%, and the number of international visitors rose by 13.7%. Today education and tourism together account for 14% of Australia’s export value. Graduates are eligible to work for up to four years, and some stay longer, giving Australia a relatively young, well-educated, multicultural workforce.

Those workers will need places to live, which has helped increase house construction. According to Paul Bloxham, the chief Australia and New Zealand economist at HSBC, Australian builders completed almost 200,000 new dwellings last year, and will probably do the same this year and next. Construction has absorbed some of the employment losses as mining investment has waned (building a mine requires more people than running one).

Yet that has failed to stop an alarming rise in house prices, particularly on Australia’s east coast. In 2015 the median house price in Sydney was 12.2 times the median income, up from 9.8 in 2014. Melbourne’s multiple rose from 8.7 to 9.7 in that period. Some argue that house prices have peaked, and that as residential construction continues prices will moderate (except perhaps in central Sydney). But if prices collapse, that could not just harm Australia’s otherwise healthy banks, but also dampen domestic consumption for years.

Some argue that government debt, which has hit a record 36.8% of GDP, up from a low of 9.7% in 2007, is another worry, because it provides less policy room to deal with the next crisis. It remains lower than in most developed countries. But given the risks of a housing bust or deeper slowdown in China, such worries reflect a healthy lack of complacency. After all, one day the luck will run out.

y, local media reported on Tuesday that Suzhou in China’s eastern Jiangsu province had unveiled fresh measures steps, including higher down payment requirements, to cool the housing market.

Hanjin Shipping: decked

Even state-backed lenders are now wary of the container shipper

© Getty

August 30, 2016

It is quite a moment. Korea’s state-backed development bank has declined to support the restructuring plan of the country’s biggest shipping company. Bankruptcy looms. Anyone hoping this heralds an outbreak of common sense in the oversupplied container shipping market will be disappointed.

Korea Development Bank said on Tuesday that Hanjin Shipping’s restructuring plan would not solve its cash crunch. Hanjin’s shares shed another quarter before being suspended. It now has until September 4 to get its finances in order or enter creditor protection.

Hanjin could yet be salvaged. Smaller rival Hyundai Merchant Marine is already in the process of a debt-for-equity swap, and shipping is a politically important industry in Korea. But Hanjin’s predicament is arguably worse than Hyundai’s. The former has not made a net profit (after minority interests) since 2010 and debt — much of which falls due in the coming year — is more than seven times its equity. Shaky finances mean Hanjin could be excluded from THE Alliance, a new group of shipping lines set to form next March, which wants to share vessels and cut costs. Ideally, Hanjin would be allowed to fail and many of its ships would be scrapped.

That is unlikely, even if it does go bust. About half of its fleet is chartered, according to Alphaliner, so the owners of those ships will simply offer them elsewhere, even if that means accepting lower rates. And in the global pecking order Hanjin is low with just 3 per cent of global capacity — small on the surplus deck space of the wider industry.

Consolidation is unlikely to help either. The recent combinations of Hapag-Lloyd with UASC and CMA CGM with Neptune Orient were more about bigger fleets and lower costs than reducing tonnage.

That leaves the industry waiting for demand to catch up with supply, which could take several years. Three crumbs of comfort: there has been a slight improvement in rates, fuel costs remain subdued, and the supply of ultra-cheap money that financed frantic overbuilding has finally been curtailed — as Hanjin may now discover to its cost.

South Korea Injects 65 Trillion Won To Revitalize Economy in 2017

by Karen Lydelle Linaja / Sep 03, 2016 09:21 AM EDT

South Korea Injects 65 Trillion Won To Revitalize Economy in 2017

South Korea will inject more than 65 trillion won to revitalize the momentum of the economy in 2017 due to rising uncertainties and faltering exports in the global market.

The Korean government set aside more than 16 percent of the total budget of 400.7 trillion won to revitalize the economy, boost exports and support small- and mid-sized enterprises (SMEs).

Some of the 600 billion won which increased by 42.5 percent from the previous year was assigned for boosting exports according to the ministry of Trade, Industry and Energy.

Advertisement

There is a record of 19 consecutive months of losing streak in January last year. However, the outbound shipments of South Korea increased a 2.6 percent in August.

Because of the slowdown of the world economy and financial turmoil appeared in a US rate hike, experts remained alarmed in the situation. The South Korean government plans to create an export voucher program worth 177.8 billion won that will give consulting services and other benefits to the troubled local exporters in the country.

Moreover, a total of 8.1 trillion won will be set aside to foster SMEs in 2017 with 2.4 trillion won for the start-ups and venture firms. Some of the 15 billion won will be used to advertise exports of potential sectors like fashion, cosmetics, and pharmaceutical.

Hyundai Heavy Industries Co. and Daewoo Shipbuilding & Marine Engineering Co., who are the industry leaders, will lead the local shipbuilding sector with a budget of 1.7 trillion won that faces massive layoffs and contracted demand.

The bulk of the 2017 budget will be spend on expanding the transportation network, providing jobs, and creating urban re-development projects.

IMF: S. Korean Economy to Grow 3% Next Year

The International Monetary Fund (IMF) has predicted that South Korea will recover to the three percent economic growth level next year. In its latest World Economic Outlook report released on Tuesday, the IMF said the South Korean economy will grow two-point-seven percent this year and three percent next year. They are the same figures suggested for the country in an IMF report released in July ahead of the G-20 Finance Ministers and Central Bank Governors’ Meetings. The South Korean government also forecast earlier that its economy will grow three percent next year, although it is more positive about this year’s expansion than the IMF, offering a two-point-eight percent growth target. The Organization for Economic Cooperation and Development (OECD) also predicted an expansion of three percent for South Korea next year.

Korean Economy, Housing Starts & Lumber Shipments

By Tai Jeong

Technical Director, Canada Wood Korea

November 17, 2016

Posted in: Korea

Economic Update

The South Korean economy, internally constrained by sluggish consumption and investment, is also surrounded by growing external risks. The export-driven economy, in particular, is significantly dependent on its two biggest trading partners, the US and China. The most immediate point of uncertainty for the Korean economy, especially on trade, is the US presidential election.

South Korea posted a trade surplus for 57 straight months in October as imports fell at a faster pace than exports. Exports fell 3.2% on-year to US$42 billion in October, while imports retreated 4.8% to US$35 billion resulting in a US$7 billion trade surplus, up 5.7% from a year earlier.

South Korea’s consumer prices rose 1.3% on-year in October, marking the highest monthly gain since February amid concerns over potential deflation.

South Korea’s unemployment rate rose 3.4%, the highest for the month since 2005, in October from a year earlier, with the unemployment for young people still remaining high on a lingering economic slump.

The exchange rate for Canadian Dollar averaged at 849.90 won in October, 2016, down by 3.14% from 877.42 in October, 2015 and slightly up by 0.32 % from 847.18 in one month earlier.

Housing Starts

South Korea’s housing starts in year-to-date September of 2016 increased 3.7% to 86,726 buildings from a year earlier 83,640 buildings. Housing permits in the same period also increased 7.1% to 98,123 buildings from a year earlier 91,613 buildings, amid the South Korean government’s continuous efforts to prop up the local real estate market.

The number of wood building permits and wood building starts year-to-date September of 2016 also increased 10.6% to 12,517 buildings and 11.5% to 11,116 buildings, respectively, compared with those in 2015. The noticeable things are both total floor areas of wood building permits and starts in the same period of 2016, remarkably increased to 14.8% and 16.1% to 1,108,219 m2 and 1,000,772 m2, respectively, from a year earlier.

South Korea’s home transactions gained 2.2% from a year earlier in October amid an apparent rise in demand triggered by a government plan to limit the supply of new homes.

The number of home transactions came to 108,601 in October, compared with 106,274 in the same month last year.

By housing type, home transactions involving apartment units gained 5.8% on-year to 74,208, while those involving row houses slipped 1.6% to 20,202, with transactions involving detached houses plunging 9.1% to 14,191.

Lumber Shipments

BC softwood lumber export volume to South Korea for the first nine months of 2016 increased 6% to 212,602 cubic meters as compared to 200,468 cubic meters for the same period of 2015.

Export value for the same period of 2016 also increased 2.8% to CAD$55.847 million as compared to CAD$54.342 million in 2015.

For the year-to-date to September of 2016, BC’s SPF shipment to South Korea increased 7% to 202,322 cubic meters while shipments of Hemlock, Western Red Cedar and Douglas-Fir plunged 27.8%, 55.8% and 68.6% to 4,985m3, 862m3 and 657m3, respectively.

Indian schoolchildren stand in front of a store window offering discounts in Mumbai on August 3, 2016. (INDRANIL MUKHERJEE/AFP/Getty Images)

Indian parliament passes GST law, causing companies to panic

MANOJ KUMAR and DOUGLAS BUSVINE

NEW DELHI — Reuters

Published Wednesday, Aug. 03, 2016 4:57PM EDT

Last updated Wednesday, Aug. 03, 2016 5:00PM EDT

Throughout years of political gridlock, the risk that India might pass its biggest tax reform since independence appeared reassuringly remote for many businesses.

Until now.

Suddenly, the prospect that a new Goods and Services Tax (GST) could enter force next year has bosses panicking at the likely impact and seeking advice on how to cope.

The passage by parliament on Wednesday of a key constitutional amendment would resolve crucial issues needed to transform India’s $2-trillion economy and 1.3 billion consumers into a single market for the first time.

Yet the vote will only fire the starting gun in a legislative marathon in which the national parliament and India’s 29 federal states have to pass further laws determining the – still unknown – rate and scope of the tax.

At the same time, a huge IT system needs to be set up, tax collectors trained and companies brought up to speed on a levy that experts say will force them to overhaul business processes from front to back.

One boss who isn’t ready is G.R. Ralhan, head of Roamer Woollen Mills in the northern city of Ludhiana.

“Companies, particularly smaller ones, are apprehensive,” Mr. Ralhan told Reuters, calling for more time to adjust and saying a high rate of GST could put his firm out of business.

Countries that have introduced GST in the past have often faced a relative economic slowdown before the benefits of a unified tax regime feed through.

India is already the world’s fastest growing large economy, expanding by 7.9 per cent year on year in the March quarter. Economists at HSBC forecast a boost of 0.8 percentage points from the GST within three to five years.

Tax experts say that only 20 per cent of – mostly big – firms are getting ready for the GST. The rest are taking things as they come in a country where coping with a changing tax regime has been a way of life for decades.

Yet even those actively preparing must contend with a series of unknowns as the national and state parliaments tackle the task of transforming a “model” GST law into the real thing.

The first hurdle will be for a majority of state parliaments to pass the GST amendment, which would establish a GST Council to finalize key terms of the new tax.

That could take until November and mean that the legislation to put the GST into force would only come before the national parliament’s winter session.

Hitting the government’s target launch date of next April 1, the start of the fiscal year, looks ambitious. Slippage to July or October, 2017, is increasingly likely, say experts.

Mr. Modi’s government favours a GST rate of 18 per cent but states are lobbying for more. While goods producers have become inured to high tax rates, service companies now paying 15 per cent would take a hit that they would either have to absorb or pass on to customers.

“I don’t think a rate beyond 20 per cent would fly politically – if they do that it would be inflationary,” said Harishankar Subramanian, head of indirect tax at EY India.

Add to that a lack of clarity on where deals are transacted for tax purposes and telecoms, financial services and e-commerce players are worried.

“Services companies are looking at the GST as you would look at a snake,” said Amit Kumar Sarkar, head of indirect tax at Grant Thornton.

The question for Mr. Modi will be whether the boost to economic growth materializes in time for his expected bid for a second term.

“If the tax regime stabilizes, Mr. Modi can stand up in 2019 and say: ‘I’ve passed the biggest tax reform in Indian history,’” said EY’s Mr. Subramanian.

India’s economy

One nation, one tax

A tax overhaul will have welcome, if unpredictable, consequences

Aug 6th 2016 | MUMBAI | From the print edition

Time to lighten the load

GIVEN how few voters enjoy paying them, politicians rarely trumpet the advent of new taxes. But the passage of a new goods-and-services tax (GST) in India’s upper house on August 3rd is a deserved exception. Well over a decade in the making, the new value-added tax promises to subsume India’s miasma of local and national levies into a single payment, thus unifying the country’s 29 states and 1.3 billion people into a common market for the first time. The government of Narendra Modi, never averse to over-hyping what turn out to be modest policy tweaks, has enacted its most important reform to date.

Few countries are fiddlier than India when it comes to paying taxes; the World Bank ranks it 157th out of 189 for simplicity. Both the central government and powerful state legislatures impose a dizzying array of charges. Because the rates differ between states, making stuff in one and selling it in another is often harder within India than it is in trade blocs such as NAFTA or the European Union. Queues of lorries idle at India’s state boundaries much in the same way they do at international borders.

That should change with the GST, essentially an agreement among all states to charge the same (still to be decided) indirect tax rates. Businesses are thrilled at the idea of being able to distribute their products from a single warehouse, say, rather than replicating supply chains in each state. Thick, exception-riddled tax codes—car sales are liable to six different levies at various rates, depending on the length of the vehicle, engine size and ground clearance, for example—are to be replaced with a single GST rate to be applied to all goods and services.

Better yet, the GST will be due on the basis of value added. That avoids businesses being thwacked by taxes on the entire value of the products they buy and sell rather than just the value they create—a situation that often made it cheaper to import stuff rather than make it locally. Just as importantly, by requiring businesses to document the prices at which they buy inputs and sell products (unless they wish to pay higher taxes), it will force vast swathes of the economy into the reach of the taxman.

Economists and technocrats have long backed the GST, which they think could boost economic output by 1-2 percentage points a year. Their calls were insufficient to overcome India’s petty politics: GST proposals stalled under governments of left and right since it was first mooted in 2000. Mr Modi, as chief minister of Gujarat state until 2014, helped thwart the previous government’s GST plans and has faced retaliatory obstructionism since. A committee of various states’ finance ministers helped convince regional parties in the upper house, which Mr Modi’s government does not control, to clear the blockage.

Because the tax overhaul requires a new amendment to the constitution, and therefore the backing of at least 15 state legislatures, it will take several months to enact. Few expect it to be derailed, but a deadline of April 2017 seems unlikely to be met. Though efforts to water down the bill (for example by exempting petrol) appear to have been overcome, its precise workings remain undecided. Even the GST rate is unknown; a government study mooted 17-18% but some states (which will receive the cash raised) would like it to be higher.

Such nitty-gritty will be fought over in the “GST council”, a novel body which will represent both state and federal executive branches but looks likely to be dominated by ministers sitting in New Delhi. Arvind Subramanian, the government’s chief economic adviser, calls the whole construct “a voluntary pooling of sovereignty in the name of co-operative federalism”, borrowing freely from the lexicon once used by the builders of the EU’s common market a generation ago. Such projects do occasionally run into bouts of difficulty.

Indeed, the new council and the tax it will administer go against a recent trend for decentralising power from New Delhi to the various state capitals. Powerful chief ministers sitting in the provinces will be more dependent on revenue collected federally and less on purse-strings they control themselves. Money will shift from (richer) states that make things towards (poorer) ones that consume them, too. The advent of a single tax to rule them all may come to shape Indian politics as much as it does the economy.

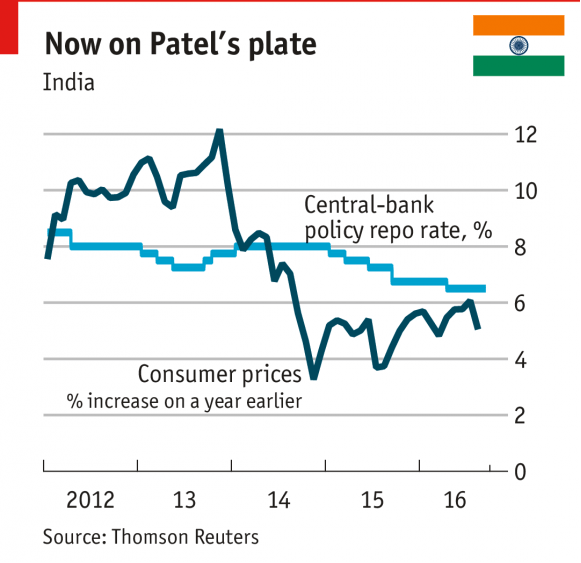

India’s central bank

Reserve player

Will the new governor be a clone of the old one?

Aug 27th 2016 | MUMBAI | From the print edition

Patel-tale signs of orthodoxy

CENTRAL banks need the confidence of investors to function well, so questions about their leadership and independence are seldom welcome. On August 20th Narendra Modi, India’s prime minister, belatedly appointed a new head of the Reserve Bank of India (RBI), nine weeks after Raghuram Rajan, the incumbent, and surprised everyone by announcing he was stepping down. The new man, Urjit Patel, was an understudy to Mr. Rajan—prompting plenty to wonder why the original cast member was, in effect, forced out.

Beyond the usual way stations for central bankers—Yale, Oxford, a period at the IMF—Mr. Patel was once a management consultant and an executive at Reliance Industries, a group headed by Mukesh Ambani, India’s richest man. He has been a deputy governor of the RBI since 2013.

India’s newish inflation-targeting framework, which has been successful in stemming rising prices (helped by outside factors such as falling oil prices), is as much his as Mr. Rajan’s. So is the upcoming arrangement whereby interest rates will be set by a panel comprising government and RBI appointees, rather than the governor alone. Though he lacks the stature of Mr. Rajan, a former IMF chief economist, his hawkish credentials will help fend off calls for lower rates from ministers and industrialists.

His appointment should alleviate fears that Mr. Rajan’s untimely exit—all recent RBI governors have served more than a single three-year term—was a ploy by Mr. Modi to hobble the central bank’s independence. Insiders suspect that it was Mr. Rajan’s sideline as a public intellectual, pontificating on matters far removed from economics that undermined him in Mr. Modi’s eyes. Mr. Patel is unlikely to stray so far from his bailiwick.

If monetary policy is expected to remain unchanged, the regulation of banks, the RBI’s other main remit, is a more open question. The state-owned lenders, some 70% of the industry, are struggling with dud loans they extended to industry and infrastructure firms five years ago. Mr. Rajan had forced the banks to recognize the holes in their balance-sheets, indirectly taking on the tycoons who had benefited from the forbearance of bank bosses.

Mr. Patel’s views on bank regulation are not known. Some of the sensible stuff enacted in recent years, such as making it easier for newcomers to obtain banking licenses, will surely stay in place. But whether Mr. Patel keeps up the same pressure on the banks will be a big test in the early stages of his three-year mandate. Many hope the new governor will be a clone of the man he replaces—while wondering why Mr. Modi didn’t just stick with the original.

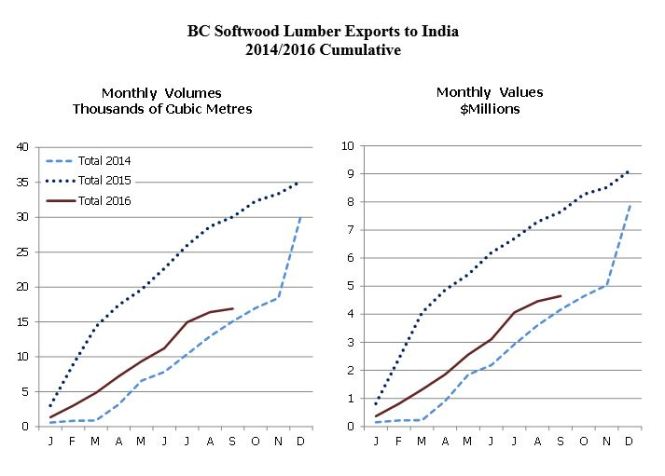

BC Forest Investment and Innovation Data for India Comparing 2014, 2015 and 2016

PM Modi ‘to boost economic ties’ with Vietnam

Sep 03, 2016 |

Prime Minister Narendra Modi (Photo: PTI)

Prime Minister Narendra Modi on Friday said India will engage constructively on all pressing international priorities and challenges with world leaders as he looks forward to “a productive and outcome-oriented” G20 Summit in China’s Hangzhou that begins from Sunday. The Prime Minister, left for Vietnam on Friday evening before he heads for China after that, said his government attaches a high priority to bilateral relations with Vietnam and the partnership between the two countries will benefit Asia and the rest of the world. PM Modi will be in Vietnam till Saturday after which he will be in China on Sunday and Monday before returning to India later that day. Vietnam is a strategic partner of India in Southeast Asia and is said to be keen on acquiring the 290 km-range BrahMos supersonic cruise missile from India.

“Today evening, I will reach Hanoi in Vietnam, marking the start of a very important visit that will further cement the close bond between India and Vietnam,” Modi said. “We wish to forge a strong economic relationship with Vietnam that can mutually benefit our citizens. Strengthening the people-to-people ties will also be one of my endeavors during the Vietnam visit,” he said in a Facebook post.

During the Vietnam visit, Modi will hold extensive discussions with Vietnam’s Prime Minister Nguyen Xuan Phuc. “We will review complete spectrum of our bilateral relationship,” he said. According to news agency reports, he will also meet the President of Vietnam, Tran Dai Quang, and the General Secretary of the Communist Party of Vietnam, Nguyen Phu Trong; and the Chairperson of the National Assembly of Vietnam, Nguyen Thi Kim Ngan.

“In Vietnam, I will have the opportunity to pay homage to Ho Chi Minh, one of 20th century’s tallest leaders. I will lay a wreath at the Monument of National Heroes and Martyrs as well as visit the Quan Su Pagoda,” the Prime Minister said.

He also greeted people Vietnam on their National Day today. “Vietnam is a friendly nation with whom we cherish our relationship,” Modi said.