Canada’s Housing Markets A Dichotomy of Messy Extremes

Canada Housing News

Canada’s largest banks warm to sharing mortgage risks

Tim Kiladze and Tamsin McMahon

The Globe and Mail

Published Thursday, Oct. 06, 2016 6:00AM EDT

Last updated Thursday, Oct. 06, 2016 10:07AM EDT

Canada’s largest banks are quietly embracing Ottawa’s new mantra to share some risk in the country’s mortgage system, a fundamental shift that would alter the way the country’s $1.4-trillion mortgage market operates.

This week, federal Finance Minister Bill Morneau said he would begin discussions with the financial industry on a government plan to introduce risk-sharing into the taxpayer-backed insurance market that covers mortgages when the customer does not have a down payment of at least 20 per cent.

Canada is unique among advanced economies in that a large share of its mortgage market is covered by government-backed insurance, meaning taxpayers could have to cover the banks’ losses for large-scale mortgage defaults during a housing crash. Risk-sharing would reduce the amount of public money that the Canada Mortgage and House Corp. and other institutions could have to pay to the lenders.

Read more: Canada’s banks brace for mortgage overhaul

Related: Ottawa’s housing reforms target foreign buyers, mortgage debt

Related: Alternative lenders face ‘major changes’ in wake of new housing rules

Publicly, the banking community’s message is that risk-sharing is unnecessary because there is no indication that a crisis would overwhelm the mortgage insurance system. They also say a change could severely damage the big banks’ profits by forcing them to devote more capital to their mortgage portfolios. “We have concerns that it could have negative side effects on a housing finance system that has worked smoothly, simply and efficiently and served Canada’s economy well,” the Canadian Bankers Association said in a statement.

But in private, many banks have embraced the idea, according to conversations with people familiar with the evolution. “Philosophically, people aren’t all that fussed,” one executive said.

The banks’ change of heart comes amid growing worries about elevated levels of household debt in Canada and soaring prices for homes in Toronto and Vancouver. “All lenders concern themselves when they see eye-watering [price] increases in urban markets,” said John Webster, head of real-estate-secured lending at Bank of Nova Scotia, because they force buyers to borrow more.

The announcement from the Liberal government is a marked departure from the Conservative government’s position that risk-sharing would be too “dramatic” a change to Canada’s housing finance system.

Federal officials held informal talks with the financial industry on risk-sharing at the start of the year, but announced their intentions only this week. Ottawa now appears intent on enacting a plan to reduce taxpayers’ exposure to the housing market, and make the banks pick up some of the slack.

Internal documents from the Department of Finance obtained by The Globe and Mail under Access to Information show that Ottawa has been considering a variety of approaches.

Government officials are studying three scenarios, according to the heavily redacted draft report of a meeting involving Finance officials in July, 2015. The first is a system where lenders would absorb a fixed percentage of the value of a defaulted loan, known as “first loss.”

Another option is a “split loss,” in which lenders pay a percentage of the total losses associated with a defaulted mortgage.

The third is “fee-based approach” in which insurers cover the full claim on mortgage defaults and charge lenders a fee. The fee option is one way the government has sought to address concerns that lender risk-sharing would affect CMHC’s $426-billion mortgage-backed securities programs, which the government also guarantees.

The document also outlines “key considerations” the government is studying, including how risk-sharing might affect competition and pricing in the mortgage market, and capital requirements for lenders.

“We must recognize that lender risk sharing would represent a fundamental reorientation of Canada’s housing finance framework, a framework that has served us very well for decades, with potential consequences that we need to fully understand,” the document states.

The Department of Finance is set to release the consultation paper in coming weeks that will more directly detail how Ottawa hopes to implement risk-sharing in the mortgage market.

Finance officials declined to discuss the options until then. “It would be inappropriate to speculate on the content before the paper is released and accessible to all stakeholders,” the department said in an e-mail.

Another proposal is putting a time limit on mortgage insurance. Currently, insurance backed by Ottawa lasts for a loan’s entire lifetime – up to 25 years on new mortgages. One option is for government backing to end at a fixed point – maybe 15 years. That could reduce taxpayers’ current exposure by 20 to 40 per cent.

As it stands, a large portion of the Big Six banks’ portfolios of insured mortgages are deemed risk-free by the Office of the Superintendent of Financial Institutions, their federal watchdog. These comprise about 70 per cent of the total market, which means taxpayers are on the hook for a large share in the event of a decline in housing prices due to a recession. The CMHC and its two private sector competitors, Genworth and Canada Guaranty, have insured more than $900-billion worth of mortgage debt as of the second quarter.

In an interview Monday, Mr. Morneau said Ottawa is committed to a gradual and modest approach to moves that could disrupt the country’s housing-finance system.

“Any changes we’ll make will be in consultation with the financial institutions,” he said. “But I think it would be fair to say that we think that we need to look at where the risk is placed in the market and do it in a way that acknowledges how well the market has worked, acknowledges how sound our housing market has been for the long-term and also recognizes that you’ve constantly got to stay on top of it.”

Stuart Levings, CEO of Genworth, CMHC’s the largest private-sector competitor, was not surprised the government is going ahead with formal consultations. But he said risk-sharing is not needed because current stringent regulations have kept mortgage defaults low and prevented the kind of bad loans that hurt the mortgage insurance industry. “There’s nobody just throwing a loan at the wall and seeing if it sticks so to speak,” he said.

People in the financial industry say Ottawa seems sincere about wanting a constructive dialogue rather than pushing a particular proposal, and that banks would not tolerate a heavy-handed shift in the mortgage market.

In the same way that they discourage sudden Bank of Canada interest rate hikes, they fear too strong an approach could harm the housing sector, which is crucial to the Canadian economy, and to the banks’ and the governments’ finances.

There is also still some frustration in the bank corner. The lenders have said they are willing to be proactive, but they still expect a bit of a game to be played before a final proposal is drafted, with each side staking out their territory. What’s become clear, however, is that multiple proposals are floating around, many of which are much more nuanced than the widespread assumption that any risk sharing would come in the form of a deductible on mortgage insurance.

Mr. Levings has suggested to Ottawa that it implement a two-tiered system for risk-sharing, requiring a higher deductible for CMHC mortgage insurance than what lenders would pay if they insured their mortgages with the private sector. “That would automatically shift a little more risk over to the private sector,” he said.

Still, he said, any shift toward risk-sharing might make lenders less likely to lend to home buyers in riskier housing markets such as remote and rural communities and those that are highly dependent on the fortunes of a single industry, such as oil or forestry.

“I don’t think we’ve really put a lot more thought into what we would prefer to see,” he said, “just because we’re still hoping that this would never need to be done.”

Housing market sees third-largest August gain since 1999

Canada’s home prices rose 1.5 per cent in August, marking the third-largest gain for that month since the index series launched in 1999.

Toronto led the way in month-over-month increases, according to new data from the Teranet-National Bank House Price Index. Seven of the 11 metropolitan markets surveyed experienced month-over-month price gains.

— Brent Jang

Go to this hyperlink (IF YOU SUBSCRIBE..) http://www.theglobeandmail.com/real-estate/house-price-data-centre-march-surge-largest-in-8-years/article29697029/

Calgary’s real estate picture continues to diverge from the hot markets in Toronto and Vancouver with a 20th consecutive month of declining home sales in July. (Jonathan Hayward/THE CANADIAN PRESS)

What real estate boom? Calgary home sales drop to 1996 levels

Tamsin McMahon – REAL ESTATE REPORTER

The Globe and Mail

Published Tuesday, Aug. 02, 2016 6:40PM EDT

Last updated Wednesday, Aug. 03, 2016 8:24AM EDT

Calgary’s housing market is bracing for more pain as persistently weak oil prices, mounting layoffs and slowing population growth continue to keep buyers on the sidelines.

Home resales in the city fell 12.6 per cent in July from the same time last year, the Calgary Real Estate Board reported. It was the 20th consecutive month of annualized sales declines as purchases of detached homes dropped to their lowest level since 1996.

“We’ve certainly got a softer market than we did a year ago,” said Diane Scott, a broker with Royal LePage.

Benchmark resale prices dropped 4.2 per cent from last July and were down more than 5 per cent from their peak in October, 2014. Detached home prices fell 3.4 per cent from last year to $502,300.

Among condos, a surge of new listings has left the market with more than six months’ worth of supply, pushing the benchmark price down 6.6 per cent from a year earlier to $277,000. Condo sales were down 21 per cent from a year earlier and were 53 per cent below peak levels in 2014. Properties in the city centre have been hit the hardest, the real estate board said, with overall benchmark price declines of 5.1 per cent, compared to 0.8 per cent for the city’s more affordable northeast quadrant.

Signs of continued slowdown in the housing market come as the City of Calgary released updated census data showing that net migration dropped in the last 12 months ended in April.

It was a sharp reversal of long-term trends that saw workers from Canada and abroad flock to jobs in Alberta.

Net migration – the difference between the number of people who moved to Calgary and the number who left – fell by more than 6,500 in April from the same time last year, the city’s figures show, mirroring the population plunge seen during the region’s last recession in 2010.

Census figures show there are now more than 20,800 vacant homes in the city, an 8,300 increase from the previous year, as the epicentre of Canada’s oil industry grapples with a recession that economists at Toronto-Dominion Bank said recently “is likely to go down in history as one of the most severe.” The bank predicted that average household disposable income in Alberta, a measure of living standards, would fall 5 per cent this year, a fact that is also weighing on Calgary’s housing market.

“The number of unemployed workers keeps rising and when you combine job losses with declining net migration, the result is going to be weaker housing demand,” said the real estate board’s chief economist, Ann-Marie Lurie.

The exodus of workers from Calgary has meant fewer new buyers in the city’s housing market and those who are shopping for homes are taking longer to make an offer, said Royal LePage’s Ms. Scott. “There are fewer buyers to start with and those that would be in the market are sitting on the fence, waiting for the prices to come down some more,” she said.

RELATED: Heritage Beltline house could be saved or sunk by unique zoning

Where buyers might have previously looked at a handful of listings before purchasing a home, many are now looking at 14 to 15 properties, she said. “They look an awful lot more than they buy these days.”

The market for more affordable detached houses and townhouses, those priced below $500,000, as well as the luxury housing market above $1-million have fared relatively well, Ms. Scott said. But the market for mid-priced homes, those between $600,000 and $800,000, has suffered from a lack of move-up buyers, while rising vacancy rates have scared off many investors who would normally have purchased condos.

In one bit of good news, the number of listings on the resale market dropped more than 10 per cent from a year earlier, led by a near 14-per-cent drop in listings of detached houses. That has helped ease pressure on prices, the real estate board said.

SIGNS OF CHANGE: CANADA’S NEW ECONOMIC REALITY

OUT OF ALBERTA

For years, workers from coast to coast flocked to Alberta to cash in on the province’s oil boom. Now, with crude prices languishing, labourers are on their way out. As Canadians embrace a new willingness to move for work, Kelly Cryderman and Brent Jang report on a trend that is reshaping the geography of Canada’s labour force.

Kelly Cryderman AND Brent Jang

CALGARY AND SURREY, B.C. The Globe and Mail Last updated: Friday, Jul. 15, 2016 7:11PM EDT

This is part of an occasional series on Canada’s economy and its shift away from resources.

Lee Cronin saw the end of his time in Alberta coming. In 2015, he made a base wage of $42 an hour on the rigs, but the lucrative overtime pay he collected as a derrickhand started to dry up as the lower oil price became more entrenched.

After spending the better part of seven years flying from his home in British Columbia to his jobs in the oil patch, Mr. Cronin, 42, saw his hours dwindle and the frequency of his flights significantly decrease.

The pickup truck he kept at the airport park-and-ride in Edmonton was suddenly doing little more than racking up parking fees. After one particularly long spell away from Alberta, he recalls paying more than $800. Then, in January, the work came to a halt altogether.

“It’s feast or famine out there. I knew that,” Mr. Cronin said during a break from his new job in B.C. “We were making very good money. Then things slowed right down to a snail’s pace.”

Mr. Cronin has left Alberta for work in Surrey, B.C.

Darryl Dyck for The Globe and Mail

Now Mr. Cronin works at the Teal-Jones lumber mill in the Vancouver suburb of Surrey, along with others who have left Alberta’s oil bust. But he makes less than half of the base wage he earned on the rigs.

He and his co-workers are part of a small but growing contingent who are leaving Alberta for other, more economically robust provinces. The low price of crude and the resulting loss of tens of thousands of oil-patch jobs has now set off a new wave of interprovincial migration that is reshaping the configuration of Canada’s labour force.

“We’re right at the turning point now,” as Canadians uproot in search of work wherever they can find it, said BMO Nesbitt Burns senior economist Robert Kavcic.

“You tend to see changes like this happen about six months to a year after you see big shifts in the labour market,” such as the extensive job cuts in Alberta, he said.

The current migration from Alberta is part of a broader trend of Canadians becoming increasingly mobile in the search for work, according to the Bank of Canada.

“Labour is being more efficiently reallocated to the regions of the country that have the tightest labour markets and away from those with excess labour supply,” said the central bank’s recent report, Canadian Labour Market Dispersion: Mind the (Shrinking) Gap.

The excess labour supply is currently concentrated in Alberta, where long-time residents are contemplating packing up and moving out – sometimes back to hometowns they haven’t lived in for decades. Fly-in/fly-out workers from B.C., Saskatchewan and Atlantic Canada who once earned big Alberta paycheques are setting aside their nomadic lifestyle to find what often more modest-paying jobs are closer to home. Some are just waiting until their children finish school or they sell their home before heading to strong labour markets in British Columbia and Ontario.

While the province once attracted migrants from across the country, and immigrants from around the world, economic heft has – at least for the time being – shifted elsewhere.

“It’s just a complete turnaround from what we’ve been used to over the past decade or so,” Mr. Kavcic said.

Alberta today is a province humbled by low global commodity prices – particularly for oil, which began its price slide in mid-2014. The Conference Board of Canada says the price slump means the province will remain in recession this year, with its economy contracting by 2 per cent in 2016. The wildfires that hit the Fort McMurray region in May could add to the economic woes of the province. Longer term, concerns about the ability to build new pipelines, having access to international crude and natural gas markets beyond the United States, and the restraint that could be placed on the energy industry in an increasingly low-carbon world, also weigh on the province.

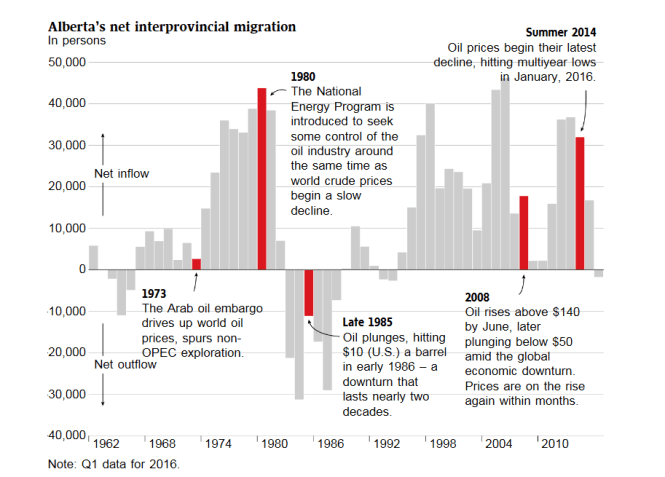

People have voted with their feet. Alberta’s long-standing status as a net gainer of people from other provinces officially ended late last year.

According to Statistics Canada, Alberta had a net loss of 977 people to all the other provinces in late 2015, and another 1,788 in the first three months of this year. This is the first time the province has been a net loser in recent memory, save for several months during the global financial crisis in 2009 – and that was really just a blip in the long-term trend of people moving to Alberta. When it comes to significant numbers, Alberta hasn’t lost people to other parts of the country since the early 1990s, a time when energy prices just started to rise out of the deep hole of the previous decade. Alberta was a net loser of tens of thousands of people between 1983 and 1988.

Booms, busts and migration

Alberta’s migration patterns are inextricably linked to the oil industry’s fortunes. During boom times, thousands of Canadians pile into the province in search of jobs, but the population rush often slows or reverses after crude prices drop. Typically, shifts in migration lag changes in the jobs market.

But now that the province has seen two years of lower energy prices, the question is whether this is the thin edge of a wedge, and the beginning of a larger movement of people to other provinces.

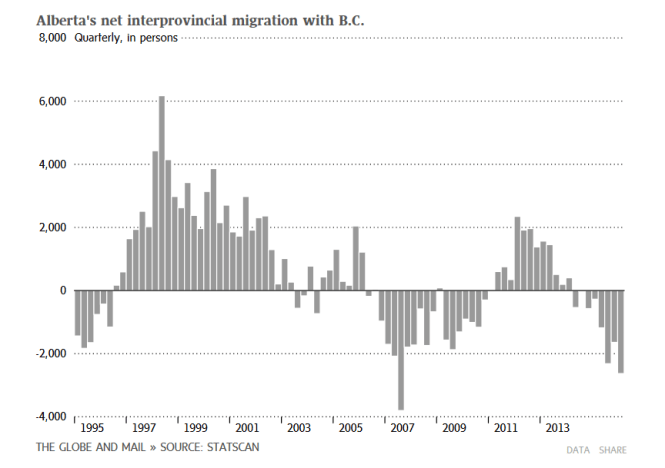

British Columbia, with jobs in forestry, construction, transportation and real estate, is becoming a destination of choice, and employment statistics show why. B.C.’s unemployment rate is 5.9 per cent, the lowest provincially. In June, the number of people employed grew by 70,000, or a 3-per-cent increase, the fastest growth among the provinces.

More B.C. residents moved to Alberta than the other way around from 2011 to 2013, but the trend began reversing in the third quarter of 2014 as the B.C. economy stayed steady. Last year, as Alberta’s economy slumped, British Columbia saw a net gain of about 5,400 people from its next-door neighbour.

In many Alberta communities with strong ties to the resource sector, there are significant numbers of relative newcomers – drawn to the province for work during the boom years. For those without strong ties to the province, the end of their employment could mean there’s nothing to keep them in Alberta. “People will head back to where they came from,” said University of Western Ontario sociologist Michael Haan, who studies migration.

“It’s not just about oil. Because some of the biggest movements in and out of Alberta were not necessarily oil workers – they were people who were working in construction,” Prof. Haan said.

Work of all sorts has dried up. In Statistics Canada’s Wood Buffalo-Cold Lake region, which includes Fort McMurray and oil sands production, the unemployment rate for all of 2015 was 7.9 per cent, compared with 4.7 per cent in 2014. Alberta as a whole has continued to see its unemployment rate creep up, going to 7.9 per cent in June from the 5.8 per cent registered one year earlier.

Layoffs have become a weekly norm. The provincial government, which requires Alberta-based companies to report plans to lay off 50 or more employees at once, says the number of group termination notices was 27 in 2013, 35 in 2014, and hit 116 in 2015. So far in 2016, there have been 50 notices. May was an especially brutal month, with 2,460 Alberta workers laid off in just nine group terminations.

For Alberta’s energy sector, and those industries reliant on it, there might be some light at the end of the tunnel. The Conference Board says the slow recovery in oil prices should ease the number of layoffs and cuts to capital budgets in the oil and gas sectors in the coming months. The wildfire that burned a tenth of Fort McMurray and temporarily shuttered oil sands operations in the region could add to the march out of Alberta as some people choose not to go back to the region. However, the rebuilding effort will likely boost the number of jobs available in the province, and help with the modest economic recovery predicted for 2017, if commodity prices stabilize or rise.

But interprovincial migration numbers reported by Statistics Canada likely understate the magnitude of the shift taking place.

During the boom years, Alberta’s work force included a sizable “shadow population” of people living in camps or in other temporary accommodation while working long hours in energy sector jobs. Like Mr. Cronin, after days or weeks of work, they would fly back home for a break at their primary residences in other provinces.

Mr. Cronin was among many “interprovincial employees” affected by the oil crash.

Darryl Dyck for The Globe and Mail

Frequent flights, including charters, between Atlantic Canada and Fort McMurray – the fly-in/fly-out capital of Canada – made a mobile work force possible. But now those trips have plummeted. For instance, Fort McMurray’s international airport reported a 62-per-cent decrease in charter flights between March 2015 and February 2016.

“People were doing the three weeks on, one week off. Well, they’re just not going out any more,” says New Brunswick Premier Brian Gallant, whose province’s unemployment rate has gone up to about 10 per cent in recent months – a trend he attributes in part to some of his province’s residents losing their Alberta-based jobs.

This year has also seen reports about a seemingly inexplicable jump in Kelowna, B.C.’s unemployment rate, while building permits, housing starts and other economic indicators are up. The Okanagan Lake city’s unemployment rate sat at 7.5 per cent in June but earlier in the year had topped Edmonton and Calgary.

Kelowna’s mayor and others say the uptick in unemployment is due at least in part to the downturn in Alberta, and the potentially thousands of B.C. southern interior residents who lost their commuter jobs in the oil patch.

Statistics Canada says the number of “interprovincial employees” working in Canada (those who live in one province but work in another) at any given time is directly linked to the price of oil. In 2011, the most recent year that numbers are available, Statistics Canada reported that about three per cent of Canada’s paid work force were interprovincial employees, with more than a quarter of those at work in Alberta.

Alberta’s unemployed now includes another restless group: Those who have lost their jobs and want to leave but have to wait. Some don’t want to leave the home they know, some can’t sell their house for a price they like and some wanted to see their children finish the school year.

For most of the seven years that Grande Prairie, Alta. was her home, Crystal-Dawn Dolen, 34, had never had trouble finding work. She worked as a pit boss at a casino and then was a sales rep for a company that provides car breathalyzers. But in January she was laid off. A few months later, still unable to find steady work, she and her 13-year-old son packed up and moved to her brother’s home in Edmonton.

Crystal-Dawn Dolen, 34, is hoping to find stable work outside Alberta.

Kelly Cryderman/The Globe and Mail

There, Ms. Dolen has found a part-time retail job. But the situation isn’t permanent. With her son done the school year in Alberta, she is preparing to move next month to the Langley area in British Columbia – to stay with a friend until they get settled.

She knows housing costs are significantly higher in the Lower Mainland, but she believes with B.C.’s strong economy she will be able to find some kind of customer service-oriented job.

“Working and not getting laid off – and being stable – that’s what I’m looking for.”

Just a couple of decades ago, the country saw big differences between employment rates in different provinces. These differences between regions and jurisdictions were more pronounced here than they were in other countries, such as the United States.

But according to a March report from the Bank of Canada, differences between provincial labour markets have levelled. And the central bank said it’s not about stronger employment growth in previously weak regions of the country; it’s because regional population growth has increasingly taken place in response to labour market conditions.

“Despite the impacts of commodity price booms from 2003 to 2008 and 2010 to 2014, the 2008 Great Recession, and the recent sharp decline in commodity prices on the Canadian economy, Canada’s provincial labour markets are less dissimilar today than at any point in at least the past 35 years,” said the report by Bank of Canada economists David Amirault and Naveen Rai.

In London, Ont., Prof. Haan notes that while most people prefer to remain in the province of their birth, there are a number of factors that make moving away, or travelling regularly for work in another province, more palatable today.

Flights are significantly less expensive, when adjusted for inflation, than they were in past decades. Technology allows people to easily research job postings on the other side of the country, as well as keep in touch with family members and friends living far away. These considerations are especially relevant for younger workers, whose roots might not be as deep as those of older workers, he said.

While that labour mobility once saw Alberta gaining people at the expense of other provinces, economic forces are now pushing people toward Ontario and B.C. – the provinces that will lead Canada’s economic growth this year.

Ian Pohanke, 31, graduated from high school in Surrey in 2003 before he moved to Alberta and worked his way up and ran his own welding business based in Calgary.

“Never been so rich, never been so broke,” he said. “I had this dream of chasing the oil money in Alberta. I have some older cousins and family that live up in northern Alberta, and heard their stories.”

Mr. Pohanke has moved back into his parents’ Surrey home, returning to his old bedroom that had been converted into a guest room. Seven of his B.C. friends also flocked to Alberta after high school. Mr. Pohanke is the last to return. “I made it the longest and everyone else is back,” he said. He’s now a mill worker along with Mr. Cronin.

Asked whether they would return to Alberta, Mr. Cronin and Mr. Pohanke joked that they couldn’t really say, given that their boss was within earshot.

Logan Jones, 26, also a former energy-sector worker, is now the general manager of a small unit at Teal-Jones that is producing shingle-siding panels from western red cedar, hoping to find a niche in the U.S. market by making a higher-quality product.

Mr. Jones, who graduated from high school in B.C.’s Fraser Valley, spent 18 months at rigs in Alberta and B.C. The former roughneck moved back to his home province in April, 2014 – before the energy industry downturn.

Praising the work ethic of Mr. Cronin and Mr. Pohanke, Mr. Jones said their time in Alberta helped shape his two employees.

“You learn how to work hard, and in the cold.”

Alberta hit hard

Alberta is in the midst of one of its “most severe recessions” ever, Toronto-Dominion Bank says, warning of a cumulative contraction of a sharp 6.5 per cent in economic activity by the end of this year.

TD chief economist Derek Burleton and economists Diana Petramala and Warren Kirkland said in a new forecast they expect Alberta’s gross domestic product to shrink by 3 percentage points this year, coming on the heels of what the province has already suffered from the oil shock.

“Based on our revised forecasts, the 2015-16 recession is likely to go down in history as one of the most severe using the GDP benchmark,” the TD economists said.

“Compared to the average of the past four recessions, declines in both real and nominal [GDP] are expected to be double the magnitude.”

The hit to jobs, though, suggests an “average” recession, and the current slump probably would have been uglier still but for some offsetting reasons, including low interest rates, the sinking Canadian dollar and a “moderately growing” U.S. economy.

“That said, to the extent that these factors have been blunting the downside, the recovery anticipated in Alberta starting next year is likely to lack the typical punch that has characterized those in the past,” they said, projecting average economic growth of 3.2 per cent between 2017 and 2018.

As TD put it, Alberta can’t catch a break. Just as oil “provided a decent whiff of recovery,” along comes the uncertain trade threats from Britain’s decision to leave the European Union. That comes on top of the Alberta wildfires that ripped through the Fort McMurry area.

Looking at four previous recessions starting in the early 1980s, TD found this:

Note the hit to personal disposable income. And while unemployment is well below the levels of those past recessions, it is forecast to remain elevated through the end of the year.

It’s also worth noting that while TD forecasts Alberta won’t get back to its 2014 levels until 2018, GDP per capita will still top that of other provinces even during the slump.

“Regarding Alberta’s longer-term prospects, much will depend on how the province tackles many of the challenges on its doorstep – sizable budget deficits, inadequate oil and gas pipeline capacity, competition from the U.S. shale industry for investment, and addressing climate change, to name a few,” the TD economists said.

B.C.’s decision to impose an extra tax on Vancouver-area home purchases by international buyers surprised many. (DARRYL DYCK For The Globe and Mail)

The loonie could be a victim of B.C.’s foreign buyer tax

The Globe and Mail

Published Wednesday, Aug. 03, 2016 5:09PM EDT

Last updated Wednesday, Aug. 03, 2016 7:15PM EDT

British Columbia’s new tax on foreigners’ home purchases may cool more than just the white-hot Vancouver housing market. The chill could extend to the Canadian dollar.

In a research report last week after the B.C. government announced a 15-per-cent transaction tax on purchases of real estate in Greater Vancouver by people who are not citizens or permanent residents, economist and foreign-exchange strategist Charles St-Arnaud of Nomura Securities in London made a case that the inflows of foreign money into Canada’s housing “are likely sufficiently significant to influence the value of the Canadian dollar.” (Mr. St-Arnaud was an economist at both the Bank of Canada and the federal finance department before joining Nomura in 2010.)

The logic is pretty straightforward. When foreigners buy residential real estate in Vancouver (and elsewhere in Canada), they purchase Canadian currency to do so. That demand for Canadian dollars has become substantial, as the booming markets in Metro Vancouver and the Greater Toronto Area have become magnets for foreign investors. And like anything else, rising demand for the currency pushes up its value.

It is hard to say just how much foreign money has been flowing into Canada’s real-estate market – indeed, this has become a crucial question for policy makers trying to tackle the increasingly concerning market excesses in Vancouver and Toronto, and the available data have barely scratched the surface. But Mr. St-Arnaud has extrapolated from some numbers recently collected by the B.C. government to try to come up with a rough estimate.

B.C.’s Ministry of Finance reported last week that between June 10, when it launched its collection of data on foreign purchases, and July 14, foreigners spend $1.02-billion on B.C. residential real estate, including $885-million in Greater Vancouver alone, representing about 10 per cent of the city’s sales. Assuming this was fairly representative of current demand, Vancouver and its surrounding areas attract something approaching $1-billion a month in foreign investment.

We do not have comparable information for the GTA market, but the Toronto Real Estate Board reported $9.66-billion in home resales in June. Sales of new homes totalled roughly another $2.7-billion, based on data from the Building Industry and Land Development Association. Even if you assume foreigners are not as enamoured with Toronto as they are with Vancouver, you could comfortably estimate that Toronto would account for between $500-million and $1-billion a month of foreign housing investment.

Toss in the rest of the country, which certainly attracts some foreign buying despite having generally much less exciting conditions than the Vancouver and Toronto markets, and “maybe total flows into Canadian real estate is $2-billion [a month], and maybe even slightly higher,” Mr. St-Arnaud said via e-mail.

To put it in perspective, net inflows of foreign investment in Canadian securities (stocks, bonds and the like), which certainly have a significant effect on the currency, have averaged about $15-billion a month this year. Inflows from the export of energy products – always a big deal for currency traders, who grossly oversimplify the Canadian dollar as a petro-currency and thus reflexively link its value closely with the price of oil – have been about $5-billion a month. The foreign inflows in the housing market might not be big enough to be driving the currency’s gains this year (up 12 per cent against the U.S. dollar since mid-January), but in a year when Canada’s overall exports have generally struggled (down 3.4 per cent year over year), they are big enough to be providing meaningful support.

So if B.C.’s new tax puts the intended serious dent in foreign demand that could certainly put the Canadian dollar under pressure – at a time when the currency is already facing another downturn in oil prices. So far, the loonie has weathered oil’s recent skid admirably, thanks in part to the country’s relative attractiveness as an investment haven (economic and financial stability, proximity to U.S. growth, interest rates that still look unlikely to decline.) But add in shrinking foreign inflows in the housing sector, and that resilience could give way to a new downturn in the currency.

For some, especially in the export sector, that might be for the best, providing a renewed competitive shot in the arm. Still, it might not happen. As Mr. St-Arnaud points out, the new home-buying tax affects only one attractive Canadian real-estate market (albeit a big one); foreign investors could merely move their attention to Toronto, or Victoria, where hot markets remain unfettered by such a tax.

Still, given the level of concern expressed by all levels of government as well as the Bank of Canada at the housing-market frenzies on the B.C. coast and in Ontario’s Golden Horseshoe, it is hard to imagine that such a shift would last for long without further measures being imposed to cool foreign investors’ enthusiasm. Which might pave the way for the soft landing in housing for which policy makers have long prayed.

Just don’t be surprised if the ultimate fallout includes a somewhat lower-altitude currency, too.

Follow David Parkinson on Twitter: @ParkinsonGlobe

Greater Vancouver home sales tumble in August following foreign homebuyers tax

Defaults Done Has the ulta-hot real estate market frozen solid?

Home sales in Metro Vancouver took a sharp drop in August, as expected, one month after the introduction of the 15-per-cent foreign homebuyers tax.

The Real Estate Board of Greater Vancouver says sales fell 26 per cent compared to the same month last year. Residential property sales totalled 2,489 in August, compared with 3,362 sales in August 2015.

The numbers also represent a 22.8 per cent decline compared with July sales.

As sales slowed, the price of a house, condo or townhouse in Metro Vancouver continued to rise. The benchmark price for detached properties, according to the report, increased 35.8 per cent over August 2015 to $1,577,300, a 4.2 per cent increase over the last three months.

An apartment property increased 26.9 per cent over that same period to $514,300, and the price of townhouse jumped 31.1 per cent to $677,600.

“The record-breaking sales we saw earlier this year were replaced by more historically normal activity throughout July and August,” said board president Dan Morrison in a statement Friday.

“Sales have been trending downward in Metro Vancouver for a few months. The new foreign buyer tax appears to have added to this trend by reducing foreign buyer activity and causing some uncertainty amongst local home buyers and sellers.”

The sales-to-active listings ratio for August 2016 is 29.3 per cent, indicating it remains a seller’s market.

Analysts had predicted a sharp decline following the tax, which came into effect on Aug. 2.

Realtor Steve Saretsky said sales of detached homes dropped 50 per cent in Richmond, Vancouver and Burnaby compared to the average number of sales in August between 2010 and 2014. He left August 2015 out of his calculation because it was an abnormally hot month.

RBC senior economist Robert Hogue said a number of data sources confirmed a sharp drop-off for the first half of August but it will take months to see whether the initial blow will be sustained. He said the market had already begun to cool after an all-time high in February for a number of reasons, including a lack of affordable homes that was hurting demand.

Areas covered by the Real Estate Board of Greater Vancouver report include Whistler, Sunshine Coast, Squamish, West Vancouver, North Vancouver, Vancouver, Burnaby, New Westminster, Richmond, Port Moody, Port Coquitlam, Coquitlam, New Westminster, Pitt Meadows, Maple Ridge, and South Delta.

Meantime, on Vancouver Island, sales hit record-breaking numbers in Greater Victoria. August saw 883 properties sold through the Victoria Real Estate Board’s multiple listing service, leading to a total sales value of $496 million.

That’s up by 19.2 per cent from the 741 properties sold in August 2015 and sets the sixth consecutive monthly sales record, the Victoria Real Estate Board said Friday.

The benchmark price for a typical single-family house in the Victoria core area is now at $746,900. A year ago, it was $603,200. For those who look at average prices, the average for a single-family house throughout Greater Victoria came in at $752,509 and the median (mid-way) price was $645,000.

With files from The Times Colonist and The Canadian Press

Related

September home sales plunge nearly 33% in Metro Vancouver

Tiffany Crawford More from Tiffany Crawford

Published on: October 4, 2016 | Last Updated: October 4, 2016 7:48 AM PDT

The Real Estate Board of Greater Vancouver says home sales in Metro Vancouver plunged by nearly 33 per cent per cent in September over last year, as uncertainty continues in the housing market. Gerry Kahrmann / Vancouver Sun

The Real Estate Board of Greater Vancouver says home sales in Metro Vancouver plunged by nearly 33 per cent in September over last year, as uncertainty continues in the housing market.

In a report Tuesday, the board said the number of sales dipped below the 10-year monthly sales average last month for the first time since May 2014.

There were 2,253 sales last month, a decrease of 32.6 per cent from the 3,345 sales recorded in September 2015 and a decrease of 9.5 per cent compared to August 2016 when 2,489 homes sold.

Last month’s sales were 9.6 per cent below the 10-year sales average for the month, according to the report.

As for the cost of a home in Metro Vancouver, prices remained stable, with a slight decline month to month. The composite benchmark price for all residential properties in Metro Vancouver, according to the board, is $931,900, a 0.1 per cent decline compared to August. Year over year, however there is still an increase of 28.9 per cent increase.

The cost of a detached home remained steady at nearly $1.6 million, which increased by 33.7 per cent over last September, but represents a small decline of 0.1 per cent compared with August.

Board president Dan Morrison says changing market conditions are easing upward pressure on home prices in the region. August was the second month that a 15 per cent tax applied to foreign buyers.

“There’s uncertainty in the market at the moment and home buyers and sellers are having difficulty establishing price as a result,” he said, in a statement Tuesday.

The biggest hit was in the sales of detached properties compared with last year, which decreased 47.6 per cent to just 666 homes sold. Townhomes were down 32.2 per cent and sales of condos declined by 20.3 per cent.

New listings for detached, attached and apartment properties were down one per cent to 4,799 in September, and down 11.8 per cent since August.

The report says the total number of homes currently listed for sale is 9,354, a 13.4 per cent decline compared to September 2015 and a 10 per cent increase compared to August 2016.

The sales-to-active listings ratio for September 2016 is 24.1 per cent, the lowest since February 2015.

Canadian Housing Corporation Statistics

United States News

Summertime blues about Christmas

Michael O’Neill, Agility Forex Senior Analyst, Special to Financial Post | August 11, 2016 7:39 PM ET More from Special to Financial Post

(Mark Wilson/Getty Images) Federal Reserve Board Chairwoman, Janet Yellen

Forget “Summertime Blues.” Global financial markets are already singing Christmas songs despite a heatwave in large swaths of the Northern Hemisphere.

Unfortunately, those songs are of the less cheery variety and include “Blue Christmas”, by Elvis Presley and “The Season’s Upon Us” by Dropkick Murphys.

It’s not actually Christmas that has markets down in the dumps, it’s the lack of clarity surrounding the Federal Open Market Committee (FOMC) interest rate decision due December 14 and the increasing belief that Fed Chair Janet Yellen and the FOMC members have lost their way.

That sentiment isn’t new. Last December, the Fed raised the target funds rate by a quarter point, from 0.0%-0.25% to 0.25%-0.50%, the first rate increase in seven years. In fact, at the time, the decision was viewed as a “doveish” hike and one that was made almost reluctantly. China’s August 2015 equity market meltdown and currency devaluation had triggered a stampede into risk aversion trades and underscored the fragility of the global economic recovery. Deflation was a major concern due to the impact from falling oil prices. Still, the FOMC made a decision.

Today’s issues with the Fed stem from the December 2015 FOMC Economic Projections. Back then, they forecast that the Fed Funds rate would be 1.4% in 2016, 2.6% in 2017 and 3.4% in 2018.

Markets being markets, became convinced that those projections translated into four rate increases in 2016, slotting one increase per quarter, in March, June, September and December.

Then a whole lot of things happened. China equities melted down, again. China devalued the yuan, again. Bank of Japan stimulus initiatives not only failed to devalue the yen, but precipitated a huge rally (From 125.60 to 100.00). The European Central Bank (ECB) ran into the same problem. ECB President Mario Draghi announced a massive stimulus program in March 2016, but the expected EURUSD decline fizzled when he did a Looney Tunes impression and said “That’s all folks.”

In between, Daesh was terrorizing Europe, China had imperialistic sights on the South China Seas and Europe was attempting to deal with a gargantuan refugee and humanitarian crisis, all of which contributed to global economic downgrades by the likes of the World Bank, the International Monetary Fund and the Organization for Economic Cooperation and Development.

And to make matters worse, the United Kingdom held a referendum and voted to leave the European Union.

Despite all the global turmoil, China issues, failed stimulus programs, Brexit risks, and a reduction in global growth forecasts, the erstwhile Committee members of the FOMC fanned the rate hike flames.

Kansas City Fed President Esther George said on July 20, that “the current level of interest rates is too low relative to the performance of the economy.”

Philadelphia Fed President Patrick Harker was even more direct on July 13 when he said “it may be appropriate for up to two more rate hikes in 2016.”

San Francisco Fed President John Williams said that “the very low interest rates that we have today are not normal.”

And FOMC Vice Chairman Stanley Fischer went as far as to imply that if Brexit hadn’t happened rates would have increased in June.

More recently, in early August, Chicago Fed President Charles Evans said he was open to one interest rate increase in 2016 while the Atlanta Fed President wouldn’t even rule out a September rate hike.

Then came the August 5 nonfarm payrolls report. The surprisingly robust 255,000 increase in jobs combined with a bump in average hourly earnings is just the data that the FOMC said they needed to pull the trigger on a rate hike.

Except the financial markets don’t believe it is. The CME FEDWatch tool indicated that the probability for a September rate hike only jumped to 18% from 9% immediately after the data, but it has since declined to 12%. The December probability is only 34.3%.

FX traders apparently agree with the FEDWatch tool. Already, EURUSD and the Canadian dollar have recovered all of Friday’s post NFP losses while USDJPY is only slightly higher.

Ben Bernanke, Fed Chairman from 2006 to 2014, wrote an article for the Brookings Institute suggesting that “with policymakers sounding more agnostic and increasingly disinclined to provide clear guidance, Fed-watchers will see less benefit in parsing statements and speeches and more from paying close attention to the incoming data.”

And therein lies the problem. The data is muddled and sending mixed signals. The employment report may have been strong, but Q2 GDP missed forecasts and was a weak 1.2%. The current Atlanta Fed GDP Now indicator attempts to show current levels of GDP and, as of August 9, U.S. GDP for Q3 is at 3.7%.

Still, the FOMC statement noted concerns about soft business investment and inflation that “continued to run below the Committee’s 2% longer-run objective.”

Janet Yellen has continually stressed, since last December’s meeting, that rate hikes will be data dependent. At the same time, the FOMC still has at least one rate hike forecast for 2016.

As long as the U.S. economic data releases continue to be mixed and inflation remains low, markets should heed Mr. Bernanke’s advice about ignoring Fed speakers and just concentrate on the data.

When Santa comes, he may not have a rate hike in his bag of toys.

Home size increases, but lumber usage down

The average size of new, single-family homes in the U.S. has grown larger in recent decades. Homes being bL1iJ.t now are more than 2.5 times larger than houses built in 1950. However, the volume of timber used in new homes has been in a gradual declines since 1990.

Industry analyst Tack Lutz with the Forest Research Group, a Maine-based firm providi.ng forest economics and timberland investment consulting services, offers several observations.

In a recent report, Lutz noted that house size has been growing faster than wood use per unit. TI1e amount of wood used per square-foot of house has declined from 8.9 board feet per square foot of house in 1950, to 5.6 board feet per square foot in 2010 (a 37% decrease).

As the average new home is getting bigger, rooms are getting bigger – and larger rooms require less lumber per square foot of room. As an example: a 10 x 10 room has 100 square feet of floor space and 40 linear feet of wall, with studs every 16 inches plus top and bottom plates. This adds up to about 235 board feet of 2x4s. A 12x 12 room has 144 square feet f floor ·pace and 48 linear feet of wall, and just over 275 board feet of 2×4. ‘The floor space is 44% higher, but the volume of2x4s is only 18% greater.

As houses have gotten bigger, they have become a tor more open, with fewer walls. Fewer walls and door means less lumber – but in multilevel homes, stronger materials are required to keep the second level floor from sagging.

Engineered products have replaced solid wood in some applications. Some of these engineered products u e le wood. For example, I-joists that replaced solid-sawn 2xl0s and 2x12s as floor joists use less wood.

Lutz reported that vinyl and wood composites have replaced wood in exterior siding on many homes, and vinyl has surpassed wood usage in windows. Wood composites are also being used on decks and railings.

When doves cry? America’s economy

Today’s jobs report is the only one falling between the Federal Reserve’s most recent monetary-policy meeting and its next, in early November. Analysts reckon payrolls swelled by 168,000 in September—just a little below the average monthly gain this year. That is unlikely to be enough to make the Fed raise rates at its November meeting, which falls just days before the presidential election. Rate-setters do say the case for tightening monetary policy has strengthened, though; traders are betting on rates rising in December. Core inflation, which excludes volatile food and energy prices, is 1.7%, a little below the Fed’s 2% target. But hawks are keen to slow the labour market as they approach their goal, lest they overshoot it. Doves think that a dose of above-target inflation would be a good way to raise inflation expectations, which have sagged in recent years. Come December, the hawks will probably get their way.

Random Lengths “Through the Knot Hole” September 19 2016