This quarter focuses on key globalization issues including worker replacement with robotics, economic hurdles in China and India, container shipping meltdown. Thankfully no news on “The Donald”

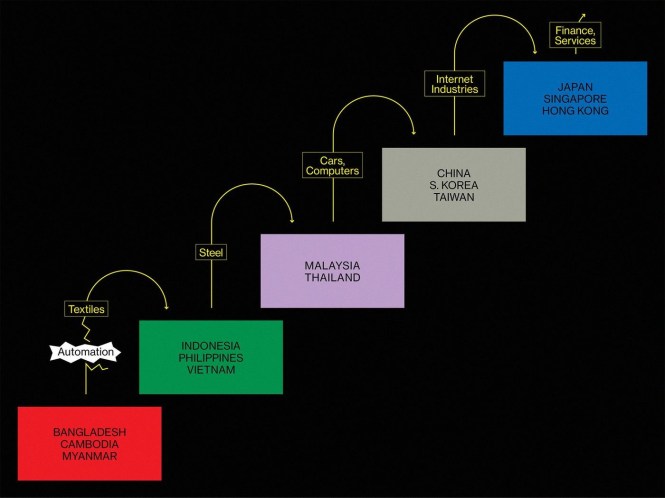

Bloomburg Report on JOBS -ASEAN Factory workers displacement with Robots

Illustration: Traditional Manufacturing Succession in Asia. Progression of wealth building for Factory workers leading to the growth of middle class workers -DBW

Kevin Hamlin and Dexter Roberts June 21, 2017 2:00 PM

Thirty minutes by car into the scrubby desert outside Korla, in China’s remote Xinjiang region, a textile manufacturer owned by Jinsheng Group is building its latest factory complex. Inside the 16 billion-yuan ($2.4 billion) facility—a collection of stark white warehouses surrounded by an enormous expanse of pristine artificial grass—are rows of huge cotton spools, more than a million bright red and blue spindles, and almost no people. A few German engineers wander around, making sure the equipment runs at peak efficiency. This is the depopulated future of an industry that’s lifted millions of Asians out of poverty.

Jinsheng’s factory covers almost 15 million square feet, more than five times the floor area of the Empire State Building, but it needs only a few hundred production workers for each shift. “Textiles used to be a labor-intensive industry,” said Pan Xueping, the chairman and chief executive officer, in a September speech in Urumqi, Xinjiang’s capital. “We are at a turning point.” Instead of moving production to whatever nearby country has the lowest wages, he added in an interview a day after the speech, “the industry can achieve a human-free factory.”

Pan’s company is at the vanguard of a trend that could have devastating consequences for Asia’s poorest nations. Low-cost manufacturing of clothes, shoes, and the like was the first rung on the economic ladder that Japan, South Korea, China, and other countries used to climb out of poverty after World War II. For decades that process followed a familiar pattern: As the economies of the early movers shifted into more sophisticated industries such as electronics, poorer countries took their place in textiles, offering the cheap labor that low-tech factories traditionally required. Manufacturers got inexpensive goods to ship to Walmarts and Tescos around the world, and poor countries were able to provide mass industrial employment for the first time, giving citizens an alternative to toiling on farms.

“The window is closing on emerging nations. They will not have the opportunity that China had in the past”

Today, Bangladesh, Cambodia, and Myanmar are in the early stages of climbing that ladder—but automation threatens to block their ascent. Instead of opening well-staffed factories in these countries, Chinese companies that need to expand are building robot-heavy facilities at home. “The window is closing on emerging nations,” says Cai Fang, a demographer in Beijing who advises the Chinese government on labor policy. “They will not have the opportunity that China had in the past.”

The transformation looks like it will happen fast. The International Labor Organization (ILO) estimates that mass replacement of less-skilled workers by robots could be only two years away. Overall, more than 80 percent of garment industry workers in Southeast Asia face a high risk of losing their jobs to automation, according to Chang Jaehee, an ILO researcher who studies advanced manufacturing. Chang recalls presenting her findings to a government official in a country in the region that she declines to name. The official’s response? If she’s right, the result could be civil unrest.

Until recently, even as robots took over much of the manufacturing of larger goods such as cars and jet engines, the prospect of applying automation to towel-weaving or dress-stitching looked like a long shot. Sewing clothes is a delicate undertaking. Making a seemingly simple dress shirt with a breast pocket can require 78 separate steps, and machines that can match the dexterity of human fingers are still a costly rarity. What’s more, tech entrepreneurs had little incentive to design automated systems for a low-margin industry with ample access to cheap labor and little cash to spend on sophisticated gear.

These factors have led to complacency in parts of the textile industry. “Today, there is no equipment that can make these handmade products,” says Sahil Dhamija, whose Sahil International produces bathmats and bed linens for export at a factory in Panipat, India, that employs about 500 people. He spoke at the Canton Fair, a trade conference in Guangzhou, China, in May.

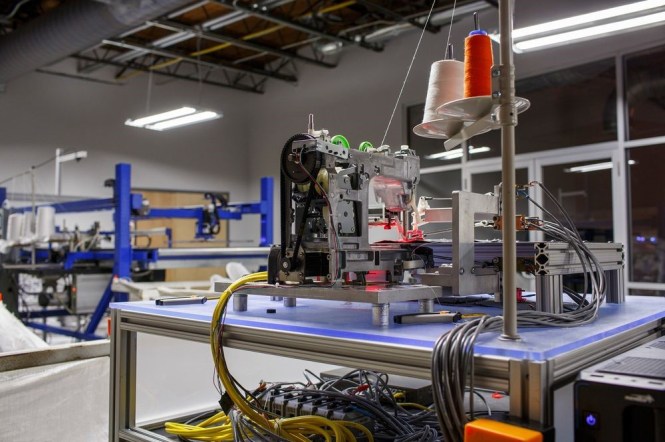

Dhamija might want to visit Atlanta. A group of Georgia Tech engineering and robotics professors founded a startup called SoftWear Automation there in 2007, with the goal of overcoming the difficulties machines have in picking up flexible fabric and pinpointing where to stitch and cut. SoftWear’s first prototype took seven years to develop, sustained in part by a $1.75 million grant from the Defense Advanced Research Projects Agency, a Pentagon group that pushes bleeding-edge development. In 2015 the company made the first sales of its invention, the Sewbot, to customers in the U.S. Revenue last year rose 1,000 percent, and it’s on track to do the same in 2017, according to CEO Palaniswamy “Raj” Rajan.

The breakthrough was as much about vision as touch; before SoftWear’s robots could make clothes accurately, they needed to learn to see garments as a collection of fine folds and details, rather than undifferentiated blobs of fabric. For now, the Sewbot can handle products including towels, mattress covers, and pillows, which require 10 steps or fewer to produce. But the company is at work on upgraded machines that can create T-shirts and eventually more complicated garments such as jeans and dress shirts. The ultimate goal, Rajan says, is “full automation, from a roll of material to finished product.” He says he has preliminary interest from clients in China, South Korea, Japan, and other countries across Asia.

SoftWear Automation’s sewing-machine robot prototypes at the startup’s offices in Atlanta.

Photographer: Melissa Golden/Redux

As automation accelerates, it’s not just Asia that could see its industrial trajectory affected. If the cost of labor is no longer a major factor, there’s no reason manufacturers can’t relocate production to where the bulk of their customers are: North America and Europe, where wages for decades have been too high to support textile production. Remove most of the workers from the equation, along with the costs and delays of round-the-world shipping, and making clothes or shoes in Dallas or Düsseldorf instead of Dhaka starts to look like a compelling idea.

German sportswear giant Adidas AG moved some shoe production to a highly automated “speedfactory” in its hometown of Ansbach that’s scheduled to begin large-scale operations this year. The company plans to open a similar plant in the U.S. In May, China’s Shandong Ruyi Technology Group Co., the owner of luxury brands such as Sandro and Maje, announced that it would invest $410 million in a textile plant in Forrest City, Ark. “Automation essentially levels the playing field,” says Frederic Neumann, co-head of Asian economics research at HSBC Holdings Plc in Hong Kong. “What emerges is a giant strategic game, in which individual governments will seek to attract industries to set up shop locally.”

The losers are likely to be poor countries that were counting on large-scale manufacturing employment to build prosperity. As wages rose in China, Transit Luggage Co., a suitcase maker based in the southern city of Dongguan, explored two options: moving production to low-wage Vietnam or investing in automation at home. Executives chose the latter. One robot now matches the output of about 30 workers making soft luggage, says sales manager Yang Yuanping. As a result, she says, the company employs fewer workers than it did a decade ago, while producing three times as many items.

Even that pace of production is no guarantee of survival in a fast-innovating industry. Yang has begun to worry about competition from Poland and the Czech Republic, as automation allows European countries to compete on price for the first time. “We have to think about how we can beat them,” she says. “We know they will get the machines.” —With Jason Clenfield and Bloomberg News

(Chandan Khanna/AFP/Getty Images)

Series Introduction:

As each country tries to find the best way to thrive in the global economy, it must consider its comparative advantages. Take Brazil, for example. Like many other countries in North and South America, Brazil has an abundance of land that it exploits efficiently through large, modern farms. Japan, on the other hand, is light on land but has a wealth of capital at its disposal. And India’s biggest strength is its massive — and growing — labor pool. These disparate assets help determine not only a country’s economic development but also its stance on trade.

Every international trade negotiation starts out with a goal and a price. The goal is typically to open up an area of another country or bloc’s economy that could benefit the nation driving the negotiations. In return, the negotiator must pay a price, often by opening a sensitive part of its economy to the other party’s products. But even while pursuing its offensive interests in trade talks, a state must also consider its defensive interests — less competitive areas in its domestic economy that it must shield against foreign competitors, lest they overwhelm the sector. Defensive interests are sometimes more strategic; Japan, for example, has long protected its agricultural sector as a way to ensure its self-sufficiency in the event of a trade disruption. Either way, the industries that fall under a country’s defensive interests often have outsize political influence and powerful lobby groups on their side to resist liberalization.

Global trade, meanwhile, is changing. The kinds of multilateral agreements that characterized the postwar years have stalled out over the past two decades, prompting countries and economic blocs to try to negotiate smaller deals with fewer partners. Nations and blocs have more leeway under this new model to negotiate the trade agreements that best suit their interests and to avoid those that don’t. Now, more than ever, the future of international trade depends on a country or bloc’s defensive interests, offensive interests and underlying factors of production. Our fortnightly Trade Profiles aim to break down these factors to facilitate an understanding of where global trade stands today and where it’s headed.

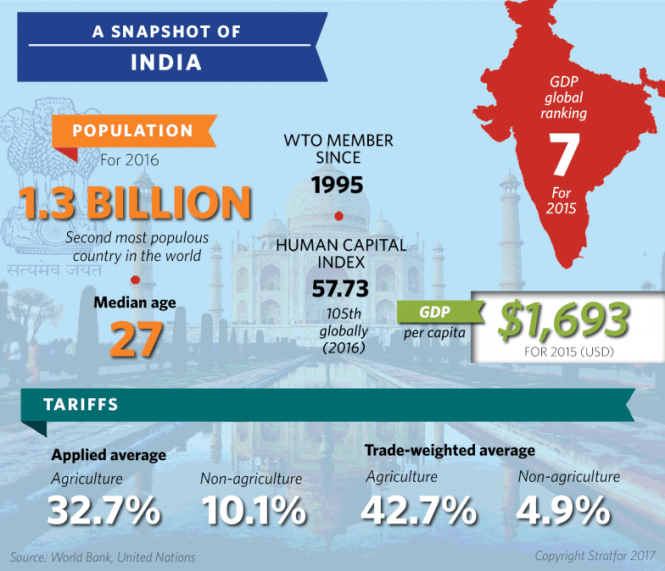

In this first installment, we focus on India.

Economic Background

India has traditionally taken a defensive stance on trade. Its first leaders adopted a closed economic model when the country gained its independence in 1947. Wary of external influence following centuries of imperial domination, the newly minted government instated rules to prevent majority foreign ownership of Indian companies and erected formidable trade barriers. These, along with high taxes and extensive domestic regulations, restrained the market. Protected from external competition and undermined by chronic government corruption and poor infrastructure, Indian industry became deeply noncompetitive. One notable exception was the pharmaceuticals sector, in which the government’s disregard for foreign patents created a nimble and innovative industry based on reverse engineering and reproducing Western goods.

Agriculture was also of high political importance, given India’s closed and poor economy and its largely rural population. Domestic farmers, however, struggled to feed the country, which for a time relied on agricultural donations from the United States to avoid famine. The Green Revolution of the 1960s transformed agricultural productivity, banishing the specter of famine — but also creating a need for government subsidies to sustain the burgeoning farming industry. The farm lobby steadily amassed influence in India; Charan Singh, in fact, rose out of the camp to rule the country for a brief stint as prime minister in 1979, and huge farmers’ marches characterized the 1980s.

Then in 1991, an economic crisis in India, along with the fall of the Soviet Union, signaled an abrupt change. The government toppled tariff barriers, eased regulations, cut taxes and opened up much of the country’s economy to international competition during a three-year liberalization campaign. Companies around the world entered the market in force, sending India’s share of global foreign direct investment from 0.5 percent in 1992 to 2.2 percent in 1997. (The movement stopped short of a full revolution, though; extensive regulations and widespread corruption still hampered the economy, while rules limiting foreign direct investment — and investment in India’s capital market — remained in place.) India has signed 84 bilateral investment treaties since 1994, a number consistent with the overall global trend.

The reforms of the 1990s cost Indian farmers some of their clout. The sectors that thrived under the country’s economic liberalization were the newer industries, such as information and communication technology, that the old regulations least affected. India’s relatively low labor costs and large number of English speakers made it a natural hub for business process outsourcing, and today, the country ranks fifth among the world’s top services exporters (discounting trade within the European Union). Agriculture, meanwhile, lost ground in the Indian economy — it accounted for just 18 percent of the country’s gross domestic product in 2014 compared with 52 percent in 1950. As agriculture declined, debt levels climbed among India’s farmers. The mounting financial pressures led to high suicide rates in the sector; more than 270,000 farmers have killed themselves since the mid-1990s, causing widespread consternation. The industry, after all, is still politically relevant, since more than two-thirds of India’s population lives in rural areas. To try to address the problem, Uttar Pradesh’s new chief minister decided to forgive all farming loans in his state, which stand at $5.6 billion total, or 2.5 percent of India’s GDP.

The liberalization did little to boost India’s manufacturing industry, either. Poor infrastructure and uncompetitive labor costs relative to countries such as China, Vietnam and Bangladesh have held the sector back. Today, India’s merchandise exports account for just 1.6 percent of the total trade, while its exports of information and communication technology, for instance, make up 17 percent of the total worldwide. The pharmaceuticals sector, by contrast, has continued to boom in the wake of the reforms, even if they curbed its freedom. On joining the World Trade Organization in 1995, India had to sign the Agreement on Trade-Related Aspects of Intellectual Property Rights, or TRIPS, which protected foreign patents in the industry. But since the agreement took effect in 2005, Indian pharmaceutical companies have drawn on the skills they learned in their days of replicating drugs at a lower cost to make their country the world’s leading exporter of generic medications.

And remittances have also grown substantially since India liberalized its economy. The country’s sizable diaspora — now the world’s largest — dates back to colonial times. But as new opportunities have arisen for Indian software engineers in countries such as the United States, and capital controls have relaxed, personal remittances to India skyrocketed from $2.4 billion in 1990 to $70.4 billion in 2014. Half of the money comes from Indians working in Arab states, including the United Arab Emirates, Saudi Arabia and Kuwait.

Trade Implications

Defensive Interests

Notwithstanding the reforms that India undertook in the early 1990s, its trade policy has long centered on resisting liberalization. Antipathy toward free market competition extends to a societal level in India, and in the decades after its period of liberalization, the country largely reverted to its defensive ways. In 2001, for instance, India’s staunch opposition to the lower trade barriers proposed in the WTO’s Doha Development Round contributed to the negotiations’ failure.

The agricultural sector is the primary focus of India’s protectionism. With a mean farm size of only 1.33 hectares (about 3.3 acres), India can’t compete in the global market against countries in South America, where farms average 50.7 hectares, or North America, whose farms cover 186 hectares on average. India paid out an estimated $51 billion in agricultural subsidies in 2011-12, putting it on par with Japan, though its economy is only half as large. India’s applied agricultural tariffs of 32.7 percent dwarf those of its fellow BRICS — Brazil, Russia, China and South Africa, countries recognized for their rapid economic growth and potential. If New Delhi continues down this path, its refusal to reduce agricultural tariffs could keep new trade partners away. Proposed regional trade agreements such as the Regional Comprehensive Economic Partnership (RCEP), after all, emphasize tariff reduction, particularly on commodities.

Investment is also emerging as another target of India’s protectionist policies. Over the past 14 years, the country has brought 21 dispute cases against investors — a sharp increase, albeit one that conforms to global trends. (State-investor disputes tripled between 2005 and 2015, though countries, and particularly developing nations, are usually the defendants in these suits.) India has lost 80 percent of its cases, prompting New Delhi to express its dissatisfaction with the process. The country went so far as to scrap 57 existing bilateral investment treaties in 2016 in hopes of renegotiating them under the new contract model it introduced the previous year. Then this year, it blocked discussion of multilateral investment facilitation at the WTO on the grounds that the measure would limit its policy options.

New Delhi is even more eager to protect its pharmaceuticals sector, something else that could cause strife with its trade partners abroad. Many developed countries are pushing to extend the patent terms for pharmaceutical products through so-called TRIPS+ trade agreements. But because longer patent terms would cut into India’s booming generics business, New Delhi will resist the initiative. The country’s labor standards, too, could create problems. Recent multilateral trade agreements, such as the Trans-Pacific Partnership, have included prescribed labor standards. India, which ranks 105th on the Human Capital Index, may struggle to meet the new requirements.

Offensive Interests

Nevertheless, demographics could force India to resist its protectionist impulses. Compared with countries such as China, whose population will peak in 2028, India has a much younger demographic profile. A projected 280 million people will flood the workforce by 2050. Already, roughly 1 million people are entering India’s workforce each month, a rate that far exceeds the country’s job creation. In 2015, for example, India created just 135,000 new jobs. And though that year was particularly slow, even in 2009 — the best year for job growth in recent history — the country managed to add just 1.2 million positions. The situation could lead to massive unrest if India’s leaders don’t find a way to address it.

Other developing countries have traditionally relied on manufacturing to employ growing populations. Japan, South Korea, Taiwan and China all achieved solid export-led growth by rising gradually through the value chain from textiles to cars to advanced engineering. India, however, is in no position to follow their example. In addition to its relatively high wages and deficient infrastructure, the country has a dearth of available land, making it ill-suited to industries such as manufacturing. And the problem will only get worse as the population keeps growing. India’s shortcomings aside, though, the age of manufacturing-driven economic development also seems to be reaching its end. More and more, the world is spending its disposable income on services rather than goods, while the manufacturing sector itself is yielding increasingly to automation.

Yet New Delhi has not given up on manufacturing. Prime Minister Narendra Modi’s administration, in fact, has made boosting India’s manufacturing industry one of its main priorities through the “Make in India” campaign. Under the initiative, the government has eased restrictions on foreign investment in the defense, railway, civil aviation, broadcasting and pharmaceuticals sectors. It has even taken some tentative steps toward liberalizing India’s capital markets (although foreign financial services still face significant barriers). New Delhi has revived ambitious infrastructure projects, as well, and the Goods and Services Tax bill, introduced this year, stands to facilitate the transport of goods across state borders, once India’s state legislatures approve it. The legislation could inspire the country’s trade negotiators to prioritize reducing barriers to exports of manufactured goods in future talks.

The country’s services sector, meanwhile, is probably India’s best bet for coping with its demographic problem. The industry is hardly a silver bullet, considering that large swaths of the population are still illiterate and don’t speak English. Still, strong competitiveness has created a $33 billion trade surplus in services — compared with a $126 billion trade deficit in goods — and external demand promises to increase in the future, given the global market’s development. An added benefit is that services can often be performed by an Indian worker living abroad, an arrangement that would not only cut down on the number of jobs to be created domestically but could also further increase remittances.

With these factors in mind, India has recently shifted to a more offensive stance to further open the services sector. The country has been working to make it easier for Indians to move across borders for work through its free trade agreement negotiations. Last year, it proposed a multilateral trade facilitation in services deal at the WTO (following the signing of an equivalent agreement over goods in 2013) that would, among other things, encourage relaxed visa restrictions. But in a global climate in which immigration has become a highly charged subject, particularly in the developed world, India’s focus on sending its workers abroad is likely to meet some resistance from potential trading partners.

A model of the Forest City development at the Country Garden showroom in Johor, Malaysia.

Photographer: Ore Huiying/Bloomberg

The $100 Billion City Next to Singapore Has a Big China Problem

Beijing’s capital controls are spooking some property buyers

Bloomberg News June 22, 2017 3:00 PM

The $100 billion city rising from the sea next to Singapore has hit a roadblock: China’s capital controls.

The dream of a Malaysian version of Shenzhen — largely funded by Chinese developers and buyers — with hotels, offices, golf courses, tech parks and thousands of ritzy new apartments, is having to adapt after China’s government clamped down on an exodus of money for investment in overseas property.

Developers’ sales offices in China that once brought in buyers by the hundreds are now pushing developments in Chinese cities. Subsidized junkets that flew in prospective buyers to development sites in the southern Malaysian state of Johor have dwindled. And some buyers who paid deposits for yet-to-be-built homes are considering canceling their purchases.

“I feel I’m on the horns of a dilemma,” said Michelle Gao, who paid about 600,000 yuan ($87,825) toward the 1.2 million yuan cost of a two-bedroom apartment at Country Garden Holdings Co.’s vast Forest City development. “If the project relies so much on Chinese buyers like me, how on earth are they able to sell in future? Will the construction ever finish?”

Country Garden’s “Forest City” development project in the Iskandar region of Johor, Malaysia.

Photographer: Ore Huiying

The crackdown on outflows of money from China has spooked some buyers. While Chinese citizens are allowed an annual foreign exchange quota of $50,000, the government said in December that all buyers of foreign exchange must sign a pledge that they won’t use their quotas for offshore property investment. Violators would be added to a watch list, denied access to foreign currency for three years and be subject to a money-laundering investigation.

The restriction threatens to take the wind out of residential property sales in cities around the world where prices have been driven in the past few years by buyers from China. Few projects are likely to be affected as much as the Chinese-financed developments in Johor, some of which had relied on mainland customers for as much as 90 percent of sales.

Six Chinese buyers interviewed for this story said they paid a 10 percent down-payment to Country Garden in showrooms in China by swiping debit or credit cards or using payment services like Alipay. They said the property agents are now telling them they need to go to Hong Kong, Singapore, Malaysia or Macau to swipe their cards to pay the balance of installments, or wire funds to Country Garden’s overseas accounts.

Top: Potential buyers walk around a model of the Forest City showroom development as lines of buses ferrying would-be buyers sit parked outside in November 2016. Bottom: The same showroom during an event in June this year.

Photographer: Ore Huiying/Bloomberg

Many are worried that would still make them liable under China’s foreign exchange rules. This month, the Chinese government said domestic banks will have to provide daily reports of clients’ overseas transactions of more than 1,000 yuan.

“I was told it can still be done from Hong Kong, but I’m just scared now,” said buyer Elaine Xiao. “I don’t know what punishment I may get.”

Country Garden said the controls have not had a material effect on sales and construction at Forest City is continuing. It has completed a luxury hotel and handed over the first batch of 132 apartments on May 1.

The Johor developments stem from Iskandar Malaysia, a government effort to leverage Singapore’s success by building a new metropolis near the causeway that connects the island state to the Malaysian city of Johor Bahru. When the 20-year project was announced in 2006, it envisaged a total investment of 383 billion ringgit ($87 billion) and much of the early investment came from Singapore.

But then Chinese developers like Country Garden and Greenland Holdings Group Co. moved in with projects that dwarfed those of their Malaysian and Singaporean rivals. Country Garden’s “Forest City” alone called for a $100 billion high-rise town to be built on artificial islands within a few hundred yards of Singapore.

The projects were marketed in China, and thousands paid deposits for apartments that cost as much as double the rate per square meter of homes for Malaysian buyers in Johor Bahru.

A buyer whose family name is Yu said she doesn’t intend to pay the next installment on her apartment when it comes due this month. She said her agent advised her to swipe her credit card in Hong Kong to get around the rules. “I asked the sales agent will you take responsibility when I’m blacklisted in China?”

Yu, from Guangzhou, put down a deposit on a 1.2 million yuan, 59-square-meter apartment in Phase III of the project while visiting the vast landscaped sales gallery at the construction site in December. She’s among those now considering walking away from the agreement because of concern about breaking the rules.

Ongoing construction at Country Garden’s “Forest City” development.

Photographer: Ore Huiying/Bloomberg

Country Garden announced on June 20 it would proceed with stage 2 of the Forest City development, a $280 million plan that includes golf courses, an international school and another hotel. The developer said in April it was in discussion with fewer than 60 Chinese buyers who indicated their intention to cancel bookings. The company said it sold 16,000 residential units in Forest City last year.

Country Garden said earlier it had stopped marketing Forest City in its sales galleries in China and ceased organizing tours to its Johor projects for would-be buyers. Its agents in China are pushing domestic projects in the country’s tropical southern resort of Sanya and the seaside city of Beihai.

The developer said it has opened Forest City showrooms in Singapore, Kuala Lumpur and Jakarta, and plans to open more this year in Vietnam, Myanmar, Taiwan, Thailand, Japan, Dubai, the Philippines and Laos.

Construction at Greenland’s Jade Palace development was suspended in November while the company considered revising the project density to build more, but smaller apartments, according to a sales agent with knowledge of the project. No construction work was going on during a weekday visit to the site in May.

A show apartment at the Tropicana Danga Bay property showroom.

Photographer: Ore Huiying/Bloomberg

In a response to written questions, Greenland said on June 3 that construction had not stopped and that the design of the apartments will be optimized pending feedback from previous buyers. It declined to give sales figures, but said it is looking for more buyers outside China.

Samuel Tan, executive director at KGV International Property Consultants, said approvals for all new serviced apartments in Johor have been frozen since 2014 and existing projects were introducing more affordable properties at around 600,000 ringgit instead of 800,000 to 1 million ringgit.

“Given the oversupply, we don’t foresee any recovery until 2019 for high-rise projects,” Tan said. He said China’s capital controls were only significant to the Chinese-owned projects.

The glut of properties being built in Johor has also affected local developers, Petaling Jaya-based Tropicana Corp. is giving a 25 percent rebate on the list price of homes they are marketing an interest-free, 36-month deferred payment plan. Resale asking prices of properties in Johor have dropped 2 percent in the past two years, according to real estate listings website PropertyGuru.com.

Yu, the buyer from Guangzhou, worries that the thousands of apartments still to be built at Forest City will be hard to sell without Chinese buyers.

“My home is still in the ocean,” Yu said. “Locals will not buy homes with prices double the local rate. Without enough residents from China, everything will change.”

Construction continues on reclaimed land at Country Garden’s “Forest City”, with Singapore in the background.

Photographer: Ore Huiying/Bloomberg

India’s prime minister is not as much of a reformer as he seems

But he is more of a nationalist firebrand

Japan Economy & Housing Starts

By Shawn Lawlor

Director, Canada Wood Japan

May 29, 2017

Posted in: Japan

Japan Q1 GDP grew at an annualized 1.2% rate. February industrial production posted a solid growth of 4.7%. February unemployment held at 2.8%, its lowest level since the early 1990s. The consumer price index edged up 0.2% in February. Japan posted a large current account surplus of US $187 billion in February. Japan’s GDP growth forecast for 2017 is at 1.2%.

Japan Housing Starts Summary

Japanese Monthly Housing Starts Summary for January 2017

January total housing starts increased 12.8% to 76,491 units thanks primarily to a jump in rental housing. Rental housing saw growth of 12% compared to a decline of 0.2% in owner occupied housing. January results were boosted by a 38% surge in non-wood housing. Wooden housing gained 4.2% to 39,079 units. Of wooden housing, post and beam starts increased 4.9% to 29,714 units; wooden pre-fab declined 12.8% to 1,057 units, and 2×4 starts gained 4.0% to 8,308 units. Two by four owner occupied custom homes advanced 6.6% to 2,260 units, multi-family apartments increased 2.0% to 4,901 units and built for sale spec homes grew 6.6% to 1,129 units.

Japanese Monthly Housing Starts Summary for February 2017

February housing starts trailed 2.6% to finish at 70,912 units. Total wooden starts edged up 2.5% to 39,587 units, however the non-wood “mansion” condominium market fell 35.7% after experiencing a surge the month prior. Post and beam starts improved 3.4% to 30,023 units. Wooden pre-fab starts were flat at 1,057 units. Two by four starts declined 0.3% and broke down as follows: custom owner occupied declined 4.2% to 2,220 units, built for sale spec homes dropped 10.4% to 970 units and rentals improved 4.3% to 5,303 units.

Japanese Monthly Housing Starts Summary for March 2017

March total housing starts registered a faint increase of 0.2%, finishing at 75,887 units. Although owner occupied housing starts fell 3.6%, rentals posted an 11% gain. Rental housing recorded a 17thconsecutive monthly gain. Total wood starts posted a small 0.9% gain thanks to strength in the post and beam segment. Post and beam starts increased 2.9% to 31,471 units. Wooden pre-fab starts slid 7.4% to 949 units. Two by four starts declined 4.6% to 9,116 units broken down as follows: custom built owner occupied fell 8.0% to 2,161 units; rentals gained 0.5% to 5,921 units and built for sale spec homes declined 5.0% to 1,011 units.

South Korean Economy, Housing & Lumber Shipments

By Tai Jeong

Technical Director, Canada Wood Korea

May 29, 2017

Posted in: Korea

Economy Update

Owing to increased construction investment and exports, South Korea’s economy grew at a fast pace in the first quarter of 2017 showing a 0.9% GDP increase from the previous quarter. Both construction and facility investments grew 5.3% and 4.3% respectively in the first quarter from the previous quarter.Gross domestic income rose 2.3% in the first quarter of 2017 from the previous quarter, compared with a 0.8% expansion three months earlier.

On a steady recovery in exports, South Korea posted a trade surplus for 63 straight months in April since February 2012 showing a surplus of US$13 billion with 24.1% on-year increase in exports to US$51 billion and 17.3% on-year increase in imports to US$38 billion.South Korea’s consumer prices increase 1.9% in April, slowing down from the previous month’s 2.2% rise amid high-flying oil prices. Unemployment rate hit a 17-year high at 4.2% in April, up 0.3 percentage point from the same month last year.

The exchange rate for Canadian Dollar averaged at 844.08 won in April, 2017, down by 5.52% from 893.35 in April, 2016 and also slightly down by 0.44 % from 847.85 in one month earlier.

Housing Construction

South Korea’s housing starts in number of buildings for the first three months of 2017 decreased 2.7% to 23,574 buildings from a year earlier 24,224 buildings while that in number of units significantly decreased 15% to 100,124 units from a year earlier 117,742 units.

Housing permits in number of buildings for the same period of 2017 also decreased 0.6% to 27,825 buildings from a year earlier 28,005 buildings while that in number of units significantly decreased 13.4% to 141,100 units from a year earlier 163,009 units amid ongoing government intervention to limit the supply of new homes, especially new apartments in Seoul, as a way of limiting the rise in household debts.

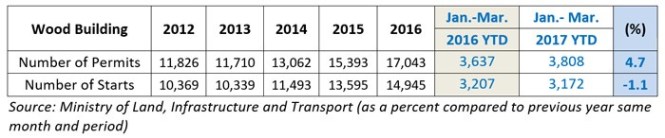

Though the overall residential construction sector struggles, the number of wood building permits for the first three months of 2017 increased 4.7% to 3,808 buildings from a year earlier. However, the number of wood building starts for the same period slightly decreased 1.1% to 3,172 buildings.

Both total floor areas of wood building permits and starts for the same period in 2017 increased 12.5% and 5.8% to 368,703 m2 and 303,770 m2 respectively from a year earlier.

Lumber Shipments

BC softwood lumber export volume to South Korea for the first three months of 2017 decreased 14.2% to 68,876 cubic meters as compared to 80,311 cubic meters for the same period of 2016.

Export value for the same period also decreased 9.9% to CAD$18.264 million as compared to CAD$20.285 million for the same period in 2016.

BC Softwood Lumber Exports to South Korea

2014/2016 Cumulative

According to the data from Korea Forest Service, Chile continued to be ranked as the number one lumber export country for the first three months of 2017 with a 44.1% increase to 162,680 m3 followed by Russia with a 16.4% decrease to 91,480 m3 and Canada with a 26.4% decrease to 39,850 m3.

Germany ranked as the 4th largest lumber export country with a remarkable 104.5% increase to 37,850 m3 followed by New Zealand with a 24.9 decrease to 25,870 m3 and Finland with a 64.9% increase to 21,540 m3.

Amid historically low levels of lumber prices in European countries, European mills continue to gain lumber market share in South Korea, especially as they increase their volume of kiln-dried and higher-grade lumber. These factors pose a growing threat to Canadian lumber export to South Korea.

China Makes Historic Strategic Move

By Edward Zheng

Research Manager, Canada Wood China

May 25, 2017

Posted in: China

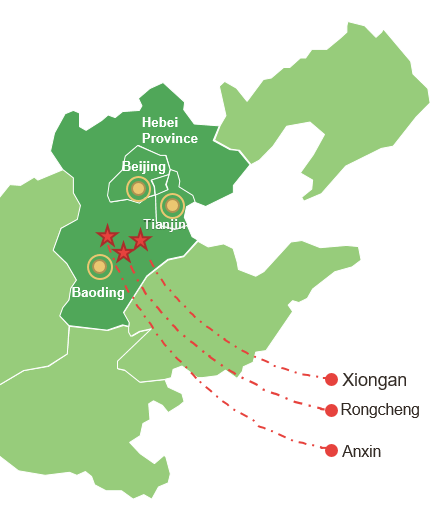

Xi Jinping announces Xiongan New Area of Hebei Province as part of a measure to advance the development of the Beijing-Tianjin-Hebei region.

In April, China announced it will establish the Xiongan New Area in Hebei Province, as part of measures to advance the coordinated development of the Beijing-Tianjin-Hebei region.

What is Xiongan New Area (XNA)?

On April 1st 2017, the Central Committee of the Communist Party of China (CCCPC) and State Council announced to establish a new satellite metropolitan district in Xiong’an., the Xiongan new area is comparable to the Shenzhen Special Economic Zone and the Shanghai Pudong New Area. According to the official circular, the new area will initially cover around 100 km2 and will be expanded to 200 km2 in the mid-term with plans for further expansion of 2,000 km2 in the long term.

The move is a “major historic and strategic choice made by the Central Committee of China’s Communist Party State Council with Comrade Xi Jinping as the core,” said the circular, which described the decision as “a strategy crucial for a millennium to come.” [1]

What are the main functions of Xiongan New Area?

- Help phase out functions from Beijing that are not related to the capital

- Explore a new model of optimized development in densely-populated areas

- Restructure the urban layout in the Beijing-Tianjin-Hebei region

- Build Xiongan into “a demonstration area for innovative development”

- The area feature geological advantages, convenient transportation, an excellent ecological environment, ample resources and lots of room for development

Xiongan is located approximately 100 kilometers southwest of downtown Beijing, the Xiongan New Area covers the counties of Xiongan, Rongcheng and Anxin, and is home to Baiyangdian, one of the largest freshwater wetlands in North China.

Significance? One of the reasons for developing the Xiongan district is that the region would serve as a high-technology hub for the Beijing-Tianjin-Hebei (Jing-Jin-Ji) metropolitan region. In fact, the government is looking to use the most advanced world-class standards and technologies to build the city; Xiong’an will serve as a so-called “iconic project” for the township initiative. The interest in showcasing cutting-edge green technologies may open opportunities for CW China to introduce wood technologies to this massive development.

Xiongan District

[1] From China Daily: http://www.chinadaily.com.cn/china/2017-04/01/content_28774796.htm

China Economy, Construction & Lumber Shipments

By Eric Wong

Managing Director, Canada Wood China

May 3, 2017

Posted in: China

March highlights:

China plans to build a “first-class international city” called “Xiong’an New Area” from scratch which will cover 2,000 square kilometers, making it almost 300% larger than New York City or Singapore

China plans to build a “first-class international city” called “Xiong’an New Area” from scratch which will cover 2,000 square kilometers, making it almost 300% larger than New York City or Singapore; President Xi intends this new city to have “a beautiful environment” with high-tech industries and efficient transportation system. The first phase (time will be determined) will cover 100 square kilometers[i].

- Wood inventory in Taicang (along with Wanfang and Meijing) port increased dramatically (67%) from 736,000 m3 (January 2017) to 1,230,000 m3 (February 2017) (see the last chart below). Volume in March dropped slightly but is still 1,153,000 m3 which shows an unexpected trend that is very different compared to the previous year[ii]. Canada Wood will follow-up to uncover the reason behind the trend.

- GDP growth and PMI in 2017Q1 were 6.9% and 51.8% respectively which are better than forecast of most economists.

Caixin PMI decreased from 51.7% in February to 51.2% in March which is the second highest figure during the past 6 months (highest is 51.9% in December 2016)[iii]. After experiencing a dramatic downward turn from USD 182.8 billion in January 2017 to USD 120.1 billion in February, exports value was back to USB 180.6 billion in March 2017 which is higher than the average value during the past 6 months (USD 177.4 billion)[iv].

China Consumer Price Index (CPI) increased from 100.8(February) to 100.9 (March) Index Points which marks the second lowest rate since October 2016 (lowest rate is 100.8 in February 2017 during the past 6 months)[v]. USD/CNY dropped from 6.88 (February 1st) to 6.87 (February 28th) and then increased slightly from 6.88 (March 1st) to 6.89 (March 31st)[vi]; CAD/CNY fluctuated from 5.27 (February 1st) to 5.16 (February 28th) to 5.16(March 1st) to 5.18(March 31st)[vii].

Building material prices

The price for cement in China increased 2.69% from RMB 291.50 per metric ton on March 1st to RMB 299.33 per metric ton on March 31st [viii]; rebar steel was worth RMB 3,688.00 per metric ton on March 1st and then declined 15.50% to RMB 3,584.38 per metric ton on March 31st [ix].

Wood Export to China[x]

[i] Economist (April 6th, 2017). A plan to build a city from scratch that will dwarf New York

[ii] China Bulletin (April, 2017).

[iii] Trading Economics (April, 2017). China Caixin Manufacturing PMI

[iv] Trading Economics (April, 2017). China Exports

[v] Trading Economics (April, 2017). China Consumer Price Index (CPI)

[vi] XE Currency Charts: USD to CNY

[vii] XE Currency Charts: CAD to CNY

[viii] Sunsirs (March 2017). Spot Price for Cement

[ix] Sunsirs (March 2017). Spot Price for Rebar Steel

[x] BOABC (March 2017). China Wood and Its Products Market Monthly Report

May 09, 2017

Source: Fordaq

According to the 2016 China Forestry Development Report, total timber supply (domestic resources and imports) in 2015 rose 2.3% to 552 million cubic meters (RWE).

Of the domestic timber supply, 13% was for commercial processing, 7% farm use and fuel wood, and 27% for fiberboard and particleboard. Timber imports accounted for a further 53% of the total timber supply which include logs, sawn wood, veneer, wood-based panel, wooden furniture, wood pulp, wood chips, paper and paper products, waste paper, as well as other wood products. The Forestry Development Report also says China’s timber consumption rose.

Domestic timber resources are mainly consumed in construction 30%, 1.7% in the coal industry, 29% in paper making, 12% in wooden furniture, 3.5% in the transport sector and 5.5% timber consumption for farmer use and fuel wood with the balance being for other purposes.

Timber exports account for around 18% of timber supply and comprised mainly wooden furniture, wood-based panels, wooden doors, window and flooring, paper and paper products.

China warning Moody’s Investors Service cut its rating on China’s debt to A1 from Aa3, its first reduction for the country since 1989. The agency warned of a “material rise” in economy-wide debt which will place a burden on the state’s finances. MSCI Inc (Modern Index Strategy). Chief Executive Officer Henry Fernandez earlier warned that China still has a lot of issues to resolve before its onshore stocks can get into the company’s emerging markets indexes. The Shanghai Composite Index, which fell as much as 1.3 percent following the downgrade, closed 0.1 percent higher after a late-session rally. Iron ore led a slump in industrial commodities following the announcement.

May 24 17

Beyond the Headlines: Five Things to Watch in China GDP Data

Bloomberg News

July 15, 2017, 8:00 PM MDT July 16, 2017, 10:01 AM MDT

- Support from state-owned enterprises may have subsided

- Slower credit expansion may be drag on economic output growth

With China’s expansion poised to hold steady, a closer look at the data reveals a more nuanced portrait of the world’s second-largest economy.

Gross domestic product expanded 6.8 percent from a year earlier in the second quarter, according to a Bloomberg survey of economists before the report due at 10 a.m. Monday in Beijing (10 p.m. Sunday in New York). Other data are forecast to show industrial production and fixed-asset investment held up while retail sales growth edged down.

With deleveraging being the dominant economic theme this year, the reports will show if and to what extent the curbs are starting to bite. With producer-price reflation slowingand property markets cooling, strong exports and resilient consumption will be key pillars of growth this year.

To better gauge China’s economy, here’s what to watch in the reports:

Borrowing Curbs

Broad money supply as a percentage of total economic output, tracked via a Bloomberg Intelligence index, probably pulled back from a near record high in the second quarter.

The ratio of broad money to GDP also shows whether authorities are making progress in efforts to rein in excessive borrowing. Broad money supply growth was the slowest on record in June, signaling policy makers may be seeing some success.

Slower credit expansion may be a drag on growth though, and a gauge of new lending as a share of GDP, which tends to lead the growth cycle, has gone from sharply rising to gently falling in the past two years, according to Fielding Chen, an economist at Bloomberg Intelligence in Hong Kong. “That casts a shadow on the growth outlook despite recent signs that suggest momentum may have picked up slightly in June,” Chen wrote in a recent note.

Chinese President Xi Jinping said at a two-day National Financial Work Conference ended Saturday the central bank will play a stronger role in defending against risks, calling for more work on safeguarding the financial system and modernizing its regulatory framework. Xi said the financial sector should better serve the real economy, according to state media.

Who’s Investing

Fixed investment is projected to hold up, rising 8.5 percent from a year earlier in the first six months. The breakdown of that growth gives an indication of demand later this year.

The boost from state-owned enterprises may have waned as private spending recovered from a record low last year. Less state dependence signals stronger business confidence.

Property development investment eased in May as sales cooled amid local curbs on buying. That weakness weighs on the expansion by sapping demand for materials like steel, concrete, glass and consumer goods such as home appliances. A sub-gauge of infrastructure spending also has been declining since a peak in the first two months of this year.

Growth Drivers

A supplemental report from the National Bureau of Statistics due for release Tuesday will break down contributions to output by industry. Information technology services, commercial leasing services and transportation were the biggest sources of growth in the first quarter.

The output of services, also known as the tertiary sector, has accounted for more than half of the economy since 2015 and likely remained a key support for the second quarter. Real estate brokerage services probably slowed further on purchasing curbs, while financial intermediation may have remained sluggish.

Consumer Pulse

Consumer spending has supported the economy’s transition away from smokestack sectors. Retail sales probably expanded 10.6 percent in June, according to economist projections.

The sub-gauge of online retail sales may signal more strength in digital commerce, and show consumer demand for specific products such as cars or clothes.

Labor Market

Slower wage gains may weigh on consumption. Disposable income levels included in Monday’s data dump will give a fresh read on the wages of about 280 million migrant workers from rural areas, a low-income group that’s still a big part of the economy.

The NBS may also comment on the labor market, including an update to the survey-based jobless rate, a better barometer than the official registered rate, although it’s not published on a regular schedule. The Ministry of Human Resources and Social Security will release its labor demand and supply ratio on Monday, which signals the overall tightness of the job market.

— With assistance by Xiaoqing Pi

Still on borrowed time Two decades after taking over Hong Kong, China is getting tougher

Will the territory’s new leader, Carrie Lam, stand up to its meddling?

Jun 22nd 2017 | HONG KONG

TWO decades ago a media circus descended on Hong Kong to witness its transfer, after a century and a half as a British colony, to Chinese rule. The handover on July 1st 1997 was an extraordinary, and for many, a poignant moment—not least for the people of Hong Kong, who had created a phenomenal economic success and who were now being placed in the care of a Leninist one-party state.

Britain’s acquisition of the “barren rock” of Hong Kong in 1842 after a brief, unequal war marked the rise not just of a small, aggressive, mercantile, maritime power but the ascent, in general, of the West. Equally, it marked the decline of a once-great civilisation. Hong Kong’s return brought the narrative full circle. For all the pomp, it was clear that Britain was just another so-so power, and China a fast-rising one that might one day eclipse the West. For the government in Beijing it was a moment of triumph: China was back.

On July 1st, in the same convention centre in which the handover ceremony was held, the country’s president, Xi Jinping, will join celebrations to mark the 20th anniversary of the handover—his first visit to the territory as China’s leader. He will preside over the swearing-in of Carrie Lam (pictured) as Hong Kong’s chief executive in place of “C.Y.” Leung Chun-ying. Mrs Lam, who previously served as head of the civil service, will be the first woman to lead the territory.

Mr Xi is certain to praise the success of “one country, two systems”, the formula China prescribed for Hong Kong. But he will be uneasy. Many people in Hong Kong are bitterly frustrated by their lack of say in how they are governed. And the growth of a “localist” movement in Hong Kong over the past five years, demanding self-determination or even independence, has greatly angered a Communist Party for which absolute sovereignty—ie, the regime’s security—is the bottom line.

Carrie Lam faces tough times ahead

Two systems, converging

China’s formula was intended to reassure Hong Kong that it could keep its capitalist economy, its independent courts and its politically liberal (if undemocratic) culture. Yet it will be lost on no one that Mrs. Lam, like her predecessors, was chosen not by ordinary Hong Kong people but by 777 votes in a nominating process tightly controlled by the party. A striking feature of Mr Leung’s five years in office has been the growing sway and visibility of the central government’s organ in Hong Kong. Known as the Liaison Office, it was once low-key. Some now divine a parallel government operating in the territory.

Just as they will be on July 1st, the people of Hong Kong were mere extras 20 years ago. They had not been consulted about the terms of the handover, including the drafting of the territory’s new mini-constitution, the Basic Law, which promised a “high degree of autonomy” and a way of life that would remain unchanged for 50 years. A lack of confidence in Hong Kong’s future had prompted a rush to obtain full British or other Western passports and to find bolt holes abroad.

Yet as the handover date approached, a generally positive mood prevailed among ordinary citizens. Opinion polling by Hong Kong University showed twice as many people satisfied with their lives as not. After all, China’s economy was beginning to take off. Indeed the whole region was booming. Hong Kong seemed extraordinarily well-placed to benefit. Early impressions of Chinese rule reinforced optimism. When the People’s Liberation Army crossed the border into Hong Kong, they disappeared into barracks. The goose stepping was confined largely to the convention centre (most people have yet to see a Chinese soldier on the streets).

Hong Kong remains distinct—not only the most prosperous part of China but also the freest. Hong Kong’s courts are still respected globally for their professionalism and unbiased rulings. The press still airs vigorous criticism of the local government and of China’s leaders. Political debate is vibrant and protest is permitted, including by organizations such as Falun Gong that are banned on the mainland. Hong Kong’s way of doing business has not noticeably eroded, despite an influx of Chinese “red-chip” companies raising capital in Hong Kong (its stock exchange is vying to attract them, see article).

But since the handover, and especially in the past five years, anxieties have grown. They have been fueled by subtle changes in Hong Kong’s political culture (“mainlandisation”, as some describe it) and intrusions by the Chinese state. In 2015 Chinese secret police abducted a bookseller to the mainland; earlier this year they did the same to a Chinese tycoon.

Democrats complain about ever-more-blatant attempts by China to manipulate elections, journalists about self-censorship in the media and university staff about politically driven appointments. Lawyers fear an erosion of judicial independence caused by China’s efforts to make sure that the Basic Law is interpreted to suit the party’s political needs. Its latest constitutional pronouncement, in November, aimed to prevent two localist legislators from taking up their posts on the ground that they had deliberately garbled their oaths when they were sworn in. A court in Hong Kong was already considering the legality of their oaths; China wanted to stop it reaching the wrong decision.

Dashed hopes

At the time of the handover, The Economist expressed hope that Hong Kong would serve as a laboratory for political change on the mainland. “What if”, we asked, “Hong Kong takes over China?” Instead, over the past two decades, and especially under Mr Xi, the party has shut down dissent on the mainland. Politics there has grown only more illiberal. Protecting Hong Kong from this trend will require considerably greater vigilance by its government and people. The greatest risk, as one former senior official says, is that political and business elites in Hong Kong, rather than strongly making the case for Hong Kong’s autonomy, fawningly cede it to the Liaison Office, or to the party in Beijing.

In the past it was easier to argue that China risked damaging itself by interfering in Hong Kong. At the time of the handover, the colony, with a population of 6.5m (now 7.3m), had an economy equivalent to a fifth of that of the mainland, with its population of over 1bn. This may partly explain why, for the first few years after the handover, China let Hong Kong’s government rule much as it wished, as long as it did not challenge the mainland politically. Anson Chan, who represented continuity as civil-service chief under both the last British governor, Chris Patten, and the first chief executive, Tung Chee-hwa, says that not once in four years did she have contact with the Liaison Office as part of her work.

But China no longer feels so beholden to Hong Kong for its economic welfare. The territory’s GDP is now less than 3% of the faster-growing mainland. And as China’s economy rapidly becomes more integrated with the rest of the world, Hong Kong’s no longer looks so special to officials in Beijing. In his book, “A System Apart”, Simon Cartledge (formerly of the Economist Intelligence Unit, a sister firm of this newspaper) argues that Hong Kong’s economy is “stuck, with remarkably little change to show for the last two decades”. Trade and logistics, which are exemplified by Hong Kong’s container port, make up nearly a quarter of GDP, little different from the mid-2000s. Finance accounts for 17%—little changed either.

China, however, has changed a lot. In many ways it is now a rival. Ports in the city of Shenzhen just across the border now do more business than Hong Kong. And Hong Kong’s role as a financial hub is no longer as important to China as it once was. The bourses in Shanghai and Shenzhen do far more trade and are strengthening their links with global markets (see article).

The rise of an economically powerful China—one less bashful about asserting its authority in Hong Kong—has coincided with growing gloom in the territory about its own economy. When measured by GDP per head, Hong Kong’s performance over the past two decades has been respectable. It is worse than other Asian tigers (and Ireland, the Celtic tiger), but better than almost everyone else. Yet its boom days are over. In the 1970s Hong Kong’s annual GDP growth averaged 9%; in the 1980s, 7.4%. But from 1998 to 2016 it averaged just 3.3%. And during Mr. Leung’s tenure, the figure was 2.3% (for annual rates, see chart). Even the one notable growth area, tourism, contributes mainly low-paying jobs and a huge influx of mainlanders whom many Hong Kongers resent. They call them “locusts” for the frenetic way they shop.

A slowdown is inevitable as any fast-growing economy matures. Yet many people are disgruntled. Inequality is rising, soaring property prices make it hard to afford a flat (nearly half of Hong Kongers live in public housing), and general satisfaction is sharply lower than it was a decade ago.

The economy has long been dominated by the same conglomerates and increasingly elderly tycoons. Property development is the most conspicuous example. A few giants are allowed a lock on a lucrative market because property is the government’s chief source of taxation. But other industries, often related to the developers, also operate as monopolies, duopolies or cartels. They include supermarkets, power, ports and aviation. From nothing, Shenzhen has given birth to such tech giants as Tencent, Huawei and ZTE; entrepreneurs in Silicon Valley salivate over the Chinese city’s prospects. Hong Kong has no such energy. Preserving wealth trumps creating it. A seventh of Hong Kongers are poor. On the streets at night old women collect cardboard to make ends meet.

With pinched prospects and inequality on the rise, it is hardly surprising that many feel the government is out of touch. There was an underappreciated economic dimension to the dissatisfaction expressed in the “Umbrella” protests in favour of free elections that blocked several major roads for more than 11 weeks in 2014. Similar sentiment was evident in elections for the Legislative Council (Legco) in September, in which localists secured a fifth of the popular vote, as well as in the underwhelming public reception of Mrs Lam’s elevation.

In Beijing, Hong Kong’s political mood is interpreted as rank ingratitude at best, treason at worst. Both the central government and Hong Kong’s pro-Beijing elites long to turn Hong Kong back to what they like to call an “economic” city, putting politics back in the bottle. That is wholly to miss the point. China’s efforts to keep Hong Kong’s economy running as it did in colonial days have compounded the local government’s political problems today.

Under the British, the government was pro-business but not of business. Since 1997 business interests have been baked into the political system (Mr Tung, the first chief executive, was a shipping magnate). Conflicts of interest have multiplied. Cronyism has grown. To date, the tenures of all chief executives have ended in ignominy or failure. The government has been reluctant to foster change. It could have tried to broaden the tax base so as to reduce its dependence on property. To broaden its appeal, it could have sought to let political parties be represented in government. It has done neither.

In office, Mrs Lam will struggle to break with this legacy. Though a hard-working bureaucrat, her cosy relations with the central government undermine her credibility locally. She is prone to curious gaffes, such as admitting she did not know where to buy lavatory paper. Above all, she is struggling to bring together a competent administration. As a gulf of legitimacy grows between the government and the governed, able people from outside the bureaucracy are less willing to take cabinet positions. Mrs Lam can always recruit members of the civil service into political posts, but that drains a respected service of competent and experienced administrators.

Shadowy government

One unwelcome consequence of the mess is that the baneful presence of the Liaison Office is even more likely to grow. As it is, the central government’s outpost has abandoned any pretense at remaining low key. It provides loans to businesses. It has bought up Hong Kong’s largest publishing house and book-chain owner. (Titles critical of the party have, of course, been removed.) It openly lobbied for Mrs Lam to be endorsed by Hong Kong’s tame election committee. Some analysts believe it influenced her decision to choose Hong Kong’s immigration chief—whose relations in that capacity with mainland authorities had been central to his work—as her future chief secretary, despite his lack of administrative experience.

One of these characters wields great power

The office’s representatives get pride of place at civic functions. And it backs candidates sympathetic to the Communist Party in elections to district councils and LegCo. Last year the office’s chief, Zhang Xiaoming, allowed his calligraphy extolling moral strength to be auctioned to raise funds for the main pro-Beijing party, the DAB (he is pictured above at the event, wearing a blue tie). A businessman with mainland interests bid HK$18.8m ($2.4m) for the art. “And it was really bad calligraphy,” says a former official. Many in the democratic camp see the creeping arm of the Liaison Office, Hong Kong’s “second team”, as a breach of China’s promises to Hong Kong—and a possible conduit for mainland-style corruption.

For those Hong Kongers with the territory’s interests at heart, the past 20 years offer some lessons. One is that for all the Communist Party’s might, and a want of democratic representation, popular opinion—strongly expressed—counts for something. Mr Tung’s attempt to pass an anti-subversion law demanded by the central government led to huge protests in 2003, the bill’s shelving, and Mr Tung’s eventual resignation. Protests in 2012 stopped a move to foist on schools a programme of Communist-inspired patriotic education. And even though Mr Leung patiently wore down the Umbrella protests by refusing to make concessions, his actions fostered a younger generation of political activists, many of them teenagers. That generation identifies far less with the mainland than do those who witnessed the handover.

Localism may help to preserve some of what makes Hong Kong distinct, but its rise is creating fractures in the pro-democracy camp. Under pressure from localist radicals, moderates are finding it more difficult to compromise with the government. Hence their rejection of a political-reform package in 2014 that would have allowed universal suffrage in choosing the chief executive, but with only vetted candidates running. Localism has also encouraged hardliners in Beijing to treat the territory as a potential political threat. Mrs Lam will take over an administration that feels overwhelmed by such conflicting pressures. Once a gung-ho place, Hong Kong these days struggles even to put in place sensible rubbish-recycling policies or push forward oft-stalled plans for a world-class cultural district. The quotidian falls victim to broader ideological struggles.

For all the current protest-fatigue, those struggles are bound to continue. Under British rule, Hong Kong was often referred to as a borrowed place on borrowed time (a description inspired by the title of a classic book about the territory by Richard Hughes). Time still haunts it. Nathan Law, an advocate of self-determination who at 23 is LegCo’s youngest member, points out that 20 years since the handover is also just 30 years until July 1st 2047, when all formal promises about Hong Kong’s autonomy are void. In May last year, protesters displayed a countdown in seconds to that date on Hong Kong’s tallest skyscraper; see picture. To Mr Law’s generation, he says, 2047 is not far away; he will still be in his prime. It is why, he argues, there is all to play for now.

Counting down to the next big date

The Communist Party and its Hong Kong backers are clear about how to play the game: restrain democracy and try to exclude from elections any candidate they deem to be sympathetic to independence. Chinese officials have been making it clear to Mrs Lam that they want the shelved anti-subversion bill to be revived; as they see it, such a law would be a useful weapon against separatists.

A better approach

So Hong Kong needs a new form of politics that involves playing a long game cannily. Mrs Lam does not seem the kind of person to argue doggedly in defence of Hong Kong’s rule of law, its way of life or its right to have free elections. But both she and her critics must find the confidence to seek new ways of co-operating with China economically. That will stick in the craw of people keen to safeguard Hong Kong’s distinctiveness. Yet dogged opposition to everything China does will make the party all the more inclined to tighten control. Let the game begin.

This article appeared in the China section of the print edition under the headline “Still on borrowed

Banyan Will China fill the vacuum left by America?

Not as long as Chinese officials remain shy of the world stage

Jun 8th 2017

EVEN analysts who make a living predicting a great shift of wealth, power and global leadership from the United States to China never anticipated the speed with which Donald Trump appears to be marginalizing his homeland. Last week Mr. Trump announced he would pull America out of the Paris accord on climate change. At an annual China-EU summit under way at the time, the president of the European Council, Donald Tusk, declared that China and Europe together would demonstrate “solidarity with future generations and responsibility for the whole planet”. Others have gone further: it will be to China that the world will now turn for leadership on the issues that matter.

China appears to have advanced on other fronts. The Shangri-La Dialogue in Singapore, an annual talkfest on security, exists in part to showcase America’s commitment to keeping the peace in Asia. Mr. Trump’s defense secretary, James Mattis, did his best at this year’s event over the weekend to reassure Asian friends. Their chief concern is over the South China Sea, which China appears bent on turning into its own lake.

But though Mr. Mattis’s promises to expand American engagement in Asia were welcome, they did not dispel the perception that America is taken up with North Korea’s nuclear threat (see Lexington), at the expense of the rest of the region. And America is run not by Mr. Mattis but by an erratic man for whom “America First” may imply wrecking the world order that America itself built out of the ruins of the second world war. Amid doubts about America’s commitment to the region, South-East Asian officials proposed that their countries’ navies join China’s to patrol the South China Sea, in which China has greatly expanded its presence through the construction and military reinforcement of artificial islands. It smacked, to some, of rolling over in the face of Chinese power.

Elsewhere, Chinese leadership seems to move from strength to strength. As The Economist went to press, China’s own security grouping, the Shanghai Co-operation Organization (SCO), which includes Russia and four Central Asian states, was preparing to welcome India and Pakistan as new members. Pakistan, an old ally of China’s, is a natural inclusion. But India is a rival, so its nod to Chinese might is notable. The SCO’s expansion reinforces China’s ambitions for its “belt and road” initiative of infrastructure spending that is intended to tie Asia to Europe, the Middle East and even Africa. Those who worry about Chinese power see the initiative as a gilded instrument of a new Chinese order.

This seeming tilt towards China owes little to its powers of attraction. It is more of a knee-jerk response to events in Washington: if that’s what you do, Mr. Trump, say those who have prospered under an American-led order, it leaves us with no choice but to turn elsewhere. But admire China’s sense of timing. In January, even before Mr. Trump’s inauguration, China’s president, Xi Jinping, speaking before the world’s elites in Davos, presented his country as a champion of globalism and open markets.

And yet: where China appears to be filling a leadership vacuum, there is often less than meets the eye. Climate change is one example. The world’s largest emitter has done much to cut back on its discharge of greenhouse gases, installing more renewable capacity than any other country. Yet its own transparency and accountability over pollution and emissions still falls far short of the openness a world leader on climate change would need to adopt. Meanwhile, common cause between Europe and China has severe limits. As James Kynge of the Financial Times says, China’s push to cut emissions is motivated by an environmental crisis at home, combined with hopes of conquering world markets for renewable energy. Europe wants to save the planet.

As for economic leadership, the EU-China relationship again reveals the limits. Mr. Xi prizes open markets, but many of China’s own remain closed—and where foreigners may operate, the fear is of technology being stolen. That has led to European frustrations. Anger is growing over China’s divide-and-rule tactics in separately wooing 16 poorer central and eastern European countries, using belt-and-road enticements.

With the addition of India and Pakistan, the share of the world’s population who are citizens of SCO members will balloon to nearly half: Chinese officials proudly point out that the group will embrace three-fifths of the Eurasian land mass. But managing the newcomers’ bickering could absorb China’s energies, reducing the forum to little more than a talking shop about terrorism and trade. As for the South China Sea, China has been strangely quiescent since an international tribunal a year ago lambasted its territorial claims in the sea. It has been at pains to get on with neighbors it has disputes with, especially the Philippines and Vietnam.

No such thing as a small matter

Since at least the days of Napoleon, the world has been gasping at the scale of China’s potential. China certainly knows how to play to that imagining. And the propaganda directed at its own people emphasizes a return to historical importance every second of the day. Yet China is reluctant to push really hard on the outer boundaries of what it might hope to do. Just as it is browbeating neighbors over the South China Sea less than some had predicted, so, for all that it relishes being referred to as a leader in climate change, it is far from keen to take on a leader’s responsibilities. And at Shangri-La, China didn’t even send any senior leaders, merely what Washington wonks call “barbarian handlers”: lower-level functionaries whose job is merely to parrot their government’s line. Being a world leader involves being able to handle criticism on an international stage. China remains very unwilling to risk that. And the reason is simple: fear of how any slip-up might play at home. Waishi wu xiaoshi, goes the saying: there is no such thing as a small matter in external affairs.

This article appeared in the China section of the print edition under the headline “Still shy of the world stage”

Herding mentalityInner Mongolia has become China’s model of assimilation

But Chinese Mongolians are still asserting their identity

Jun 1st 2017 | HOHHOT AND WEST UJIMQIN

BAYIN was three when he moved from the eastern grasslands of Inner Mongolia to Chifeng, a city of some 1 million people. Like hundreds of thousands of ethnic Mongolian pastoralists forced to settle by the government, his family has gone from rural yurt to urban block of flats within a generation. Bayin, who is 32, moves seamlessly between staccato Mongolian and tonal Mandarin. In many ways he exemplifies the successful assimilation of China’s 6 million ethnic Mongolians, most of them in Inner Mongolia in China’s north.

Yet Bayin lives largely within a Mongolian world. He designs Mongolian robes for a living and wore them to get married in 2012; of his 300 or so wedding guests only a handful were Han, the ethnic group that makes up more than 90% of China’s population. His daughter attends a Mongolian-language kindergarten. He likes to watch videos of Mongolian life in the 1950s.

The Chinese government has long struggled to bring the country’s borderlands under control. It took a decade for the Communist Party to subdue Yunnan in the southwest and Tibet after it came to power in 1949. In Tibet and in the far western province of Xinjiang ethnic tensions still sometimes flare into violence; both have separatist movements that have been brutally suppressed. Ethnic relations have not always been easy in Inner Mongolia either: Mongolians frequently clashed with the authorities until the early 1990s.

In recent decades, however, the province has been largely quiescent. It does not have a separatist movement—a surprise given that Mongolia, an independent, democratic country populated by 3m people of the same ethnicity, lies just to the north. Local gripes are more often expressed in economic terms than in ethnic ones. It helps that many ethnic Mongolians are visually indistinguishable from Han Chinese, says Enze Han of the School of Oriental and African Studies in London. They are far more likely to marry a Han than minorities in western China. Many more youths leave the province to find work elsewhere too. Small wonder that the Communist Party is trying to replicate at high speed in Tibet and Xinjiang policies that have helped it subdue Inner Mongolia over many decades.

Damned if you Xanadu

Inner Mongolia’s integration is partly historical. Kublai Khan, grandson of Genghis Khan, founded a dynasty in 1271 that bound it to China. Geographical proximity to Beijing meant exchanges were frequent. Tribal divisions and the dispersal of the population hampered resistance to Chinese authority. Inner Mongolia constitutes 12% of China’s territory, but hosts less than 2% of its population.

Government policies suppressed Mongol identity. Han migration started in the 19th century. The native population was already in the minority by 1949; now only 20% of people in the province are Mongolian. The region suffered especially severe violence in the Cultural Revolution—up to 100,000 people died, by some reckonings. Buddhism, which was strongly rooted in Inner Mongolia, was crushed, and most temples destroyed. At the sprawling monastery of Da Zhao in the provincial capital of Hohhot, tourists now outnumber devotees (nevertheless, in case of problems, a SWAT team waits around the corner).

Teaching local children in Mandarin, a policy which the party is now pursuing with gusto in Tibet and Xinjiang, started early in Inner Mongolia too. All young Mongolians speak Mandarin—far fewer understand Mongolian. So comfortable is the party with the dominance of Mandarin that it has allowed Mongolian-language education to grow: the share of primary and middle-school pupils taught in Mongolian actually increased from 10% in 2005 to 13% in 2015.

Money has helped ethnic Mongolians come to terms with the Chinese Communist Party: GDP per person is $10,000 a year in Inner Mongolia, compared with $4,000 in Mongolia the country. Such riches are the result of a deliberate government strategy to exploit minerals, particularly coal, and build infrastructure (another measure repeated recently in western China).

The question is whether the model of assimilation and appeasement is sustainable. Economic pressures are growing. Many Mongolians feel excluded from the province’s overall prosperity. City folk, who are disproportionately Han, earn twice as much as herders. Even in rural areas, the energy-intensive and heavily polluting industries that fuelled the region’s boom largely benefit Han companies; few miners are Mongolian.

Mining companies show scant regard for grass or goats and consume lots of water. The water table has dropped by 100 metres in some places, according to Greenpeace, an NGO. New mines were curtailed in 2011, when a Han driver deliberately ran over and killed a Mongolian herder, sparking protests. The provincial government also soothed pastoralists with subsidies.

But Tsetseg, a 36-year-old herder near West Ujimqin, close to the scene of the killing, says most subsidies now exist in name only. Desertification and climate change mean there is less grass for her goats to graze on, so she increasingly has to buy corn as well. With rising feed costs and falling meat prices, her family has little hope of ever repaying the 100,000 yuan ($15,000) they owe. Tsetseg’s economic woes sometimes assume ethnic overtones. The area was awash with Han police after the protests in 2011, she says. She “would not agree” to her son marrying a Han: “There aren’t many Mongols now. When they marry a Han we lose them: we have to keep our bloodline.”