China economy stable but housing to hit growth

Real estate again weakest link as FTCR Business Activity Index drops below 50

China economy stable but housing to hit growth Real estate again weakest link as FTCR Business Activity Index drops below 50

Financial Time’s latest data covering the Chinese economy pointed to stable growth as 2017 ended. FTCR measures of internal and external trade continued to defy expectations for a meaningful slowdown in the fourth quarter, while household sentiment remained near record levels of optimism.

The FTCR Freight Index ended the year at 52.5, slightly below the previous month’s reading but suggesting a fourth straight month of improving conditions. Our export index also weakened on slower volume growth, but exporting companies reported that profits improved for a ninth straight month. However, our Business Activity Index, a monthly aggregate of our data, was dragged to a four-month low of 49 in December on the back of a slowing housing market.

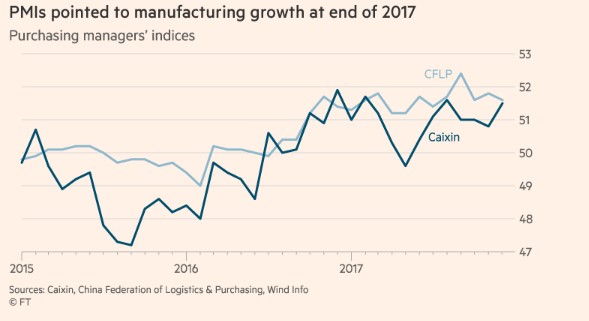

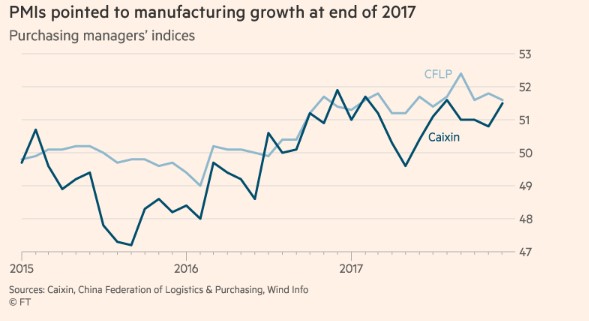

Other public and private sector measures of the economy, released after our data were published, confirmed that growth remained strong last month. The purchasing managers’ index distributed by Caixin rose to a four-month high, while that produced by the China Federation of Logistics and Purchasing, a government-linked association, remained at levels suggesting manufacturing conditions continued to improve in the final month of the year.

The FTCR Real Estate Index fell to its lowest level since January 2017, however, as rising mortgage rates continued to strangle sales activity, particularly in first-tier cities. We anticipate more pain ahead for housing, and its importance to the Chinese economy is such that overall growth will slow.

The government sees financial risk as a key threat to national security, and the country’s property market as a major source of that risk. Deleveraging was not directly name-checked in the statement marking the conclusion of the Central Economic Work Conference in December, prompting speculation that growth considerations will dominate in 2018. However, enough was made of the need to prevent financial system risk to suggest the leadership will continue its regulatory crackdown on finance in 2018. This also means that the purchase restrictions introduced by city governments starting at the end of 2016 will remain in place to snuff out speculation.

Despite tighter policies, consumers are still bullish on house prices. Our monthly gauge of price expectations showed that 62.5 per cent of respondents in December expected prices to keep increasing in the first half of this year, including 18.1 per cent who expect gains of more than 10 per cent. Over a year after local governments began making it more difficult to buy, far more Chinese consumers still expect prices to continue rising than during the peak of the previous tightening cycle in 2014, when just 41.5 per cent expected continued gains.

As price inflation cools, the market’s ongoing slowdown will have a knock-on effect on consumer views towards the economy. Recommended Chinese consumers fret about healthcare and education costs. Rising Chinese interest rates will suppress future Tier One City house price gains. China governments will see more defaults as regulators implement tougher regulations. The government’s response to a slowing economy will be crucial. Previously when growth fell below target, the Chinese leadership would loosen policy. Although the 2018 annual growth target will reportedly be set at 6.5 per cent again, the government has signalled that it will tolerate a slower pace of expansion, in accordance with its new-found goal of improving the lot of Chinese households rather than just chasing growth. The growth target will be announced at the opening of the annual meeting of the National People’s Congress in early March. Allowing growth to slip below target, to about 6.3 per cent, would demonstrate the leadership’s commitment to reform. However, while we expect greater tolerance for slower economic growth, the government will resort to stimulus if the slowdown goes too far. The FTCR China Business Activity Index is a composite reading of business activity and sentiment based on our surveys of companies in the real estate, export and freight sectors. For individual survey methodologies click here. A full set of survey results can be found in the Financial Times Database.

Rising Chinese interest rates check big-city house price gains

FTCR China Real Estate Index takes another lurch down as credit woes hit sales

Rising Chinese interest rates check big-city house price gains FTCR China Real Estate Index takes another lurch down as credit woes hit sales Share on Twitter (opens new window) Share on Facebook (opens new window) Share on LinkedIn (opens new window) Mail Save Save to myFT FT Confidential Research DECEMBER 28, 2017 Print this page House prices stopped rising in major Chinese cities in December as a scarcity of cheap mortgage deals choked sales. The FTCR China Real Estate Index fell to 43.5, its lowest level since January, as sales activity across all city tiers slowed further. Although prices continued to rise in second- and third-tier cities, developers in China’s biggest markets, where the gains have been most intense during this most recent cycle, said that prices had stopped rising in December, the first time they had done so since July 2014. This is not to say that prices are falling outright; 77.8 per cent of developers in these cities said that prices were unchanged relative to the previous month. Nonetheless, the Chinese housing market’s woes look set to continue as the government tries to make good on its pledge to stamp out the speculative impulses that have driven heady price gains across the country during the past two years. Although the number of developers reporting the availability of discounted mortgage rates ticked up in December, more than 90 per cent said first-time buyers were having to pay at or above the benchmark, signalling that credit remains historically tight. Although developers expect sales to fall again at the start of 2018, prices are expected to remain supported by a widespread belief among consumers that prices will continue to rise in the coming months. Share this graphic Sales fell across all city tiers at a faster pace than in November, with our Home Sales Index down another 4.1 points to 39.5, its lowest reading since January. First-time buyers were again the biggest source of demand (47.2 per cent), with those looking to buy an additional home accounting for 20.7 per cent of buyers, and upgraders making up the remaining 32.1 per cent. Developers reported that the volume of sales inquiries fell for a second month, with our inquiries index at 46.4, versus 45.1 in November. Share this graphic Developers in first-tier cities reported that house prices failed to rise in November, the first month they have done so since mid-2014. Increases in second- and third-tier cities were enough to lift the FTCR China Home Price Index 0.3 points to 58.5. The proportion of developers offering discounts rose 2 percentage points to 57.4 per cent, having hit a 44-month low of 53.1 per cent in October. Share this graphic The supply of new houses to the market shrank in all city tiers for a second month, with our New Home Supply Index falling 1.1 points to 44.6. The share of developers reporting rising sales volumes outstripped those reporting supply growth: 16.7 per cent said transactions increased while 15.8 per cent said supply did. Share this graphic Our Home Sales Outlook Index dropped 1.1 points in December to 47.9, but developers across all city tiers expect prices to rise further in the coming month. Our Home Price Outlook Index rose 0.3 points month on month to 56.9. Share this graphic The number of developers reporting that discounted mortgage rates were available for first-time buyers rose for the first month since January. However, credit remains historically tight, with 91.4 per cent saying that buyers are paying rates at or above benchmark. Share this graphic Our Home Sales Index for first-tier cities dropped 2 points to 37.8, in second-tier cities it fell 4.7 points to 39.1, and in third-tier cities it fell 3.9 points to 41.2. Our first-tier-city house price sub-index fell 3.4 points to 50, while the second-tier city sub-index rose 1.2 points to 60.4 and the third-tier city index increased 0.5 points to 59.3.

No ordinary ZhouZhou Xiaochuan, China’s central-bank chief, is about to retire

If you seek his monument, survey China’s economy

Print edition | Finance and economics

Feb 1st 2018

WHEN Zhou Xiaochuan took the helm of China’s central bank 15 years ago, the world was very different. China had just joined the World Trade Organisation and its economy was still smaller than Britain’s. Foreign investors paid little heed to the new governor of the People’s Bank of China. He seemed safe to ignore: another black-haired, bespectacled official whose talk was littered with socialist bromides.

Mr. Zhou is widely expected to retire in the coming weeks. He leaves with China far stronger and his own role much more prominent. No one person can take credit for the flourishing economy. But Mr. Zhou, who is 70, deserves more than most. He helped forge the monetary environment for China’s growth. He also went a long way to dragging the financial system out of the mire of central planning, even if reforms fell short of his own wishes.

His achievements are surprising. China makes no pretence of having an independent central bank. The People’s Bank is under the State Council, or cabinet. But with political acumen and a command of economics, Mr. Zhou carved out power for himself. As the years silvered his hair, his decision to leave it undyed, rare among high-ranking cadres, marked him out as different, even a bit daring.

It did not hurt that, as the son of Zhou Jiannan, a senior Communist official, he enjoyed the privileged status of “princeling”. From his early career in the 1980s, he advocated a more market-based economy. He helped design the “bad banks” that freed Chinese banks of their failed loans and paved the way for a boom. As stock market regulator, he was nicknamed “The Flayer” for trying to root out corruption. Mr. Zhou was not a radical but, by China’s standards, a staunch economic liberal.

When party leaders chose Mr. Zhou as central-bank governor in 2002, they made him the point-man for financial reform. Over time he also became the face of Chinese economic policy in global markets, much liked for his jovial manner and straight talk. At the last big shuffle of government personnel five years ago, he was old enough to retire. A former aide says that Mr. Zhou hoped to return to his other love, music. Sent to work on a farm during the Cultural Revolution, he kept a contraband collection of classical-music records; in the 1990s, when he was a banker, he wrote a book about musicals on the side. But when Xi Jinping became China’s leader in 2012, he asked Mr. Zhou to stay on. The Flayer had come to be seen as a wise elder, an indispensable guide for the financial system through a dangerous period.

His first big move as central banker, back in 2005, was to unpeg the yuan from the dollar. China’s currency remains tightly managed, but it has not stood still. It rose by a third against the dollar in the decade after unpegging. Mr. Zhou also steered China towards a system in which banks set interest rates themselves, rather than merely follow government diktats. Frustrated by the torpor of China’s other regulators, he oversaw the creation of a vibrant exchange for “medium-term notes”, a bond market in all but name. Rather than big-bang reforms, with all their attendant dangers, these were small changes that added up to something bigger.

Yet Mr. Zhou craved more. He wanted to open China’s financial system to the world, believing that only with true competition would it be possible to curb wasteful investment. As a vehicle for this he lighted on internationalising the yuan. Politically, it was an easy sell—leaders liked the idea of having a powerful currency. Economically, it proved complex, requiring China to open its sheltered financial system to more risks. When cash flooded out of the country in 2016, the central bank retreated, ratcheting up capital controls.

Criticism has come from opposite sides. Some economists, mostly in China, feel that Mr Zhou pushed too hard for market forces, especially in his drive to internationalise the yuan. One former adviser, a more conservative economist, calls him “relentless”. The other criticism, more often heard abroad, is that Mr Zhou did too little to cure China’s financial ills. Debt levels soared on his watch, a threat to stability that the government is trying to reduce.

Neither criticism is entirely fair. The project to make the yuan global was never just about the currency. Mr. Zhou knew that opening the capital account would reveal financial shortcomings in China and press the government to crack on with reform. To some extent this is now happening, with officials more focused on risks. As for the debt explosion, Mr. Zhou could do little to restrain it. Given that the government was committed to ambitious growth targets, the central bank had to provide supportive monetary policy. But it has not let things get out of hand: inflation has remained generally low and stable.

Legacy systems

Mr. Zhou is well aware that reputations change. He started his term as central-bank governor when Alan Greenspan was seen as the Federal Reserve’s “maestro”, not yet as a villain of the 2008 global financial crisis. Over the past half-year Mr. Zhou issued several warnings that debts were too high and that, without stricter regulation, China could face serious trouble. To some it looked as if he was trying to protect his legacy, since, if financial turmoil erupts, he cannot be accused of failing to foresee it.

The front-runners to replace him are Guo Shuqing, China’s most senior banking regulator, and Jiang Chaoliang, party chief of Hubei, a central province. Whoever gets the job will have less personal clout than Mr. Zhou. And with decision-making more centralised under President Xi, the central bank itself may play a diminished role. Yet in one respect its next governor will start from a much stronger position. China’s financial reforms are far from finished, but the system as a whole is much more advanced than 15 years ago. As an architect, Mr. Zhou never saw his vision fully realised, but he designed solid foundations.

China Economic Update

By Eric Wong

Managing Director, Canada Wood China

Managing Director, Canada Wood China

May 2, 2018

Posted in: China

2018 Q1 highlights:

- Based on the report issued by the official statistics bureau on April 17th, China’s GDP growth increased 6.8% in the first quarter which exceeded the previous expectation (6.7%); real estate investment is expected to go slower because China intends to restrain excessive speculation in this sector;

- The industrial output growth in March 2018 slowed down to 6% year-on-year compared to the 7.2% from January to February period which showed the strengthen policy to reduce environmental pollution from industry; retail sales are estimated to have rose 9.7% in March which match readings in the first two months, meanwhile industrial production increased 6.4%, made a slower pace compared from January and February; fixed asset investment grew slowly to 7.5% year-on-year from January to March 2018, decreased from 7.9% in January and February this year. Above-mentioned indicators are combined for the first two months of the year because of the annual holiday in China.ii

PMI (Caixin) indexes decreased unexpectedly to 51.0 in March 2018 from 51.6 in February which skipped market consensus of 51.8.iii China Exports dropped 2.7% year-on-year to USD 174.12 billion in March 2018 which didn’t make the market expectations of a 10% growth

China Consumer Price Index (CPI) fluctuated, rose from 101.5 (January 2018) to 102.9 (February 2019) and then decreased slightly to 101.7 (March 2018).v USD/CNY fluctuated, increased from 6.30 (February 1st) to 6.36 (March 1st) and then went slightly lower to 6.29 (April 1st);vi CAD/CNY dropped continuously from 5.13 (February 1st) to 4.95 (March 1st) to 4.88 (January 1st), hit the lowest spot (4.83) on March 16th during the past 12 months.vii

Building material prices

Cement price dropped slightly from RMB 410.83 to RMB 398.33 per metric ton (down 3.04%) over March 2018.viii Rebar steel price went down by 12.22% from RMB 4,088.12 per metric ton on March 1st 2018 to RMB 3,588.46 per metric ton on March 31st 2018.ix The log price index in March 2018 was 1,115.91 points which decreased 0.48% less than February 2019 and grew 2.22% compared to the same period year-on-year; the lumber price index in March 2018 was 1,123.99 which went down slightly of 0.33% month-on-month and decreased 0.56% year-on-year.x

Wood import of Chinaxi

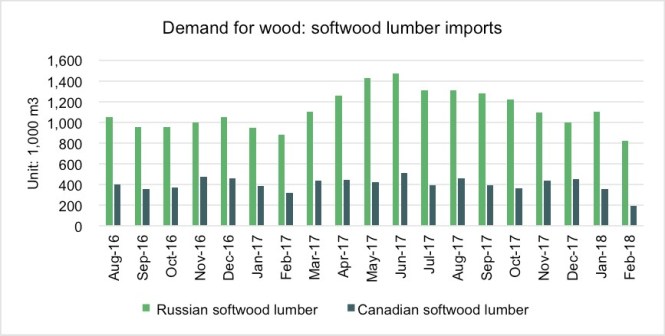

Normally during Chinese New Year (January to February) wood imports to China tend to decrease lower while volume of wood inventory stays higher in most ports. This year the volume of wood imports in total dropped to a new low at 5.49 million m3 in February which decreased 14.81% year-on-year and 35.28% month-on-month. On the contrary log and softwood inventory at Taicang, Wanfang and Meijing Ports increased steady from September 2017 (1.05 million m3) and hit 1.26 million m3 in February 2018, the latter figure shows 2.5% growth year-on-year and fits the total trend. Based on the market trend in previous years it is expected to see wood imports to China to go up and inventory goes down in the coming months. This trend shows consistency when it comes to softwood lumber imports from Russia and Canada, both figures decreased to new lows in February 2018 during the past 12 months especially for Canadian softwood lumber (194,423m3) which dropped 38.93% year-on-year and almost half (44.95%) compared to the volume of last month.

i Huileng Tan (April 17th, 2018). China says its economy grew 6.8% in the first quarter of 2018, topping expectations

ii Bloomberg News (April 16th, 2018). China’s Economy Brushes Aside Trump to Power Ahead in 2018

iii Trading Economics (April 17th, 2018). China Caixin Manufacturing PMI

iv Trading Economics (April 17th, 2018). China Exports

v Trading Economics (April 17th, 2018). China Consumer Price Index (CPI)

vi XE Currency Charts: USD to CNY

vii XE Currency Charts: CAD to CNY

viii Sunsirs (April 2018). Spot Price for Cement

ix Sunsirs (April 2018). Spot Price for Rebar Steel

x BOABC (April 2018). China Wood and Its Products Market Monthly Report

xi BOABC (January to April 2018). China Wood and Its Products Market Monthly Report

Lumber Shipments

By Tai Jeong

Technical Director, Canada Wood Korea

Technical Director, Canada Wood Korea

May 2, 2018

Posted in: Korea

BC softwood lumber export volume to South Korea for the first two months of 2018 decreased 38.6% to 24,430 cubic meters as compared to 39,784 cubic meters for the same period of 2017.

This significant downward trajectory comes from many reasons including weakened BC Coastal shipments in the first quarter of 2018 (36% decrease) and decreased housing starts in the South Korean residential construction segment forced by the South Korean government’s strong intervention to limit the supply of new homes from August 2016 to check rise in household debts and curb rising house prices.

Export value for the same period decreased 23.3% to CAD$8.048 million as compared to CAD$10.489 million for the same period in 2017.

Bank of Japan abandons ‘fiscal 2019’ target for inflation goal

Time frame on Kuroda’s pledge to hit 2% inflation has been postponed six times Haruhiko Kuroda has begun his second term as Bank of Japan governor The Bank of Japan has abandoned a pledge to hit its 2 per cent inflation target “around fiscal 2019” in a belated recognition that prices are less sensitive to monetary policy than it once believed. Japan’s central bank did not change its inflation forecasts, continuing to predict price rises of 1.8 per cent in the year to March 2020, but it scrapped the written time frame it has kept in place since the start of its massive monetary stimulus in 2013. The change of wording signals the BoJ is settling in for a long campaign to raise prices as Haruhiko Kuroda began his second term as governor. Policy stayed on hold, with overnight interest rates kept at minus 0.1 per cent, 10-year bond yields capped at around zero per cent and the BoJ buying assets at an official pace of around ¥80tn ($730bn) a year. “We do not think this will have any near term policy implications, but think the removal of the fiscal year 2019 timeline gives the BoJ more policy flexibility, avoiding the need for more aggressive stimulus,” said Mitul Kotecha, a strategist at TD Securities in Singapore. At the start of his stimulus in 2013, Mr Kuroda promised to hit 2 per cent inflation in about two years, but he has been forced to postpone the time frame six times since then. Those repeated changes have undermined Mr Kuroda’s credibility. Recommended The Big Read Central bankers face a crisis of confidence as models fail The lack of change in policy signals that the reconstituted BoJ board, including two new deputy governors, will carry on with the stimulus in place since 2013. The policy board voted 8-1 in favour of the decision. Board member Goushi Kataoka dissented in favour of more stimulus. New deputy governor Masazumi Wakatabe, who is regarded as a dove, followed tradition and voted with the governor. Inflation in Japan remains subdued with prices, excluding fresh food and energy, up 0.5 per cent on a year ago in March. There is little momentum towards the BoJ’s objective of 2 per cent inflation. Speaking at a press conference, Mr Kuroda said there was no change in policy, but the BoJ had dropped the language to correct market misconceptions about a direct link between changes in the date and changes in the BoJ’s monetary stance. “I think there is a high chance we will achieve something like 2 per cent inflation around fiscal 2019,” he said. The BoJ left its economic forecasts largely unchanged. It expects inflation of 1.3 per cent in the year to March 2019 and 1.8 per cent in the year after that, excluding the effects of a planned rise in consumption tax. Most external analysts are more pessimistic. “Japan’s economy is likely to continue growing at a pace above its potential in [the year to March 2019],” said the BoJ. But it added: “The year-on-year rate of change in the consumer price index has continued to show relatively weak developments.” The BoJ said that risks to growth next year were “skewed to the downside” because of the consumption tax rise, from 8 per cent to 10 per cent, scheduled for October 2019. Its cautious outlook highlights how far Japan still has to go to achieve a permanent escape from the past two decades of on-and-off deflation. Despite slow progress on inflation, economic activity remains robust, with the ratio of open jobs to applicants hitting a fresh 44-year high of 1.54 times. The unemployment rate held steady at 2.5 per cent. The BoJ hopes that tight labour markets will ultimately lead to upward pressure on wages, higher consumption and a faster pace of increase in prices.

The elephant in the room India’s missing middle class

Multinational businesses relying on Indian consumers face disappointment

El

Print edition | Briefing

Jan 11th 2018| MUMBAI

THE arrival of T.N. Srinath into the middle class will take place in style, atop a new Honda Activa 4G scooter. Fed up with Mumbai’s crowded commuter trains, the 28-year-old insurance clerk will become the first person in his family to own a motor vehicle. Easy credit means the 64,000 rupees ($1,000) he is paying a dealership in central Mumbai will be spread over two years. But the cost will still gobble up over a tenth of his salary. It will be much dearer than a train pass, he says, with pride.

Choosing to afford such incremental comforts is the purview of the world’s middle class, from Mumbai to Minneapolis and Mexico City to Moscow. Rising incomes and the desire for status have, in recent decades, seen such choices become far more widespread in a host of emerging markets—most obviously and most spectacularly in China. The shopping list of the newly better off includes designer clothes, electronic devices, cars, foreign holidays and other attainable luxuries.

Many companies around the world are looking to India for a repeat performance of China’s middle-class expansion. India is, after all, another country with 1.3bn people, a fast-growing economy and favourable demography. And China’s growth is flagging, at least by the standards of the past two decades. Companies which made a packet there, both incomers such as Apple and locals like Alibaba, are seeking pastures new. Firms that missed the boat on China or, like Amazon and Facebook, were simply not allowed in, want to be sure that they do not miss out this time.

Enthusiasm about India is boundless. “I see a lot of similarities to where China was several years ago. And so I’m very, very bullish and very, very optimistic about India,” Tim Cook, Apple’s boss, recently told investors. A walk around the Ambience Mall in Delhi shows he is not the only multinational boss with big ambitions in the country. Indian brands like Fabindia, a purveyor of fancy clothes and crafts, are outnumbered by Western ones such as Levi’s, Starbucks, Zara and BMW. The slums that host a quarter of all India’s city dwellers feel a long way off.

Beyond the mall, Amazon has committed $5bn to establish a presence in the world’s biggest democracy. Alibaba has backed Paytm, a local e-commerce venture, to the tune of $500m. SoftBank, a Japanese investor, has funded a slew of start-ups premised on the potential buying power of India’s middle class. Uber, the world’s biggest ride-hailing firm, has hit the streets. Google, Facebook and Netflix are vying for online eyeballs. IKEA is putting the finishing touches to the first of 25 shops it plans to open over the next seven years. Paul Polman, boss of Unilever, has described India as potentially the consumer giant’s biggest market. Reports put out by management consultants routinely point to 300m-400m Indians in the ranks of the global middle class. HSBC, a bank, recently described nearly 300m Indians as “middle class”, a figure it thinks will rise to 550m by 2025.

But for some of the firms trying to tap this “bird of gold” opportunity, as McKinsey once called it, an awkward truth is making itself felt: a lot of this middle class has little money to spend. There are many rich people in India—but they number in the mere millions. There are a great many more who have risen above the poverty line—but not so far above it that they spend much on anything other than feeding their families. And there is less in between the two than meets the eye.

Missing the mark

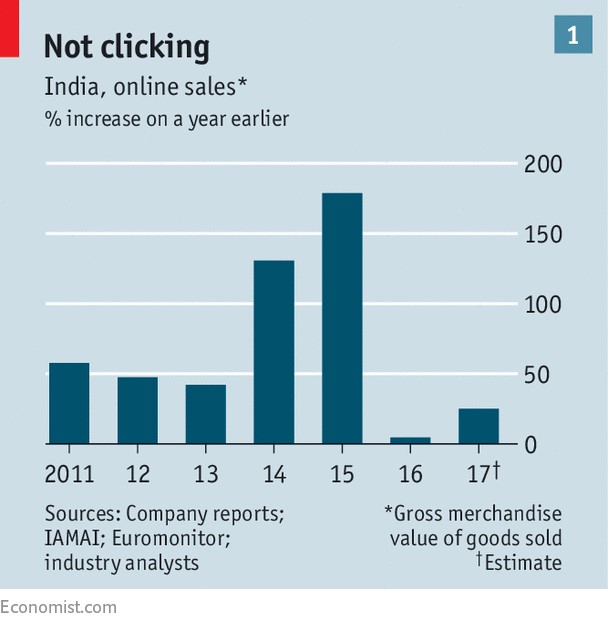

Companies that have tried to tap the Indian opportunity have found that returns fell short of the hype. Take e-commerce. The expectation that several hundred million Indians would shop online was what convinced Amazon and local rivals to invest heavily. Industry revenue-growth rates of well over 100% in 2014 and 2015 prompted analysts to forecast $100bn in sales by 2020, around five times today’s total.

That now looks implausible. In 2016, e-commerce sales hardly grew at all. At least 2017 looks a little better, with growth of 25-30%, according to analysts (see chart 1). But that barely exceeds the 20% the industry averages globally. Even after years of enticing customers with heavily discounted wares, perhaps 50m online shoppers are active in India—roughly, the richest 5-10% of the population, says Arya Sen of Jefferies, an investment bank. In dollar terms, growth in Indian e-commerce in 2017 was comparable to a week or so of today’s growth in China. Tellingly, few websites venture beyond English, a language in which perhaps only one in ten are conversant and which is preferred by the economic elite.

India has yet to move the needle for the world’s big tech groups. Apple made 0.7% of its global revenues there in the year to March 2017. Facebook, though it has 241m users in India, probably the most in the world in one country, registered revenues of just $51m in the same period. Google is growing more slowly in India than in the rest of the world. Mobile phones have become popular as their price has tumbled—but most handsets sold are basic devices rather than the smartphones that are ubiquitous elsewhere in the world.

Eating their words

Fast-food chains once spoke of a giant market. Their eyes were bigger than Indian stomachs. Despite two decades of investment McDonald’s has hardly any more joints in India than in Poland or Taiwan. The likes of Domino’s Pizza and KFC have struggled to come close to expectations that were once sky-high. Starbucks says it has big plans for India but has opened about one new coffee shop a month over the past two years, bringing its total to around 100—on a par with Utah or the United Arab Emirates. A new Starbucks opens in China every 15 hours, adding to 3,000 already operating.

Executives remain relentlessly upbeat in public—even if investments do not always follow. Anurag Mehrotra, boss of Ford India, told the Financial Times in May that car sales in India were set to double every three to five years. That would be an extraordinary change in fortunes: sales grew by less than 20% overall in the six years to 2016. There is one car or lorry for every 45 Indians, according to OICA, a trade group. The Chinese own five times as many. Motorbike sales have grown fast but only because their price has tumbled by 40% since 2000, points out Neelkanth Mishra of Credit Suisse, another bank.

India-boosters point to middle-class services that have taken off. With 20% annual growth in passengers, aviation is already booming at the rate Mr Mehrotra hopes to see in the car industry. But taken together, all India’s domestic airlines are no larger than Ryanair, the world’s fifth-biggest carrier, according to FlightGlobal, a consultancy. SpiceJet, an airline, says that 97% of Indians have never flown. A mere 20m Indians travelled abroad in 2015, about one in 40 adults.

Optimists also argue that the rapid growth of things like Chinese mobile-phone brands shows that the Indian middle class is out there and spending—just not on Western brands. Locally based fast-food chains that undercut McDonald’s or KFC have done much better than the new arrivals. But local consumer businesses face much the same problem as multinationals. Inditex, Zara’s parent firm, has 46 clothes shops in India, fewer than in Ireland, Lithuania or Kazakhstan. For the kind of goods the global middle class aspires to own at least, executives whether at global or local firms clock the number of potential customers at 50m and no more. Even selling basic consumer goods does not necessarily work. Hindustan Unilever, which purveys sachets of shampoo for just a few rupees, has seen virtually no sales growth in dollar terms since 2012.

“The question isn’t whether Zara or H&M can open 50 stores in India. Of course they can. The question is whether they can open 500,” says a banker who asks not be named, on the ground that it is best not to be seen questioning the Indian middle-class narrative. “You can try to push beyond the 50m people who have money, but how profitable would that be? Companies can expand for a time, but the limits to growth are getting obvious.”

The bullish argument that brought Western brands to India was basically this: although the country remains, for the most part, very poor, its population is so enormous that even a relatively small middle class is large in absolute terms, and fast overall growth will, as in China, quickly increase its size yet further. This assumes two things. One is that the middle class in India is the same relative size as in other developing countries where marketers have succeeded in the past. The other is that growth will benefit this middle class as much as other parts of the population. Neither is true in India, which as well as being poor is deeply unequal, and becoming more so.

For all the talk of wanting to tap the middle class, no firm moving into India thinks it is targeting the middle of the income distribution. India’s mean GDP per head is just $1,700, and 80% of the population makes less than that. Adjust for purchasing-power parity by factoring in the cheaper cost of goods and services in India and you can bump the mean up to $6,600. But that is less than half the figure for China (see chart 2) and a quarter of that for Russia. What is more, foreign companies have to take their money out of India at market exchange rates, not adjusted ones.

Defining the middle class anywhere is tricky. India’s National Council of Applied Economic Research has used a cut-off of 250,000 rupees of annual income, or about $10 a day at market rates. Thomas Piketty and Lucas Chancel of the Paris School of Economics found in a recent study that one in ten Indian adults had an annual income of more than $3,150 in 2014. That leaves only 78m Indians making close to $10 a day.

Meager market

Even adjusting for the lower cost of living, that is hardly a figure to set marketers’ heartbeats racing. The latest iPhone, which costs $1,400 in India, represents five month’s pay for an Indian who just makes it into the top 10% of earners. And such consumers are not making up through growing numbers what they lack in individual spending power. The proportion making around $10 a day hardly shifted between 2010 and 2016.

Another gauge is whether people can afford the more basic material goods they crave. For Indians, that typically means a car or scooter, a television, a computer, air conditioning and a fridge. A government survey in 2012 found that under 3% of all Indian households owned all five items. The median household had no more than one. How many of them will be anywhere near able to buy an iPhone or a pair of Levi’s if they cannot afford a TV set?

To get in the top 1% of earners, an Indian needs to make just over $20,000. Adjusted for purchasing-power parity, that is a comfortable income, equating to over $75,000 in America. But in terms of being able to afford goods sold at much the same price across the world, whether a Netflix subscription or Nike trainers, more than 99% of the Indian population are in the same league as Americans that count as below the poverty line (around $25,000 for a family of four), points out Rama Bijapurkar, a marketing consultant.

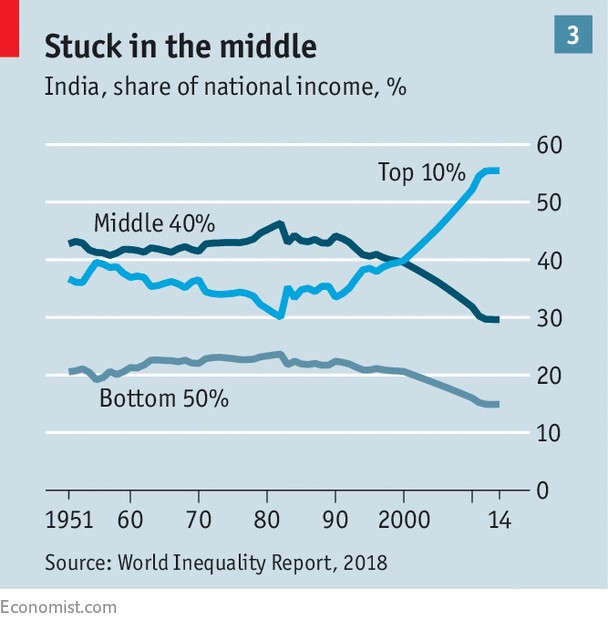

The top 1% of Indians, indeed, are squeezing out the rest. They earn 22% of the entire income pool, according to Mr Piketty, compared with 14% for China’s top 1%. That is largely because they have captured nearly a third of all national growth since 1980. In that period India is the country with the biggest gap between the growth of income for the top 1% and the growth of income for the population as a whole. At the turn of the century, the richest 10% of Indians made 40% of national income, about the same as the 40% below them. But far from becoming a middle class, the latter’s share of income then slumped to under 30%, while those at the top went on to control over half of all income (see chart 3).

Such economic success at the top leaves less for everyone else. Consider the 300m or so adults who earn more than the median but less than the top 10%. This group has fared remarkably badly in recent decades. Since 1980, it has captured just 23% of incremental GDP, roughly half what would be expected in more egalitarian societies—and less than that captured by the top 1%. China’s equivalent class nabbed 43% in the same period.

The rich get richer

Some have doubts about Mr Piketty’s methodology. But other surveys suggest similar distribution patterns. Looking at wealth as opposed to income, Credit Suisse established in 2015 that only 25.5m Indians had a net worth over $13,700, equating roughly to $50,000 in America. And two-thirds of that cohort’s wealth was held by just 1.5m upper-class savers with at least $137,000 in net assets.

India’s middle class may be far from wealthy, but the rich are truly rich. There are over 200,000 millionaires in India. Forbes counts 101 billionaires and adds one more to the list roughly every two months. It shows. The Hermès shop next door to the Honda dealership frequented by Mr. Srinath sells scarves and handbags that cost far more than his scooter. Flats in posh developments start at $1m. In other emerging economies, there are fewer very rich and a wider base of potential spenders for marketers to tap.

In absolute terms, India has wealth roughly comparable to Switzerland (population 8m) or South Korea (51m). Although India’s population is almost the size of China’s, it is central Europe, with a population about the size of India’s top 10% and boasting roughly the same spending power, that is a better comparison. Global companies pay attention to markets the size of Switzerland or central Europe. But they do not look to them to redefine their fortunes.

Confronted by this analysis, India bulls concede the middle class is comparatively small, but insist that bumper growth is coming. The assumptions behind that, though, are not convincing. For a start, the growth of the overall economy is good—the annual rate is currently 6.3%—but not great. From 2002 China grew at above 8% for 27 quarters in a row. Only three of the past 26 quarters have seen India growing at that sort of pace.

Another assumption is that past patterns will no longer hold and that the spoils of growth will be distributed to a class earning decent wages and not to the very rich or the very poor. Yet the sorts of job that have conventionally provided middle-class incomes are drying up. Goldman Sachs, another bank, estimates that at most 27m households make over $11,000 a year—just 2% of the population. Of those, 10m are government employees and managers at state-owned firms, where jobs have been disappearing at the rate of about 100,000 a year since 2000, in part as those state-owned enterprises lose ground to private rivals.

The remaining 17m are white-collar professionals, a lot of whom work in the information-technology sector, which is retrenching amid technological upheaval and threats of protectionism. In general, salaries at large companies have been stagnant for years and recruitment is dropping, according to CLSA, a brokerage.

Might those below the current white-collar professional layer graduate to membership of the middle class? This happened in China, where hordes migrated from the countryside to relatively high-paying jobs in factories in coastal areas. But such opportunities are thin on the ground in India. It has a lower urbanisation rate than its neighbours, and a bigger urban-rural wage gap, with little sign of change. It is not providing jobs to its young people: around a third of under-25s are not in employment, education or training.

There are other structural issues. Over 90% of workers are employed in the informal sector; most firms are not large or productive enough to pay anything approaching middle-class wages. “Most people in the middle class across the world have a payslip. They have a regular wage that comes with a job,” points out Nancy Birdsall of the Centre for Global Development, a think-tank. And women’s participation in the workforce is low, at 27%; worse, it has fallen by around ten percentage points since 2005, as households seem to have used increases in income to keep women at home. Households that might be able to afford luxuries if both partners worked cannot when only the man does.

Spent force

Across the income spectrum, households that do make more money tend to spend it not on consumer goods but on better education and health care, public provision of which is abysmal. The education system is possibly India’s most intractable problem, preventing it becoming a consumer powerhouse. Attaining middle-class spending power requires a middle-class income, which in turn requires productive ability. Yet most children get fewer than six years of schooling and one in nine is illiterate. Poor diets mean that 38% of children under the age of five are so underfed as to damage their physical and mental capacity irreversibly, according the Global Nutrition Report. “What hope is there for them to earn a decent income?” one senior business figure asks.

None of this leaves India as an irrelevancy for the world’s biggest companies. Whether India’s consumer class numbers 24m or 80m, that is more than enough to allow some businesses to thrive—plenty of fortunes have been made catering to far smaller places. But businesses assuming the consumer pivot in India is the next unstoppable force in global economics need to ask themselves why it already looks to have run out of puff—and whether it is likely to get a second wind any time soon.

This article appeared in the Briefing section of the print edition under the headline “The elephant in the room”

BanyanAsia is taking the lead in promoting free trade

Asian voters know open markets have lifted billions of them out of poverty

Jan 24th 2018

THE obituary of the Trans-Pacific Partnership (TPP) was widely written when Donald Trump pulled America out of the 12-country free-trade deal on the third day of his presidency. Yet, a year later and against all the apparent odds, the pact lives on. On January 23rd its remaining 11 members met in Tokyo to thrash out the final details of pressing ahead regardless. The plan is to sign a final agreement in March, to come into force in 2019. It will be one of the world’s most exacting trade pacts, measured by openness to investment from other members, the protection of patents and environmental safeguards.

The pact’s resurrection is one of the more unlikely events in a year of surprises. After all, America accounted for almost two-thirds of the original bloc’s $28trn in annual output. Access to the vast American market was what made other members readier to open up their own. Moreover, Mr. Trump’s retreat had sent a dismal message about the prospects of the open, rules-based order that America had underwritten. The Asia-Pacific region had benefited more than any from that order in recent decades—yet Mr. Trump was declaring multilateralism dead and signalling an intention to raise barriers to trade. Soon afterwards, he ordered South Korea to renegotiate its free-trade agreement with America. And this week he imposed punitive tariffs on imported washing machines and solar panels, aimed at South Korean and Chinese manufacturers (see article).

In spite of this forbidding backdrop, the dauntless 11—Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore and Vietnam—have regrouped. In Vietnam in November their leaders sketched out an agreement on the core features of a revised deal. The pact’s name has changed, to the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), in case the original had tripped too lightly off the tongue. But remarkably few (22, to be precise) of the original provisions have been frozen. The victims are mainly strictures insisted on by America. For instance, copyright has been reduced from 70 to 50 years. And special protections for biologics, a booming category of drugs, have been suspended.

A few concessions were made to those still in the pact. Malaysia will not immediately have to liberalise its state-owned enterprises. Communist Vietnam can put on hold new rules about resolving labour disputes and allowing independent trade unions.

The biggest foot-dragger was Canada, the second-biggest economy in the group (after Japan), which had wanted special treatment for cultural industries such as television and music—a concern for Francophone Canadians—and changes to the rules on imports of cars. Canada has a big car-parts industry, which caters mainly to American carmakers. Now that America has dropped out of the pact, fewer cars from this integrated North American supply chain will have enough content from CPTPP countries to qualify for tariff-free access to other members. But Canada will still have to open its market to Asian cars, subjecting its car-parts firms to a one-sided dose of foreign competition.

In the end Canada’s concerns were met with a favourite TPP trick: “side letters” between it and other members, that are not officially part of the deal. One of them promised Canada greater access to the Japanese car market. CPTPP’s members were sufficiently determined to revive the pact, in other words, that they gritted their teeth and compromised.

How does CPTPP carry on, even as multilateralism has fallen out of favour elsewhere? For some members, including Japan, which has done most to keep the show on the road, there is a strategic imperative: to prop up the old rules-based order in America’s absence. (The less-welcome alternative might be an order overseen by China.) Bilahari Kausikan, a Singaporean ambassador-at-large, predicts that America will eventually return to the partnership. After all, CPTPP (and TPP before it) is not typical of the tariff-cutting deals that Mr. Trump claims have shafted America. Rather, it breaks ground in setting American-inspired standards and safeguards for everything from online commerce to creative industries. Mr. Kausikan believes it is only a matter of time before American firms are clamouring to take part.

Before then, others may seek to join an arrangement designed to be infinitely expandable. South Korea, Indonesia and the Philippines have expressed interest—even Britain has. And CPTPP is not the only trade deal making progress in Asia. Japan has just concluded a sweeping agreement with the European Union. The Association of South-East Asian Nations is seeking to create a vast free-trade area encompassing China and India, among others.

Fair blow the Asian trade winds

In Asia free trade is more popular than it is in America and much of Europe. The question is why. One explanation is that in the West, trade creates winners and losers; in Asia, at a lower stage of development, it mainly creates winners, though some gain more than others.

Yet that is not quite right. Asia’s pell-mell development creates lots of losers. It can be traumatic to be forced off your land to make way for a palm-oil plantation or a high rise. Inefficient rice-farmers across the continent have much to fear from free trade. Even in prosperous Singapore, points out Deborah Elms of the Asian Trade Centre, an advocacy group, it is still an emotional wrench to see nearly every landmark of your childhood vanish in an orgy of rebuilding.

The difference is that most Asians don’t have what Mr Kausikan calls the illusion of choice. Trade is how billions of them have attained a modicum of prosperity. And thanks to rapid, trade-fuelled growth, the drawbacks of opening markets seem relatively insignificant. For as long as wrenching change is offset by the prospect of a better tomorrow, Asia will fly the flag of global trade even when it is being furled elsewhere.

Stratfor Worldview March 11 2018

Overview

The White House Takes on the World: The White House will bump up against the laws of the United States and the central tenets of the World Trade Organization as it launches a global trade offensive in the name of national security. U.S. production costs will rise in response, and countries will target America’s politically sensitive sectors in retaliation.

Trade, Technology and Taiwan: Tension between the United States and China will spike, putting businesses caught in the fray at risk. While the White House targets Chinese trade and investment with its protectionist policies, Congress will rouse Beijing’s ire by upgrading U.S. ties with Taiwan.

A Race to the Cutting Edge: As the United States turns its attention toward its competition with China and Russia, the development of disruptive weapons technology among the great powers will further degrade the world’s arms control treaties. Beijing will funnel state funds toward artificial intelligence research in hopes of catching up with its American adversary while the West struggles to navigate antitrust and data privacy concerns.

The Stubborn Problem of Nuclear Proliferation: Building on a brief detente, South Korea will try to persuade the United States and North Korea to reconcile their mostly intractable positions on the issue of denuclearization. Meanwhile, Iran will rely on Europe’s support to keep its nuclear deal alive as Saudi Arabia uses the same agreement to negotiate a civilian nuclear program of its own.

Fighting for the Future of Europe: Headed by a divided Germany and an emboldened France, the debate over euro zone reforms will expose the deeper divides threatening Continental unity as Italy stands ready to flout any rules-based regime that Berlin and its northern allies propose.

Balancing Oil and Building Batteries: Global oil producers, led by Saudi Arabia and Russia, will extend and adjust their agreed-upon production cuts to counter U.S. shale output over the long run. In the alternative energies sector, battery developers will have to contend with the Democratic Republic of the Congo’s attempt to rake in more revenue as the world’s demand for cobalt grows.

Trouble Brews in the Americas: Mexico will let Canada take the lead in confronting the United States on trade issues during NAFTA negotiations. Trade tension will likewise mar Washington’s rocky relationship with Brazil as the two remain at odds over how to manage Venezuela’s economic crisis and its regional spillover.

India Protects Its Periphery: China’s deep pockets and wide maritime reach will draw India into closer defense cooperation with the United States, Japan and Australia as it works to balance against its increasingly powerful neighbor.

Ankara’s Ambitions Take Center Stage: A rising power in its own right, Turkey will push its troops deeper into northern Syria and Iraq while laying claim to the eastern Mediterranean Sea, upsetting Cyprus’ plans for the energy resources that lie beneath the disputed waters.

Global Trends

The Bull in the China Shop

As U.S. President Donald Trump’s 2018 trade agenda put it, “these are exciting times for U.S. trade policy.” That may be the understatement of the year. The White House is ready to take aim at the global economy this quarter, and the bull’s-eye is sitting squarely on Beijing.

Trump is convinced that China’s economic rise poses a national security threat. And when it comes to China’s penchant for dumping goods, enacting unfair subsidy regimes, distorting the market and violating intellectual property rights, many countries in the developed world would agree. The United States, however, isn’t willing to wait around for the European Union and Japan to address these challenges in a managed, multilateral forum. Instead it will follow an “act now, talk later” strategy that it believes — rightly or wrongly — will coerce Beijing into coming to the negotiating table on Washington’s terms. The United States also hopes its tactics will galvanize free-trade advocates to reform institutions like the World Trade Organization (WTO) so that they, too, can bring China in line with international trade and investment norms. That’s the idea, anyway.

But just as the United States claims that China benefits from a rules-based global trade order [1] by refusing to play by those rules, the White House is bending many of them to make its point. For instance, the sweeping tariffs on steel and aluminum [2] that Washington will use to combat overcapacity in the name of national security will produce a litany of legal challenges within the United States and at the WTO, as affected countries — including members of the European Union, China, Brazil, Japan and South Korea — protest the measures.

In fact, many will retaliate with anti-dumping and countervailing duties of their own against the United States, taking care to target politically sensitive sectors like agriculture ahead of midterm elections in November. These reprisals may even take on an anti-American tone: The European Union has already threatened to crack down on iconic American imports, including Harley Davidson motorcycles, bourbon and blue jeans.

By using creative arguments to wield the most powerful trade weapons in its arsenal, the United States will back the WTO into a corner. Legal challenges in the organization take years to play out, but if the arbitration ends in Washington’s favor, it will endorse a dangerous precedent of invoking national security to justify economic protectionism. Should the WTO rule against the United States, the White House could opt to ignore the decision altogether by citing American sovereignty, undermining the institution’s credibility in the process. (Notably, the White House will also continue to paralyze the WTO’s arbitration system by blocking new appointments to the appellate body.)

In the meantime, steel and aluminum consumers in the United States will have to bear higher input costs. Contrary to Trump’s logic that higher tariffs will reduce trade deficits, they aren’t guaranteed to make Chinese steel less competitive in the United States. Metals exporters subject to U.S. tariffs will divert their goods to other markets around the world, which in turn will cause big metals importers to throw up barriers to protect their markets from a flood of foreign products. Amid the ensuing trade scramble, the United States hopes to persuade the European Union and Japan to join its crusade to counter excess global steel capacity. But Washington’s partners may instead choose to stand up to its blatant protectionism and push back against the United States under the auspices of the WTO.

The United States’ opening trade move may be to target overcapacity, but intellectual property will be high on its list of concerns as well. Under a Section 301 investigation into whether China’s technology transfer and investment requirements of American firms operating inside its borders are discriminatory, Washington will take action against Beijing — both within and beyond the bounds of the WTO. (The investigation must wrap up by August, but Washington may release its findings before then.) The United States is already entertaining some legally questionable moves, such as declaring a national emergency [6] in response to China’s intellectual property violations, to impose punitive measures and erect safeguards around certain U.S. industries like consumer electronics, household appliances and automotives. Along with Europe, it will also continue to block Chinese investments in the tech sector as it sees fit, pointing to national security as its motive.

China, of course, won’t take Trump’s trade jabs lying down. In addition to imposing its own restrictions on some U.S. agricultural goods, Beijing is likely to selectively apply regulatory pressure on American companies with stakes in China. And when the time comes for Beijing to negotiate with Washington, it will have a handful of concessions — expanding U.S. access to the Chinese market and boosting Chinese imports of U.S. goods in certain sectors, to name a few — to offer. The external pressure mounting against China’s economy may even accelerate the country’s ongoing attempts to tackle overcapacity at home.

Though the White House may be willing to stomach the political risk attached to tariffs that ratchet up metals prices for U.S. industrial consumers, it will show more caution as it navigates North American trade negotiations. The ongoing NAFTA talks will stretch beyond this quarter, thanks to major sticking points on rules of origin requirements for the auto sector and to Canada’s more assertive stance against the United States. So far, domestic political checks on Trump’s actions have dissuaded the president from abruptly withdrawing from the pact. As he leans on more aggressive trade measures in the months ahead, overruling defenders of free trade within his administration, Congress will take on a more assertive role in regulating the country’s commerce abroad. Though U.S. lawmakers will have greater room to insulate existing free trade agreements, including NAFTA, their ability to counter unilateral tariffs leveled by the executive branch will be limited.

The White House’s trade policy will be one of several factors fueling market volatility [in the second quarter. Any uptick in expectations of inflation could lead to four hikes in U.S. interest rates this year instead of three. While by no means certain, this outcome would cause overvalued asset prices in U.S. equity markets to deflate. Higher interest rates could also strengthen the dollar and put more pressure on the central banks of the euro zone, Japan and China to tighten their monetary policies as they guard against the outflow of capital — with consequences for economic growth that could ripple across the globe.

Reining in Rogues and Rivals

The president’s approach to trade offers yet another example of his willingness to override the concerns of national security professionals within his administration on certain issues. Many have called for a more measured and targeted approach to avoid entrapping strategic U.S. allies and increasing the costs of U.S. defense. Still, as long as these voices remain in the White House, they will continue to restrain Trump’s responses to thornier foreign policy matters.

Among them will be nuclear containment. Despite worsening military friction between the United States and North Korea this quarter, a U.S. strike on the Korean Peninsula will remain an unlikely prospect — particularly given the promised summit between Trump and North Korean leader Kim Jong Un. Meanwhile, even as the United States urges Europe to threaten Iran with sanctions related to its ballistic missile program, Washington will stop short of tearing up Tehran’s nuclear deal altogether. But new nuclear proliferation concerns are emerging in the Middle East. Having already secured Russia’s stamp of approval for a preliminary roadmap, Saudi Arabia will use the Joint Comprehensive Plan of Action between Iran and global powers as a framework for a deal on a civilian nuclear program in the kingdom that includes domestic enrichment rights. Though it won’t be thrilled with the idea, the United States will work to ensure that it — rather than a rival like Russia — is best positioned to partner with allies in the Arab world that seek civilian nuclear programs of their own.

As it fends off Moscow’s encroachment in the Middle East, Washington will prepare for a more fundamental competition with Russia and China. At the beginning of the year, a series of U.S. defense reviews all but confirmed this by dubbing the two eastern giants the main strategic threats to the United States today. As the great power competition [9] takes shape, countries caught in the middle will have no choice but to adapt. Some, like Ukraine and Taiwan, will use the contest to fortify their alliances with the United States. Others, like the Philippines, will find it increasingly difficult to balance their relationships with both sides.

Spurred by their rivalry, the United States, China and Russia will continue to develop disruptive weapons technology. But rather than force all parties into compliance with existing arms treaties, this dangerous race is more likely to further degrade the deals [10] as time goes on. Accusations of violations will continue to fly between the United States and Russia as the pivotal Intermediate-Range Nuclear Forces Treaty steadily falls apart, undermining talks on the extension of the New Strategic Arms Reduction Treaty in the process.

A Mad Dash to the Cutting Edge

At the same time, the United States and China will jockey for the leading edge in artificial intelligence, which stands to have a profound impact on both military and civilian life. The United States is still ahead of China on this front, but Beijing is sprinting to catch up. And whereas big tech firms will have to contend with data privacy concerns and antitrust investigations in the West, China’s corporate giants will be largely unfettered in the mad dash for technological dominance [11].

Data privacy and its role in the evolving relationship among citizens, companies and states will take the spotlight in the European Union in the months ahead. Though European governments are particularly keen to protect the privacy rights of individuals, the Continent is simply too large a market for tech companies to avoid entirely. The General Data Protection Regulation set to take effect across the European Union on May 25 will thus set a global precedent for tech firms trying to navigate data privacy challenges.

The financial tech sector will follow the same path. Now that the speculative bubble around cryptocurrencies has burst, states will have more space to craft rules for cryptocurrencies, distributed ledger technology and initial coin offerings. Other industries — from supply chain management to insurance to health care — are beginning to adopt and regulate distributed ledger technology as well, albeit at a slower pace. Pending regulatory approval, a recently announced joint venture between IBM and Maersk Line shipping will bear watching because it may pioneer the use of block chain technology in the management of global supply chains.

As governments wrap their heads around the benefits of alternative currencies, more state-backed cryptocurrencies will crop up throughout the year, each driven by a different motive. For advanced countries, such as Estonia, cryptocurrency adoption is a natural step in digitizing their economies. For Iran and Russia, it could offer some insulation from the sanctions against them. Cryptocurrencies can also be useful to shambolic economies like Venezuela or Zimbabwe, where people have lost trust in fiat currencies, want to back their currencies with a commodity or hope to shield themselves from sanctions. And as small, dollarized countries like the Marshall Islands are discovering, cryptocurrencies can offer greater economic flexibility and an alternative to the dollar.

Old Challenges and New Appetites in Energy

The U.S. energy industry, a major steel consumer, will be hit hard this quarter by hefty steel tariffs that jack up its production costs — and at a time, no less, when U.S. oil output has broken records at over 10 million barrels per day. Though U.S. shale production may moderately decline as a result, it won’t be enough to ease the concerns of OPEC and its external partners, which have trimmed back their output in an effort to balance out the growing supplies of their American competitors. So far, production dips in Mexico, China and Venezuela are helping to offset the relentless climb in U.S. and Canadian output. OPEC and non-OPEC producers will probably extend their cuts through the end of the year when they meet in Vienna in June. The details of a longer-term agreement, led by Saudi Arabia and Russia, to counter U.S. shale production will likely emerge around the same time as well.

Elsewhere in the energy realm, demand for lithium-ion batteries — and the corresponding need for cobalt and lithium — is on the rise. At its heart is China, whose environmental reforms and technological drive are fueling the development and demand for electric vehicle batteries. But the world’s newfound appetite [15] for these resources will create a host of geopolitical challenges. This quarter, battery producers will have to grapple with new legislation in the Democratic Republic of the Congo, a major source of cobalt that will increase mining royalties owed to the government. And although Argentina and Chile are well-positioned to attract foreign investment into their lithium sectors, growing political instability in Bolivia will hurt its chances of doing the same.

Asia-Pacific

The Bell Heard ‘Round the World

For months, the nuclear threat rising from the Korean Peninsula has transfixed the globe, but during this quarter, a different issue will take center stage in Asia: China’s brewing trade spat with the United States. With Washington determined to bring Beijing’s behavior in line with its own agenda, it will ratchet up pressure by targeting China’s economy and strategic interests in the region — including its claim to sovereignty over Taiwan. Rather than take these measures lying down, China will retaliate, sounding the bell for a boxing match that will determine the moves and countermoves of smaller nations caught between the sparring giants.

The impending showdown has loomed for over a year. Throughout 2017, China parried most of the United States’ jabs by answering Washington’s calls to ramp up economic pressure on North Korea. To that end, Beijing scaled back its trade ties and severed its lingering financial connections with Pyongyang. But as North Korea accelerated its weapons development, China’s ability to shape events on the peninsula waned, eroding its ability to link trade matters to security issues [17] in the process. No longer able to fend off the United States’ blows, and faced with the maturation of several U.S. punitive trade measures against it, China could respond in kind by slapping tariffs on U.S. exports, including on agricultural and chemical products; by challenging U.S. measures at the World Trade Organization (WTO); and by pressuring American firms operating in China. All the while, Beijing will try to create room for negotiation with Washington by offering to open up Chinese markets and boost its imports of U.S. goods. Despite its best efforts, however, the United States will keep its sights trained on Chinese trade practices.

The timing of this feud couldn’t be worse for Beijing. On the heels of a crucial quinquennial transition in political leadership, China’s elite face the daunting task of pushing through a raft of delayed socio-economic reforms. Over the past few months, the country has taken advantage of its robust economic growth and stable trade ties to advance important aspects of a plan to shift its economic model away from credit-based investment and toward domestic consumption. Among these steps are deleveraging China’s financial system and deeply indebted state-owned enterprises, eliminating overcapacity in resource-intensive industries, and increasing the enforcement of environmental regulations.

As Beijing expands its reforms in the months ahead, the central government will concentrate on making sure that local governments and industries effectively enforce them. So far China’s attempts to curb informal lending and overhaul the bloated state-run companies at the heart of the nation’s debt crisis have fallen short at the local level; governments and companies there collectively hold debt equal to about 80 percent of China’s gross domestic product. Likewise, the implementation of environmental laws has been lackluster across the southern provinces and among a handful of industries, including steel and coal. Beijing will try to rectify these problems by stressing the importance of compliance but doing so will carry the risk of widespread failure caused by overly hasty implementation or by local resistance stemming from a desire to preserve economic growth and jobs.

Having cemented his grip on power, President Xi Jinping will have few excuses left for such failures. He will rely in part on the new National Supervision Commission to keep a sharp eye on local officials’ performance and ensure that they don’t botch the job. One issue will draw particularly close attention from Beijing: easing China’s massive local debt burden by correcting an imbalance between the fiscal responsibilities of the central and local governments. Since the start of the year, Beijing has made significant headway on its long-delayed tax reforms, in part by shoring up local tax bases. Though its centerpiece property tax likely won’t emerge until 2020, the Chinese government will continue to enact fiscal reforms, encourage domestic consumption, reallocate resources to underdeveloped regions and lighten corporate debt loads in the coming months — all with the aim of setting the Chinese economy down a more sustainable path.

Of course, a deepening trade dispute with the United States [25] will present a formidable obstacle on the road to reform. On March 23, Washington will impose high tariffs on U.S. steel and aluminum imports to protect itself from what it deems to be unfair trade practices by other countries, including China. Because only about 2 percent of U.S. steel imports come from China, the volume of these imports will remain fairly steady. But China, which accounts for roughly half of the world’s steel production, will still be hit hard as steel prices tumble and major exporters divert their supplies from the United States, snatching up a portion of China’s market share along the way. To make matters worse, Washington’s actions could inspire European countries and Japan to erect their own trade barriers against China to protect producers at home. Each new source of strain could damage China’s steel industry, potentially reducing employment in the sector and undermining Beijing’s ability to address stubborn overcapacity issues.

Steel and aluminum tariffs aren’t the only weapon at the United States’ disposal, either. Washington could opt to establish tariffs or import quotas on major Chinese exports, such as electronics. It may also charge hefty fines intended to alter China’s market restrictions and intellectual property practices. Each of these tactics would become even more effective if the United States were to join forces with the European Union and Japan — a scenario China is undoubtedly eager to avoid. But try as it might, Beijing’s efforts to open up its services, finance and manufacturing industries to the rest of the world won’t satisfy Washington’s demands or discourage its scrutiny of Chinese investment in the high-tech sector.

Regardless of which means the United States uses to achieve its ends, China will have to expend more and more resources to prop up its precarious economy. And as its funds run low, Beijing will be forced to compromise on some of its key economic objectives. For instance, should Washington’s measures chip away at China’s growth or employment figures, Beijing may back off its planned production cuts and environmental reforms, or it may use lines of credit to buoy the economy. In the direst circumstances, the central government could even bolster the real estate market, potentially creating a real estate bubble and, in the long run, the heightened risk of a national debt default.