I thought these were amusing predictions from the Toronto Sun for 2017. Somewhat relevant with the current cast of leaders. Let us hope that the red rooster’s impulsive and hasty nature does not “trump” strategic and measured responses. Another fun and exciting year in our global neighborhood!

The Chinese New Year is coming up January 28, and this year is the Year of the Rooster. Every year, world-renown astrology Eugenia Last presents a special horoscope celebrating this auspicious occasion.

United States Outlook

The United States will need to practice control, striving to obtain the perfect balance between diplomacy and strong-arming any opponents that might want to challenge or take privileges without asking. It will be of utmost importance that strategy supersedes the temptation to act in haste and without the general consensus of superpowers around the world.

Showing excellence and integrity along with compassion and logic will be required during many muddled moments that could result in hasty reactions based on assumptions instead of facts.

A steady hand and willingness to work in unison with the majority will mark the outcome of a year riddled with posturing. It will take strong, savvy leadership to navigate through the challenges that face the world physically and financially.

Canada Outlook

Canada will strengthen its relationships within the global network of countries fighting for freedom and peace on earth. The contributions made by this nation will set an example on the world platform that will inspire others to follow suit.

The 2017 Fire Rooster year will radiate authority and precision in order to bring about control, however not without plenty of drama to assure his presence is felt on a world level. This is a year where pressure and persuasion will be applied to vie for power, making it necessary to join forces with those who share the same values and environment concerns.

United Kingdom Outlook

The United Kingdom will face its own challenges, but a steady pace to strengthen and bring about positive change is apparent. However, it could still be subjected to homeland security issues, leaving room to be threatened by outside sources trying to undermine this great nation’s intelligence and courage to stand tall and remain united with its allies.

It will be time for the British to use past experience and intelligence to contribute to and bring about a worldwide plea for universal solidarity.

Schumpeter

The three Rs behind global banks’ recovery

Soaring share prices suggest the end of the tunnel for big banks

Jan 7th 2017

IN THE Bible, seven years of feast were followed by seven years of famine. For banks there have been ten lean years. Subprime-loan defaults started to rise in February 2007, causing a near-collapse of the industry in America and Europe. Next came bail-outs from governments, then years of groveling before regulators, mass firings of staff and quarter after quarter of poor results that left banks’ shareholders disappointed. Now, a decade later, the moneylenders are quietly wondering if 2017 is the year in which their industry turns a corner.

Over the past six months the FTSE index of global bank shares has leapt by 24%. American banks have led the way, with the value of Bank of America rising by 67%, and that of JPMorgan Chase by 39%. In Europe BNP Paribas’ market value has risen by 52%. In Japan shares in the lumbering Mitsubishi UFJ Financial Group—the rich world’s biggest bank by assets—have behaved like those of a frisky internet startup; they are up by 57%. Predictions about global banks’ future returns on equity have stopped falling, note analysts at UBS, a Swiss bank. Some of the biggest casualties of the financial crisis are even expanding. On December 20th Lloyds, bailed out by British taxpayers in 2009 at a cost of $33bn, said it would buy MBNA, a credit-card firm, for $2bn.

The excitement can be explained by three Rs: rates, regulation and returns. Consider interest rates first. The slump in rates has been terrible for banks. Between 2010 and 2015, the net interest income of the rich world’s 100 biggest banks fell by $100bn, or about half of 2010 profits. When rates across the economy rise, by contrast, banks can expand margins by charging borrowers more, while passing on only some of the benefit of higher rates to depositors. So bankers have been watching the bond market with barely concealed joy. Ten-year government yields have risen by one percentage point in America, and by 0.30-0.64 points in the big euro-zone economies and Japan over the last six months. Investors are talking about a Trump-inspired “reflation”: the president-elect promises to embark on a public-spending boom. In Germany inflation is at a three-year high of 1.7%.

| 3 |

Banks’ CEOs are also chipper because they think that regulation has peaked. In America the new administration is likely either to repeal the Dodd-Frank act, an 848-page law from 2010, or to prod regulators to enforce it less zealously. Bank-bashing fatigue seems to have set in among the public. True, when firms misbehave, there is still a firestorm of outrage. John Stumpf, the boss of Wells Fargo, quit in October after his bank admitted creating fake accounts. But many people can see that power has migrated from banking to the technology elite in California. The brew of high pay, monopolistic tendencies and huge profits that attracts populist resentment is now more to be found in Silicon Valley than in Wall Street or the City of London.

Global supervisors are still cooking up new rules, known as “Basel 4” (see article), but are unlikely to demand a big rise in the safety buffer the industry holds in the form of capital. The strongest banks are signaling that they will lay out more in dividends and buy-backs, rather than hoard even more capital (today, the top 100 rich-world banks pay out about 40% of their profits).

A third reason for optimism in bank boardrooms is returns. Global banking’s return on equity (ROE) has crept back towards a respectable 10%. The worst of the fines imposed by American regulators are over. So far, “fintech” startups that use technology to compete with rich-world banks have not won much market share; banks have used technology to boost efficiency. They have also got better at working out which of their activities create value after adjusting for risk and the capital they tie up. Barclays, once known for cutting corners, says it can calculate the ROE generated by each of its trading clients. It is ditching 7,000 of them.

Given the giddy mood, the big danger starts with a C, for complacency. Regulators believe that banks now pose less of a threat to taxpayers. American lenders have $1.2trn of core capital, more than twice what they held in 2007. Citigroup, the most systemically important bank to be bailed out, now has three times more capital than its cumulative losses in 2008-10. European banks’ capital buffers have risen by 50% since 2007, to $1.5trn.

Yet there are still plenty of weak firms that could cause mayhem. Deutsche Bank, several Italian lenders and America’s two state-run mortgage monsters, Fannie Mae and Freddie Mac, are examples. Mega-banks may simply be too big for any mortal to control. For every dollar of assets that General Electric’s Jeff Immelt manages, Jamie Dimon at JPMorgan Chase looks after $5.

Once bitten

And banks still lack a post-crisis plan beyond cost-cutting. Despite their surging shares, most are valued at around the level they would fetch if their assets were liquidated, which hardly indicates optimism about their prospects. Before the crisis, they inflated their profits by expanding in unhealthy ways. They captured rents from state guarantees, created ever more layers of debt relative to GDP, and grew their balance-sheets by means of heavy over-borrowing. They have reversed much of this expansion over the past decade but that strategy cannot go on forever.

In 2017 banks will need to articulate a new growth mission and show that they can expand profits without prompting public outrage or a regulatory backlash. One area of promise is the drive to raise rich-world productivity. That would boost economies broadly, and their own profits. There is plenty that banks could do: get more credit to young firms, improve payments systems so that a higher proportion of midsized firms can engage in cross-border e-commerce, and harness technology to make banking as cheap and easy to use as a smartphone app. Forward-thinking bank bosses are already emphasizing such goals. If they could achieve them over the next decade, they might even realize a fourth R—redemption.

Global corruption in forestry sector worth USD 29 billion a year, says Interpol

A recently released Interpol report underlines the scale of criminal activity tied to the forestry sector and the importance of coordinating anti-corruption efforts to protect forests.

Among its key findings, the report entitled Uncovering the Risks of Corruption in the Forestry Sector estimates that the annual global cost of corruption in the forestry sector is worth some USD 29 billion.

It also found that bribery is reported as the most common form of corruption in the forestry sector. Other forms of corruption include fraud, abuse of office, extortion, cronyism and nepotism.

The report says that criminal networks use corruption and bribe officials to establish ‘safe passage’ for the illegal movement of timber. Criminal groups also exploit these routes to transport other illicit goods such as drugs and firearms.

It includes an example from Peru where the mayor of an important timber trading city was arrested for his involvement in drug trafficking through plywood shipments. The mayor controlled a timber business that had been used to strategically build a logistical network for bribing officials to move illegally harvested timber out of the country.

Using this network, the mayor and other drug traffickers were able to move cocaine hidden in plywood shipments. Upon arrest, police seized assets worth USD 71 million which could not be accounted for.

“By raising awareness and documenting current corruption practices as well as potential solutions, we empower law enforcement officers in the field. This increases the chances of criminals getting caught and is one of the greatest deterrents to corruption,” said Interpol Secretary General Jürgen Stock.

“An international, coordinated response is an essential part of the solution to combat the organized transnational criminal groups involved in forestry crime. Our collective goal must be to turn corruption into a high risk, low profit activity,” added the Head of Interpol.

To this end the key measures that the report recommends include capacity building across the entire law enforcement chain, enhanced financial investigation techniques, and adoption of Interpol’s I-24/7 global secure communications network for anti-corruption investigators.

In 2012, Interpol launched Project Leaf to counter various aspects of forestry crime, including illegal logging and timber trafficking, and related crimes such as corruption.

Under the Project, Interpol can issue international notices and alerts on behalf of member countries to request information on, and warn of, the movements and activities of people, vehicles and vessels.

It can also organize national and regional training sessions relevant to forestry crime, including evidence collection, chain-of-custody and operational planning.

Funded by the Norwegian Agency for Development, Project Leaf works in collaboration with UN Environment to help shape a global response to forestry crime.

FORDAQ january

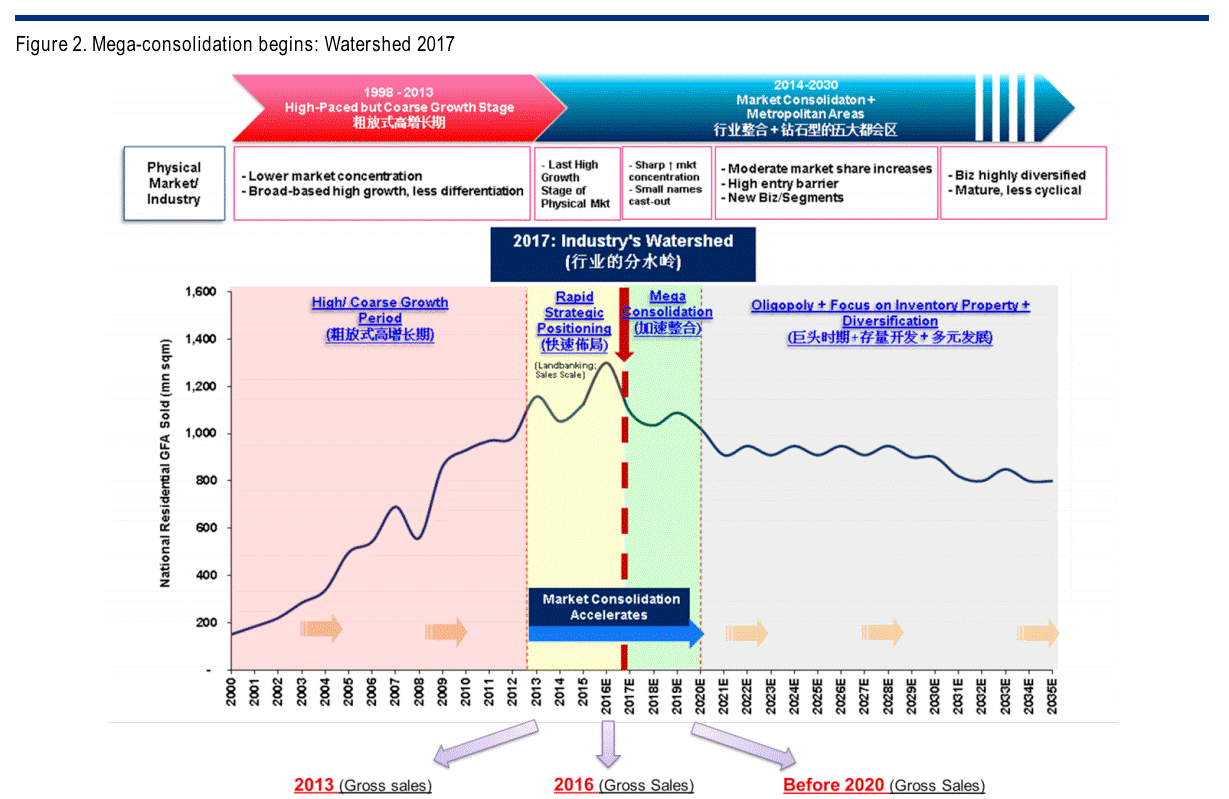

China’s coming property oligopoly, charted

The thesis is simple. More market share based on the need for more market share: “Leaders’ near-term priority for market share will force out small players, raising entry barriers (given difficulties to replenish land) and sowing the seeds for an oligopoly market (巨头垄断) – securing mid-long term earnings visibility. By 20E, the top-10 players’ shares should rise to 35% (top-20: 45%), and they can start diversification with distinctive edges (e.g., huge clientele).”

And do note that we are apparently through the high-paced but coarse growth stage for this market, as per the following charts, the second of which includes actual names for those feeling brave:

Not pictured: Continuously perilous bubble-like conditions and the related overriding presence of the state in the market. Over the past half year that presence has been aimed at cooling the overheating market, particularly in Tier1 and Tier2 cities, and it’s important to remember that the government can very easily increase the supply of land if it wants to:

To be fair to China property bulls though, China’s developers are not new to the cycles of the property market and the assumption is always that the government is keen to defend land and property value since so much of the highly-leveraged economic edifice is built upon it. Land (and construction) has an outsized role in GDP growth and is used as collateral in local government, individual and corporate borrowing — the local government bit being extremely important during the fiscal expansion of the past few years.

As Citi say, with our emphasis:

According to the China National Audit Office (NAO), China’s local governments are estimated to have total debts of RMB17.4 trillion, of which RMB11.3 trillion (c. 65%) are bank borrowings that have land pledged as collateral. Besides, according to MLR’s report (2015 中国国土资源 公报), for the 84 key cities, the land areas that have been collateralized have been continuously increasing. By the end of 2015, a total 490,800 hectares had been pledged for total loans of RMB11.30 trillion, up 8.8% and 19.1% yoy, respectively…

Fiscal revenues (mainly tax-related revenues such as business taxes, propertyrelated taxes, etc) and government fund income (dominated by revenues from land sales) are the key sources of direct income for local governments. They also enjoy tax returns/transfers from the central government to subsidize investments and expenditures. According to our analysis, property-related tax revenues and land sales proceeds jointly account for 42% of local governments’ direct income (fiscal revenues + local government funds). The property market, in short, has become the critical income source for local governments. This is the key reason why we believe a property market collapse could be ill afforded by central/local governments, though they do hope for a cooling of the property market.

Also:

.. 2017 is a “politically” important year for China given the 19th National Congress of the Communist Party of China (中国共产党第十九次全国代表大会) will be hosted in 2H (around Nov). Before this meeting, “stability” will be the watchword, in our view, making it unlikely that there will be significant reform of the land system.

We look forward to it all continuing in a linear, forecast able manner.

Top of Form

Add to myFT

Bottom of Form

Wave of spending tightens China’s grip on renewable energy

Beijing’s global role in green power contrasts with Trump rhetoric on retrenchment

© Reuters

Bottom of Form

January 5, 2017

by: Andrew Ward, Energy Editor

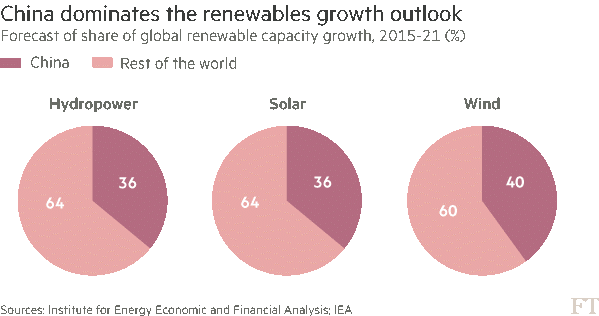

China is strengthening its dominance of the global renewable energy industry after increasing investments in green technology overseas to more than $32bn — far in excess of the amounts deployed by any other country.

The 60 per cent surge in Chinese capital last year highlights the country’s increasing economic commitment to low-carbon forms of energy even as Donald Trump, the US president-elect, threatens to weaken Washington’s backing for the shift away from fossil fuels.

China is already investing more than $100bn a year in domestic renewable energy projects — more than double the US figure — and the latest data show that Chinese money also dwarfs US green finance globally.

“As the US owned the advent of the oil age, so China is shaping up to be unrivaled in clean power leadership today,” said Tim Buckley, director of energy finance studies for the Institute for Energy Economics and Financial Analysis, a US-based think-tank.

Chinese companies made 11 outbound investments in excess of $1bn in 2016, adding up to a combined $32bn, compared with eight deals for a combined $20bn in 2015, according to research by IEEFA.

These ranged from an offshore wind farm in Germany and a solar power project in Egypt, to an Indonesian hydropower plant and lithium production for electric vehicle batteries in Chile.

Four of the five biggest renewable energy deals worldwide in 2016 were made by Chinese companies, according to Mr Buckley, and he predicted this trend would continue irrespective of any change in approach by the US.

“Whether it’s for energy security, or the need to improve air quality, or the need to create jobs and find outlets for capital; by any of these logics China is totally committed to renewable energy,” said Mr Buckley. “Until recently it was a domestic story but in the past year or two China has started to invest globally.”

By far the biggest of the deals struck in 2016 was the acquisition of a controlling stake in CPFL Energia, one of Brazil’s biggest generators and distributors of renewable power, by State Grid Corporation of China as part of a proposed takeover expected to total $13bn once completed.

Mr Trump, who once tweeted that climate change was a Chinese hoax to undermine US competitiveness, promised before his election to withdraw the US from the Paris climate accord and sweep aside many of the commitments to cut fossil fuel emissions that the US had pledged as part of the agreement. However, he has since said he has an “open mind” on the issue.

Sam Geall, a specialist on low-carbon technology in China at the University of Sussex, said Chinese capital had become a more important driving force behind the expansion in renewable energy capacity around the world than US policy.

The 2015 UN climate agreement in Paris was only possible, he said, because of the rapidly declining cost of replacing fossil fuels with renewable energy — a trend he attributed in large part to Chinese investment. Five of the world’s top six solar panel manufacturers are Chinese, as are five of the top 10 wind turbine manufacturers.

“That was the result of smart long-term industrial policy in China and the Trump presidency will not change that,” said Mr Geall. “What it may mean is that, if the US does not support its own renewable industry, it will lose out to China.”

China invested $103bn in domestic renewable energy in 2015, according to Bloomberg New Energy Finance, compared with $44bn by the US. China’s National Energy Administration this week committed to further increases in years ahead with a plan for Rmb2.5tn ($363bn) of domestic investment in clean energy by 2020.

China eyes biomass energy as to replace coal

China plans to expand the upgrade of biomass energy in the next 5 years as to reduce coal consumption and improve the air quality.

The National Energy Administration announced on the 5th of December that the country aims to achieve the target of using biomass energy equivalent of 580 million of tons of coal yearly by 2020, as reported by China Daily.

As the administration’s 2016-2020 biomass energy development plan shows, the biomass energy use will be more commercialized and industrialized by 2020. At the moment, China produces biomass energy that is similar to approximately 460 million tons of coal annually. The energy is used mostly for biogas, biomass power generation and biomass heating, but the great amount of biomass is not yet used because the proper technology isn’t ready for it.

Biomass is a forestry by-product which can be used as to produce heat via combustion directly or indirectly after being converted to different biofuels.

As reported by China Daily, the country is promoting non-fossil energy, including biomass energy, to power its economy in a cleaner, more sustainable fashion. The government aims to lift the proportion of non-fossil energy in the energy mix to 20 percent by 2030 from the current level of around 11 percent.

At the moment, China’s energy mix is dominated by coal.

FORDAQ January 18, 2014

FSC to publish revised Chain of Custody standards

The FSC Board of Directors has approved revised FSC chain-of-custody standards FSC-STD-40-004 V3-0 and FSC-STD-20-011 V4-0. The revised standards will become effective on 1 April 2017.

The two revised standards are:

- FSC-STD-40-004 V3-0 Chain of Custody Certification (applicable to organizations that manufacture and trade FSC-certified products)

- FSC-STD-20-011 V4-0 Chain of Custody Evaluations (applicable to certification bodies evaluating organizations against FSC-STD-40-004)

The main purposes of this revision process were to simplify and streamline the chain-of-custody certification. Requirements have been simplified, including the addition of illustrative examples, tables, and graphics to clarify key concepts.

Content changes

The main content changes are the following.

- New transaction verification requirements: A new clause has been added requiring businesses to support transaction verification conducted by its certification body and Accreditation Services International (ASI), by providing samples of FSC transaction data as requested by the certification body. Further information on this will be communicated in the first quarter of 2017.

- Permitted application of percentage and credit systems at multiple site level, under certain conditions (also called “cross-site methods”): FSC will monitor the implementation of these requirements and re-evaluate them after two years.

- Refined credit system and product group requirements, including clarifying credit accounting for assembled wood products, and an extension of the credit accounting period from 12 to 24 months.

- Reduce the threshold for FSC-labelled recycled wood products from 85 per cent to 70 per cent (same threshold as required for FSC Mix products).

- A merger of advice notes and standard interpretations is incorporated into the standard.

China and the Fed: how different this time?

Renminbi mystery has a Beijing suspect

by: Gavyn Davies

Exactly a year ago this week, the mood in the financial markets started to darken markedly. As 2015 had drawn to a close, financial markets had seemed to have weathered the first increase in US interest rates since 2006 in reasonable shape. The Federal Open Market Committee had telegraphed its step to tighten policy in December 2015 with unparalleled clarity. Forewarned, it seemed, was forearmed for the markets.

Meanwhile, China had just issued some new guidance on its foreign exchange strategy, claiming that it would eschew devaluation and seek a period of stability in the RMB’s effective exchange rate index. This had calmed nerves, which had been elevated since the sudden RMB devaluation against the dollar in August 2015.

A few weeks later, however, this phoney period of calm had been completely shattered. By mid February, global equity markets were down 13 per cent year-to-date, and fears of a sudden devaluation of the RMB were rampant. It seemed that the Fed had tightened monetary policy in the face of a global oil shock that was sucking Europe and China into the same deflationary trap that had plagued Japan for decades. Secular stagnation was on everyone’s lips.

We now know that the state of the global economy was not as bad as it seemed in February, 2016. Nor was the Fed as determined as it seemed to tighten US monetary conditions in the face of global deflation. And China was not set upon a course of disruptive devaluation of the RMB. Following the combination of global monetary policy changes of February/March last year, recovery in the markets and the global economy was surprisingly swift.

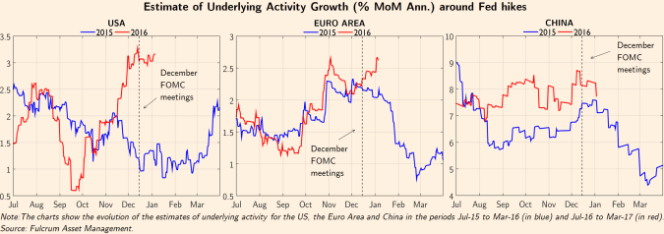

A year later, the key question for global markets is whether the Fed and the Chinese currency will once again conspire to cause a collapse in investors’ confidence. There are certainly some similarities with the situation in January 2016. The Fed has, once again, tightened policy, and China is battling a depreciating currency. But there are also some major differences that should protect us this time.

First, consider the attitude of the Federal Reserve. The main problem, a year ago, was that the FOMC seemed hell-bent on a pre-set course to “normalize” US monetary policy, almost regardless of events in the US economy and, especially, in the rest of the world. Of course, there were many caveats in the Fed’s communication of its intentions at the time, but the basic message was that the US economy had returned close to “normal”, while the setting of monetary policy was still highly abnormal.

The Fed believed that the headwinds that had slowed US growth for so long were waning, and was reluctant to believe that the equilibrium real interest rate (r*) had permanently dropped. There was scant belief in secular stagnation within the corridors of the Board’s headquarters on Constitution Avenue.

The markets, however, did not agree. The large gap between the FOMC’s predictions for US short rates, and the markets’ far lower expectations, proved that investor confidence was fragile. The collapse in markets in early 2016 was driven largely by widespread fears that US monetary tightening would persist in the face of an economy that was already slowing and vulnerable.

In short, the Fed seemed determined to administer an adverse monetary shock – an inappropriate tightening – on the slowing US economy, and this was spreading to the rest of the world via a possible devaluation of the RMB.

This year, the FOMC once again seems fairly hawkish, to judge from the FOMC minutes published last week. However, there is much less concern that the rise in US interest rates is inappropriate this time (see Tim Duy). In particular, according to the Fulcrum nowcasts, the US and Chinese economies are considerably more robust than they were a year ago, and even the Eurozone is doing quite well:

Instead of the adverse monetary shock that was happening a year ago, there has been a positive shock in global economic activity. Markets have reacted accordingly.

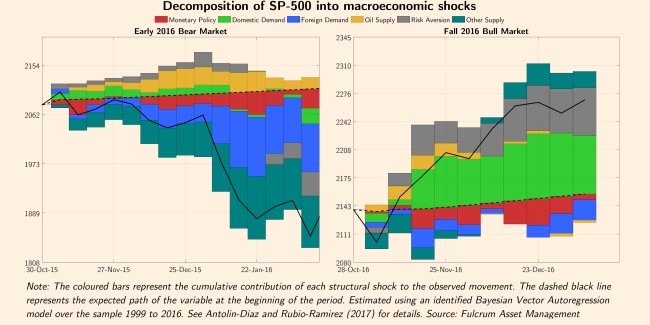

In both the monetary shock of 2015 and the activity shock of 2016, real bond yields and the dollar increased. But elsewhere the differences in market behaviour have been stark: inflation expectations have risen this time, instead of falling; and equities have surged, instead of collapsing. These are clear signs of a positive activity shock, not an adverse monetary shock.

Using the “economic shocks” model developed by Juan Antolin Diaz and colleagues at Fulcrum, the difference between last year and this year in the shocks that have been driving US equities is clear. Last year, Fed tightening, weak foreign demand and weak domestic supply pushed stocks down. This year, a positive domestic demand shock, and reduced risk premia, have triggered a bull market:

According to the model, the markets have not perceived the Fed tightening to be an adverse monetary shock this time. The FOMC is raising rates, but it appears much more concerned about foreign risks and the dollar than was true a year ago, and is less convinced about the need to return to a historic level for r*. Policy is genuinely “data determined” this year, which I think makes a hawkish monetary mistake far less likely.

What about China? Here, too, the strength of economic activity is clearly helping, and the Chinese authorities have shown a readiness to protect the RMB and stimulate the domestic economy when necessary. This makes the China factor less poisonous than it was last year.

However, the behaviour of the exchange rate continues to cause nervousness in markets. Before last week, the RMB’s effective index had been broadly stable for some months, but the currency had depreciated against the rising dollar. The capital outflow from China has continued at an alarming rate, caused mainly by domestic entities fleeing the currency, not by sales of the RMB by foreign investors.

The authorities have been forced to prop up the RMB by running down China’s foreign exchange reserves, and by tightening loopholes in outward capital controls. But this has not been sufficient, so last Wednesday the authorities intervened forcibly to buy RMB, and to squeeze liquidity in the offshore market for the currency. The result was the sharpest two-day rise in the Chinese currency in history as short term speculators were crushed.

This action was similar to that taken in January 2016, when the currency crisis last appeared to be getting out of hand. But it might also have been influenced by the possibility that incoming President Trump has threatened to label China as a currency manipulator as soon as he arrives in the White House on 20 January. Strong intervention to reverse the decline in the RBM would make this less likely – in a rational world.

So will the events of early 2016 repeat themselves in the near future? Global economic activity and the changed attitude of the Fed argue not. And the gradual RMB depreciation of 2016 leaves China inherently less vulnerable than it was a year ago.

But the Trump/China nexus is the risk that investors should be watching. If President Trump defies economic logic by labelling China as a currency manipulator, global market confidence could swiftly suffer a major setback.

China should fulfill global obligations by promoting structural reforms

7:49 pm, January 30, 2017

The Yomiuri Shimbun China must propel structural reforms aimed at realizing consumption-led economic growth while preventing its economy from plummeting, thus contributing to the stability of the world economy.

China’s gross domestic product posted annual growth of 6.7 percent last year, the country’s lowest growth in 26 years. Annual GDP growth has slackened for six consecutive years, with the underlying tone of an economic slowdown further intensifying.

Exports, the driving force of China’s economy, fell markedly. The decline is believed to stem from its weakened international competitiveness, centering on the manufacturing sector, due to rising labor costs that accompany economic growth.

China’s economy is the world’s second largest after the U.S. economy and is more than twice as large as Japan’s. Since the country joined the World Trade Organization in 2001, the exports of China as “the world’s factory” have soared, boosting its GDP.

Chinese President Xi Jinping has held up a policy of shifting China’s economic growth pace to a “new normal,” from rapid growth to stable domestic demand-led growth. The question is how deep-rooted the structural problems impeding the transition are.

China’s 4 trillion yuan stimulus measures, implemented in the wake of the financial crisis triggered by the collapse of Lehman Brothers, propped up the world economy. Now, however, the stimulus has become a negative legacy for the country, weighing on its economy.

The country’s steel industry is burdened with excessive production facilities, whose capacity is as much as four times that of Japan. Already more than half of its steelmakers are said to be so-called zombie companies, which have effectively collapsed.

Prevent capital outflow

The liquidation of unprofitable enterprises is a very difficult problem to deal with. This is because provincial governments, which dislike increases in unemployment, oppose this. As nonperforming loans held by financial institutions have piled up, a sense of unease has spread, which stems from the real state of affairs being kept in the dark.

What the new U.S. administration under President Donald Trump will do is likely to add to such worries, with Trump increasing his criticism of China, the U.S. trading partner with which it has the largest trade deficit.

If trade friction between the United States and China becomes a reality, it would embroil many other countries that have deep economic ties with the two countries, and thus likely depress the world economy.

China needs to expedite its efforts to correct its overproduction so as not to foster U.S. protectionism.

At the World Economic Forum held recently in Switzerland, Xi said, “We must … promote trade and investment liberalization … and say no to protectionism.” He was probably trying to hold in check Washington’s hardline stance against China. But we cannot help but feel a sense of discomfort.

In China there remain many restrictions on foreign capital and opaque administrative guidance and the like. Its domestic market is by no means open to foreign countries.

Against the backdrop of the uncertain economic situation, capital outflows from China are continuing. The Chinese authorities have been driven to take yuan-buying and dollar-selling interventions with its foreign currency reserves, which once reached close to $4 trillion, dropping to $3 trillion late last year.

China should make efforts to carry out structural reforms, such as improving the investment environment for foreign capital, rather than merely criticize protectionism.

(From The Yomiuri Shimbun, Jan. 30, 2017)Speech

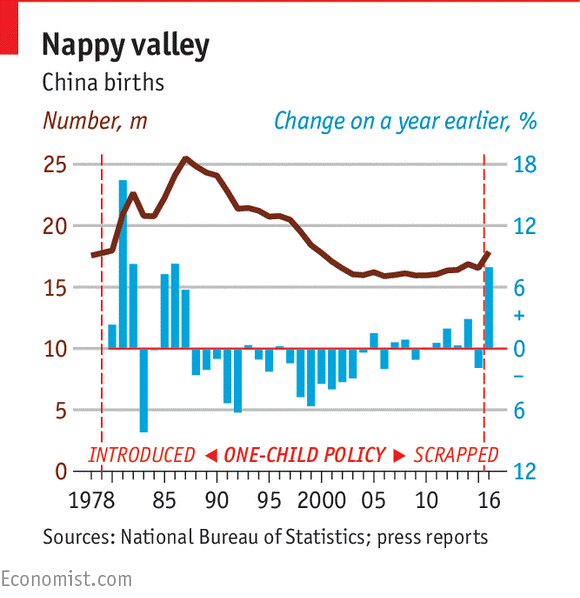

Understanding the spike in China’s birth rate

Will it end the country’s fertility woes?

Jan 25th 2017 | BEIJING | China

WHEN China’s government scrapped its one-child policy in 2015, allowing all couples to have a second child, officials pooh-poohed Western demographers’ fears that the relaxation was too little, too late. Rather, the government claimed, the new approach would start to reverse the country’s dramatic ageing. On January 22nd the National Health and Family Planning Commission revealed data that seemed to justify optimism: it said 18.5m babies had been born in Chinese hospitals in 2016. This was the highest number since 2000—an 11.5% increase over 2015. Of the new babies, 45% were second children, up from around 30% before 2013, suggesting the policy change had made a difference.

Confusingly, the National Bureau of Statistics announced its own figures at the same time: it said the number of births had risen by 8% to 17.9m (see chart). These numbers were based on a sample survey of the population, not hospital records, hence the difference. But both sets of figures used valid methods of calculating a birth rate and both showed a significant rise. Yang Wenzhuang of the health and family-planning agency said the increase showed the introduction of a two-child policy had come “in time and worked effectively”.

It always seemed likely that the one-child policy was a little like a dam, with couples wanting a second child banked up behind it. As soon as the flow of the dam was changed, they would have their desired babies quickly. That seems to have happened. It might also have made a difference that 2016 was the year of the monkey in the Chinese zodiacal calendar. This is considered a propitious year. Chinese couples have sometimes chosen to have a child under such a sign, rather than (say) in the less lucky year of the chicken, which begins on January 28th. So there were one-off reasons for the number of births to rise.Alas, it is far too early to claim victory. There are several reasons for thinking the rise in births is a spike, and very few causes to believe the underlying fertility rate (the number of children a Chinese woman can expect to have during her lifetime) has risen much, if at all.

Even so, the increase was smaller than expected. When they introduced the two-child policy, family-planning officials forecast that between 17m and 20m babies would be born every year between 2015 and 2020—an increase of about 3m a year. In the event the increase in 2016 was only 1.3m. Moreover, if pent-up demand explains much of the increase, that influence will fade. After a brief spate, the flow of water through the dam will go back to what it was before—unless there is a change in China’s underlying fertility rate, meaning unless the average woman of child-bearing age decides she wants more children.

So far, that does not seem to be happening. It is true that the short-term rise in births may be hiding long-term changes but, anecdotally, there is little sign yet of a shift towards wanting larger families. More than 30 years of relentless propaganda have persuaded most Chinese that “one is enough”. In a government survey in 2015 three-quarters of couples said they did not want a second child, citing the cost of child care and education. People’s Daily, the Communist Party’s main mouthpiece, recently lamented that China’s fertility rate, at 1.05, was the lowest in the world (others put the rate a little higher). It has fallen consistently since 1950.

Even if the fertility rate were to rise, it might not be enough to offset the continuing influences of the one-child policy and the destruction of female fetuses that accompanied it. Because of these, the number of women of child-bearing age (15-49 years) is due to fall by about 5m each year in the next four years. So if the fertility rate stays the same, the number of births will start falling, because there will be fewer mothers to bear children.

And that in turn would mean the remorseless greying of China would continue. At the moment, one in seven of the population is over 60. By 2050, the share will rise to more than one-third. China will need more than a change in the one-child policy or a spike in the birth rate to reverse that.

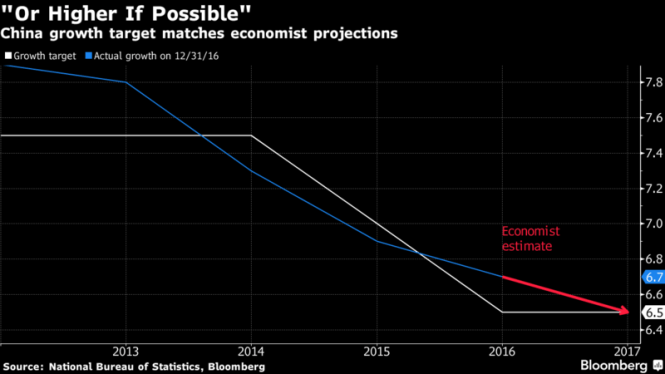

China Sets Growth Target of About 6.5% Amid Pledges to Ease Risk

Bloomberg News

March 4, 2017, 5:33 PM MST March 4, 2017, 11:38 PM MST

- M2 money supply growth objective lowered to about 12%

- CPI target increase about 3%, retail sales growth of about 10%

Takeaways From China’s National People’s Congress

China set a 2017 growth target of “around 6.5 percent, or higher if possible” as focus shifts to easing risk and ensuring stability before a twice-a-decade leadership transition this year.

The objective outlined Sunday in Premier Li Keqiang’s work report to the National People’s Congress in Beijing compares with last year’s target rangeof 6.5 percent to 7 percent. Economists surveyed by Bloomberg project 6.5 percent expansion this year.

Read More: China dials back defense spending increases

Other objectives included:

- M2 money supply growth target was cut to about 12 percent from 13 percent last year

- Consumer price index target of about 3 percent increase was unchanged from last year

- Fiscal budget deficit ratio goal at 3 percent of gross domestic product, also unchanged

- Yuan exchange rate will be further liberalized, Li says in report

Top leaders working to steady economic growth also are shifting to a more neutral policy to reduce financial risks from excessive borrowing. Economic and social stability are key priorities before President Xi Jinping and his cadres gather later for a reshuffling of top officials, which is planned for the fourth quarter.

“China has lowered the economic development targets across the board,” said Zhou Hao, an economist at Commerzbank AG in Singapore. “China’s policy stance has turned to risk control and bubble deflating. This means that the monetary policy will gradually tighten.”

The report said “the RMB exchange rate will be further liberalized, and the currency’s stable position in the global monetary system will be maintained.” That’s a change from last year’s language saying the market-based mechanism for setting the exchange rate will be improved “to ensure it remains generally stable at an appropriate and balanced level.”

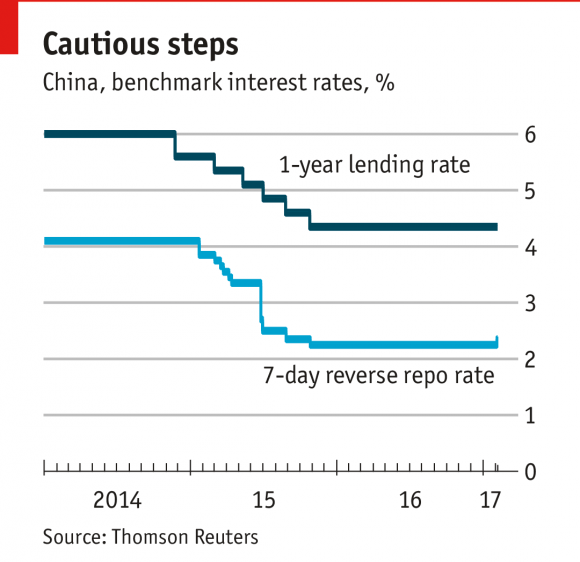

The work report reiterated that China will pursue a prudent and neutral monetary policy this year. The People’s Bank of China has left the benchmark interest rate at a record low while starting to tighten money market rates, and analysts expect further measures to cool lending without choking the wider economy ahead of the 19th Communist Party Congress.

Li’s report sounded a hopeful note with the addition of language calling for growth above the target if possible, while also emphasizing the need to reduce threats to that expansion. China is confident it can keep systemic financial risk in check, and is “highly cautious” of the dangers from bad loans, bond defaults, shadow banking and online finance.

Despite pledges to keep an eye on emerging risks, the credit taps are still flowing freely. Aggregate financing, the broadest measure of new credit, climbed to a record 3.74 trillion yuan ($545 billion) in January. The credit-to-GDP ratio rose nearly 100 percentage points in eight years to 260 percent by the end of 2016, according to Bloomberg Intelligence estimates.

Top leaders also face external uncertainty. Potential threats include a sharp drop in exports due to slowing demand or rising trade barriers — U.S. President Donald Trump has promised tariffs on Chinese goods — and faster-than-expected rate hikes by the Federal Reserve.

Here’s What to Expect at China’s NPC

Read More: What to Watch at China National People’s Congress

The work report also outlined objectives for attacking excess capacity by cutting 150 million metric tons of coal capacity this year and reducing steel capacity by 50 million metric tons. Urban home buying by both local and new residents will be supported, while another 6 million housing units will be renovated in urban areas, according to Li’s report.

Financial regulation will be “proactively and prudently reformed” and the industry’s ability to serve the real economy will be strengthened, the report said. Officials also vowed to accelerate reforms of state-owned enterprises and said “more will be done to energize the non-public sector.” They also plan more support for technological innovation and the development of emerging industries.

Bottom of Form

The annual gatherings of the NPC and the Chinese People’s Political Consultative Conference, are known as the “two sessions.” They include release of Li’s government work report and accompanying reports from the Ministry of Finance and top economic planning body, the National Development and Reform Commission, outlining plans for everything from ammonia nitrogen emissions to mobile phone roaming charges

‘Very High’

Michael Tien, a delegate from Hong Kong and chairman of clothing retailer G2000 Group, said he was “surprised” by the GDP target and thought it was “very high.” “I don’t think China can sustain such growth if they only look at the domestic market,” he said in an interview on the sidelines of the gathering. “They really need to open up, get foreign investment in.”

Over the longer term, policy makers aim for a 6.5 percent average growth pace in the five years through 2020 to achieve the party’s promise of building a “moderately prosperous society” with GDP and income levels double those of 2010. Xi isn’t wedded to the 6.5 percent goal due to concerns about rising debt, a person familiar with the situation told Bloomberg News in December.

The upcoming Party Congress marks a critical juncture in Xi’s leadership and will show the extent to which he has consolidated support since taking power in 2012. If retirement conventions hold, 11 of 25 Politburo members — including five of seven members on its supreme Standing Committee — would be expected to step down, leaving positions open.

Party leaders have repeatedly emphasized the need to maintain control before the conclave. Xi told a meeting of his National Security Commission — its first known meeting since 2014 — that safeguarding “political security” was the top priority.

“A slightly lowered and somewhat more flexible growth target is about as good as we could have asked for,” said Andrew Polk, Beijing-based head of China research at Medley Global Advisors, which advises institutional investors. “We’d still like to see an abandonment of the growth target altogether, but that is just not in the DNA of China’s government.”

China Economy, Construction & Lumber Shipments | Canada Wood Group

http://canadawood.org/wp-content/themes/canadawood/js/html5.js

China Economy, Construction & Lumber Shipments

January economic highlights (China):

- China’s economy situation was generally positive in 2016 thanks to a growth in consumers spending and a property market rebound.

- GDP grew 6.8% year-on-year during Q42016, which is slightly more than the grow forecast of 6.7% as indicated in a Reuters poll of 42 economists.

- China’s economy managed to expand the fastest rate in Q4 in 2016 despite that the property market was tightened with less decisive policy support. Experts believe that increasing retail sales and manufacturing activities are the main source of growth.[i]

- China’s wood import in 2016 has reached 80.24 million m3 – setting a new record -and increased 13.2% compared to last year.

China’s GDP growth rate in Q42016 reached 6.8% with 6.7% growth in the full year, which fit the estimation from head of China’s state planning agency; consumption constitutes for 64.6% GDP in 2016 while annual per capital consumption was up 8.9% year-on-year to RMB 17,111 (USD 2,490).[ii]

Caixin PMI decreased to 51.0 in January 2017 from 51.9 in December 2016. December had marked the seventh back-to-back month growth period.[iii] Exports from China dropped 6.1% year-on-year to USD 209.42 billion in December 2016 with a revised 1.6% drop in November against an expected drop of 3.5%; Sales decreased 7.7% in the full year of 2016 which is the second year of decline and the lowest since the global financial crisis of 2009.[iv]

China Consumer Price Index (CPI) dropped to 102.10 Index Points in December (102.30 in November 2016).[v] USD/CNY fluctuated from 6.89 (December 1st) to 6.94 (December 31st) and 6.94 (January 1st) to 6.88 (January 30th)[vi]; CAD/CNY stayed level at 5.17 on both December 1st and 31st but increased from 5.17 (January 1st) to 5.28 (January 30th)[vii].

Real Estate Construction Market

In 2016 the total investment in national real estate reached RMB 10258.1 billion, growing 6.9% year-on-year;[viii] in the same year construction floor area started increased to 1.67 billion m2 with 8.1% growth year-on-year; residential floor area started was up to 1.16 billion m2 with 8.1% growth year-on-year.[ix]

Construction: floor area started

Taiwan GDP Q4 2016

Taiwan: Economy shows solid growth in fourth quarter of 2016

February 13, 2017

Taiwan’s GDP increased 2.6% year-on-year in Q4 2016, accelerating from the 2.0% increase in Q3, marking the fastest pace of growth since Q2 2015. The result nevertheless missed the 2.9% increase the markets had expected. Sequentially, economic growth moderated. GDP—adjusted for seasonal factors—expanded 0.5% from the previous quarter in Q4, which was down from the 1.0% rise in Q3.

The headline figure continued to suggest positive economic dynamics and looking at the details, exports of goods and services accelerated substantially in the final quarter of 2016 (Q4: +8.2% year-on-year; Q3: +3.6% yoy). Imports also jumped (Q4: +9.4% yoy; Q3: +5.3% yoy), bringing the contribution from net exports to overall economic growth to 0.4 percentage points in Q4, swinging from a 0.4 percentage-point drag in Q3. In terms of domestic demand, private consumption slowed from a 2.5% increase in Q3 to a 1.3% expansion in Q4. Growth in gross investment picked up from a 3.1% increase in Q3 to a massive 8.2% expansion in Q4, supported by a strong rebuilding of inventories. On a negative note, government consumption decreased 1.1% in Q4, which was the first fall since Q1 2015.

In the full year 2016, Taiwan’s economic growth was 1.4%, strengthening from the 0.7% expansion in 2015. Taiwan’s economy is one of the most exposed to China’s and Q4’s acceleration is consistent with a modest upturn in GDP growth in China in the final quarter of the year.

The government expects GDP to expand 1.9% in 2017. FocusEconomics Consensus Forecast panelists project GDP to grow 1.8% in 2017, which is unchanged from last month’s forecast. For 2018, the panel estimates that economic activity will increase 2.0%.

Author: Ricardo Aceves, Senior Economist

SAMPLE REPORT

Looking for forecasts related to GDP in Taiwan? Download a sample report now.

Taiwan GDP Chart

Note: Year-on-year changes of GDP in %.

Source: Directorate General of Budget, Accounting and Statistics (DGBAS) and FocusEconomics Consensus Forecasts.

Technology | Mon Jan 9, 2017 | 5:50am EST

UPDATE 2-Taiwan’s Dec export spurt may mean factories keep firing into Q1

* Exports +14.0 pct y/y, beats forecasts

* Shipments to China +21.4 pct y/y; to U.S. +2.0 pct

* Exports to Japan +10.2 pct y/y; to Europe +0.1 pct

* 2016 exports contract for 2nd year, -1.7 pct (Releads, adds more comment from official and analysts)

By Jeanny Kao and J.R. Wu Rueters

TAIPEI, Jan 9 Taiwan’s exports bounced to a four-year high in December, fuelling hopes that global demand for technology goods and commodities will keep the island’s exports strong through the first quarter.

The third monthly rise in exports, however, was not enough to help full-year shipments stay out of the red or subdue worries about rising global trade protectionism.

The island’s tech-dominated manufacturers are nervous about the policies of incoming U.S. President Donald Trump, who has threatened to raise tariffs on imports from some countries when he takes office on Jan. 20.

“We cannot assess the exact impact. It is only after he takes office that we will know exactly how he will implement (his policies),” Beatrice Tsai, an official with Taiwan’s finance ministry, told a news conference on Monday.

ADVERTISING

Tsai said improved momentum reflects the global recovery and also stronger orders ahead of the long Lunar New Year holiday at the end of January, when factories in China and Taiwan grind to a halt.

ADVERTISING

“We expect double-digit growth extending into the first quarter of this year. However, it would be a difficult job to maintain the same level of growth beyond the first quarter,” said Tony Phoo, Northeast Asia senior economist at Standard Chartered Bank.

Taiwan’s recent export-related data could signal a stronger first quarter, which tends to be a cyclically weaker period and is coming from a low base. A measure of manufacturing activity in December showed operating conditions at their best in nearly six years and pointed to new business ahead at home and abroad.

Annual exports in December rose 14 percent, beating a 10.4 percent forecast in a Reuters poll and the fastest pace since January 2013’s 21.9 percent gain.

Exports to China – where many Taiwan factories are located – leapt 21.4 percent, finance ministry data showed.

Shipments of electronic components, and the sub-category of integrated circuits, showed solid gains of more than 20 percent in December, while those related to smartphones rose just over 9 percent, data showed.

Exports of base metals, chemicals and transportation equipment posted double-digit growth.

But full-year exports fell for a second year in a row by 1.7 percent, while imports dropped 2.6 percent.

Goldman Sachs cautioned that rising trade barriers could limit export growth prospects in Asia this year, and it expects little monetary tightening in the region even if the Federal Reserve keeps raising interest rates.

“Downside risks to exports from increased trade protectionism look substantial,” the investment house said in a research note on Monday.

Taiwan’s trade surplus with the United States, its second-largest trading partner last year, fell to $4.92 billion, compared with $5.35 billion in 2015 and is down from highs of as much as $8.8 billion five years ago, ministry data showed.

Officials have said that Taiwan’s trade surplus with the United States is within acceptable levels that shouldn’t trigger protectionist attention from the incoming Trump government. (Editing by Jacqueline Wong)

Taiwan Ratings upbeat on Taiwan’s GDP growth in 2017, 2018

2017/01/18 19:37:23

Taipei, Jan. 18 (CNA) The Taiwan Ratings Corp. (TRC) has predicted that Taiwan will see growth of 2 percent in its gross domestic product (GDP) this year and a 2.5 percent rise in 2018, surpassing the levels of both Hong Kong and Singapore.

Taiwan’s economic growth will jump from 0.9 percent in 2016 to the levels forecast by the rating agency’s mother company, Standard & Poor’s International, the TRC said in its 2017 Taiwan Credit Outlook report, published on Wednesday.

The 2 percent GDP growth for this year will be higher than the 1.7 percent predicted for Hong Kong, and the 1.3 percent for Singapore, the report said.

In the report, South Korea is forecast to achieve GDP growth of 2.7 percent in 2017, the highest among the so-called “Four Asian Tigers” — Taiwan, Hong Kong, Singapore and South Korea.

GDP in 2018 will see growth of 2.9 percent in South Korea, 2.5 percent in Taiwan, 2.0 percent in Hong Kong and 2.0 percent in Singapore, according to S&P’s rating.

TRC credit analyst Lan Yu-han said Taiwan’s economic development will benefit from a gradual recovery of the U.S. economy in the coming two years, as well as economic stability in the emerging countries.

These two factors are expected to help boost Taiwan’s exports in the near future, Lan said.

However, the growth momentum might be slow in the first few months of this year due to a slow recovery in mainland China and Europe and increasing competition from other exporters, Lan said.

(By Tsai Yi-chu and Elizabeth Hsu)

ENDITEM/J

Monetary metaphysics: China

If interest rates rise in an economic forest and no one hears a central-bank statement, do they still make a tightening sound? This is the metaphysical question of Chinese monetary policy these days. Last week the People’s Bank of China nudged up rates on a series of short-term liquidity tools that lenders can tap if short on cash. But it left benchmark rates untouched and also offered no explanation for its moves. Still, its intentions seem plain enough: worried about a property bubble and excessive credit growth, the central bank wants to tighten monetary conditions. At the same time, it hopes to avoid panicking financial markets or weighing too heavily on growth. So far, investors remain content, pricing in mild downward pressure on stocks and bonds, and not overreacting. But the Chinese central bank is walking a tightrope. It has only taken the first step; keeping balance will get harder.

Squeezed to life

China’s currency upsets forecasts by beginning the New Year stronger

A liquidity squeeze thwarts investors hoping to profit from a falling yuan

From the print edition | Finance and economics

Jan 14th 2017

THE omens for the Chinese yuan seemed bad heading into 2017. The capital account looked as porous as ever, making a mockery of the government’s attempts to fix the leaks. The new year, when residents received fresh allowances for buying foreign currency, was due to bring even more pressure. Analysts braced for a stampede for the exits from China. The yuan had fallen sharply at the beginning of 2016, catching them by surprise. This time, they were ready.

Instead, the yuan began the year as one of the world’s star performers. This was particularly so in the offshore market, where foreigners trade it most freely. It gained 2.5% against the dollar over two days in the first week of 2017, its biggest two-day increase since 2010, when trading began in Hong Kong, its main offshore hub. Within China itself, price increases were more subdued, but the yuan still climbed to a one-month high.

Currency markets are notoriously fickle, so it is dangerous to read too much into a few days of price swings. But in China the government has always had a tight grip on the yuan. So the currency’s strength raised the question of whether it was simply being propped up—or whether the yuan’s prospects were in fact improving.

The Hong Kong rally has the Chinese central bank’s fingerprints all over it. The proximate cause was a shortage of yuan in Hong Kong. As its residents have turned away from the Chinese currency, deposits there have fallen to just over 600bn yuan ($86.7bn), their lowest level since early 2013. That has led to periodic liquidity squeezes, making the cost of borrowing yuan in Hong Kong prohibitive: the overnight rate soared to 61% at the start of 2017.

In normal circumstances, central banks would be expected to inject money to ease such shortages. But the Chinese authorities did little to stem the cash crunch, pleased to see it hurt those betting against the yuan. To make money by “shorting” a currency, investors borrow it, sell it and then hope to buy it back after its value has fallen. With borrowing rates so high, this becomes all but untenable. As the liquidity squeeze has abated in recent days, the offshore yuan has pared its earlier gains.

China’s success in defending the yuan suggests that, as the government tightens capital controls, they are having more effect. In the past two months it has started reviewing all transfers abroad by companies worth $5m or more. Transfers by individuals will also soon face more scrutiny. The controls should slow the erosion of China’s foreign-exchange reserves, which are down to $3trn from $4trn in 2014.

Most important, the Chinese economy is sounder than it was two years ago, when the yuan’s gradual descent began. A property boom has breathed life into heavy industry. Producer-price inflation is running at its fastest in more than half a decade. The central bank is tightening monetary conditions, however gingerly. As China’s economic and policy cycles more closely track those in America, there is less scope for runaway strength in the dollar, which in turn takes pressure off the yuan.

Even so, many of the factors remain that led the yuan to drop by 7% last year, its steepest fall on record. The broad money supply is still growing at a double-digit rate. Chinese companies and households still have a ravenous appetite for foreign assets. Most analysts expect the yuan soon to start falling again, though that consensus is no longer rock-solid. China’s central bank has long said that it wants to make the yuan more volatile and less predictable. On that score, it has surely succeeded.

This article appeared in the Finance and economics section of the print edition under the headline “Squeezed to life”

China’s New Banking Regulator Chief Faces Daunting Challenges

Bloomberg News

February 23, 2017, 11:20 PM MST

- Rise in shadow banking and bad loans are among risks

- Guo Shuqing said to head China Banking Regulatory Commission

Guo Shuqing.

Photographer: Sim Chi Yin/Bloomberg

China has appointed Guo Shuqing as the new head of the banking regulator, according to people familiar with the matter. Having spent much of his life working on transforming the nation’s financial system, Guo, 60, faces daunting tasks ahead as he takes on oversight of the world’s largest banking industry by assets. Below are five charts highlighting some of the biggest issues.

- Shadow Banking

Bottom of Form

Shadow banking is now in every segment of China’s financial system, prompting authorities to work together to address growing risks. The central bank and the securities, banking and insurance regulators are drafting new rules for asset-management products that have swollen to almost $9 trillion as of June 30. So-called wealth-management products issued by banks surged 30 percent last year, making them the largest component of the banking system that exists largely outside of lenders’ balance sheets.

- Liquidity Risks

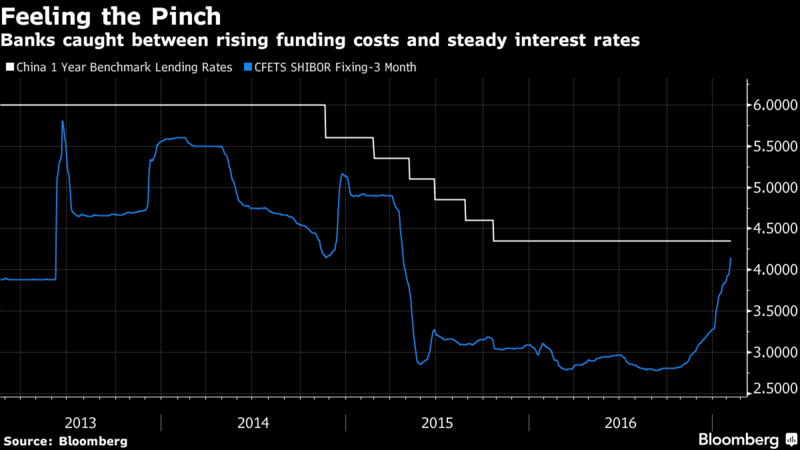

Banks have increased reliance on funding their operations by borrowing from each other with short-term instruments such as negotiable certificates of deposit, raising risks of a liquidity shock. Difficulty selling the securities is fueling concerns that smaller lenders could face cash crunches and even miss payments.

- Profit Slowdown

China’s largest lenders are expected to post their first decline in annual profit in more than a decade. Earnings growth has slowed in recent years because of swelling bad loans and pressure on lending margins.

- Funding Costs

Policy makers’ recent drive to reduce financial-system risks is squeezing banks. Caught between the central bank’s intensifying efforts to raise short-term borrowing costs, and benchmark interest rates that haven’t moved since 2015, Chinese lenders have few options but to absorb much of the higher costs.

- Bad Loans

China’s economy is growing at the slowest pace in a quarter century, adding urgency to the banks to clean up bad loans. Official figures on soured debts are widely believed to understate the true scale of the problem, with CLSA Ltd. estimating the non-performing loan ratio at 15 percent to 19 percent for 2015 — about 10 times higher than the official 1.67 percent.

Getty Images

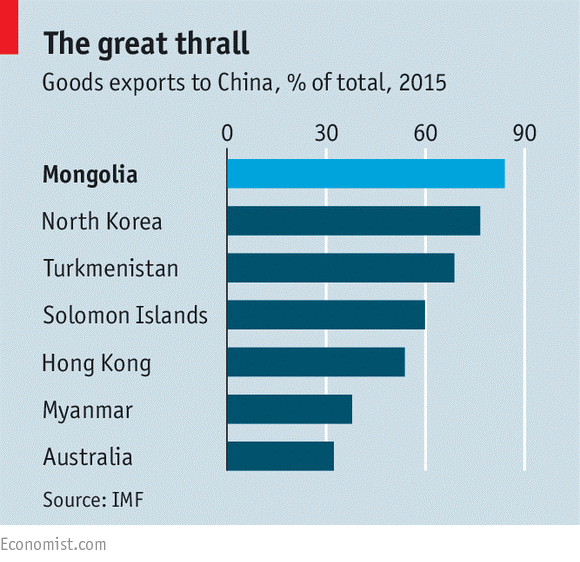

This might yurt!

The IMF bails Mongolia out—again

Every commodity bust brings a balance-of-payments crisis

Feb 25th 2017

WHEN Jim Anderson first lived in Mongolia in 1993, there was one local word foreigners could not help but learn: baikhgui, which translates as “absent” or “unavailable”. Bread? Rice? Electricity? Often as not, they were baikhgui, he recounts in a blog post for the World Bank, for which he has returned to Mongolia as country director. Even those lucky enough to have American currency to spend in “dollar shops” received sticks of chewing gum as change.

Mongolia thought it had left those days far behind. A mining boom (copper, coal, gold) has transformed the country, filling the shops with goods and the cities with cranes. From 2009 to 2014, the economy grew by 70%. In 2012 alone, it attracted foreign-capital inflows equivalent to some 54% of its GDP. But since 2014 commodity prices have fallen, foreign-direct investment has reversed and a number of daunting debt payments have crept closer. Mongolia’s foreign reserves have dwindled from over $4bn in 2012 to little more than $1bn at the end of September, equivalent to about four months of imports. Foreign creditors were about to learn the word baikhgui.

Enter the IMF. This month it agreed to lend Mongolia about $440m over three years to help it avoid default and rebuild its reserves. Assuming the agreement is approved by the fund’s board, it should unlock another $3bn or so from the Asian Development Bank, the World Bank, Japan, South Korea and others.

China should also help. Irked by the Dalai Lama’s visit in November, it imposed new duties on Mongolian goods and delayed lorries at the border. A little over 50% of Mongolians identify as Buddhist. But almost all the country’s exports (84%) are sold to China, making it the most China-dependent exporter in the world (see chart). Mongolia’s government has apologised for the “misunderstanding” caused by the visit and said it will not permit a repeat. It now hopes China will extend a 15bn yuan ($2.2bn) swap line.

The strings attached to the IMF’s loan are more conventional. They include keeping the central bank out of “quasi-fiscal” activities: it had bought cheap-rate mortgages worth 1.95trn togrog ($787m), helping to support a housing bubble in a country known for nomadism. At the IMF’s urging, the government is also distancing itself from the management of the Development Bank of Mongolia, a state lender that accounts for over a fifth of credit in the country.

Mongolia’s prospects should improve. Copper and coal prices have recovered somewhat. The economy will also benefit from heavy investment in Oyu Tolgoi, a copper mine operated by Rio Tinto. But Mongolia has turned to the IMF twice in eight years. If it does not manage the next commodity cycle better, it might find that its benefactors’ patience is baikhgui.

Mongolia to spend India’s one billion USD loan on infrastructure

By Ch.KHALIUN

During his state visit to Mongolia last year, Prime Minister of India Narendra Modi promised to provide one billion USD in loans. Mongolian Mining Journal interviewed Minister of Foreign Affairs L.Purevsuren about details on the loan agreement and plans for spending.

Last May, India said that it would provide a one billion USD loan to Mongolia. What will it be used for?

In May 2015, Prime Minister Narendra Modi paid an official visit to Mongolia. During the visit, the prime ministers of Mongolia and India held official negotiations and exchanged views on expanding cooperation and relations between the two countries. Prime Minister Modi reported that the Government of India had decided to open a one billion USD credit line for ensuring Mongolia’s economic growth, based on the importance of Mongolia’s infrastructure sector development.

This is a long-term concessional loan. Does the Indian side have any requirements for the loan’s conditions and spending?

Since 1990, Mongolia has taken out 27.5 million USD in concessional loans from India, which makes up one percent of the nation’s total concessional loans. Prime Minister Modi underlined that the loan will be issued for the nation’s infrastructure sector. The Indian side proposed a concessional loan with a 1.5 percent annual interest rate and an eight-year repayment period. At the beginning of April, government representatives from the Cabinet Secretariat, Finance Ministry, Foreign Affairs Ministry, and Roads and Transportation Ministry visited Delhi to negotiate with the Indian side on softening the loan conditions. As a result, the concessional loan will issued for a 25-year period with a 1.75 percent annual interest rate, and Mongolia will be exempt from repaying the principal payment of the loan for the first seven years after receiving funds. We are now working toward establishing the general loan agreement. We are planning to spend the money on infrastructure, especially in the railroad sector.

Are there any other loans or financial assistance that will be provided to Mongolia in 2016?

In addition to the concessional loan from India, we are negotiating on a one billion USD loan from China’s Exim Bank. The issue of taking out loans from Asian Development Bank, World Bank, and other international banks and financial organizations remains open. These issues will be regulated in accordance with the Law on Debt Management.

Short URL: http://ubpost.mongolnews.mn/?p=19359

VN can meet 6.8% growth target in 2017: Forbes

Update: January, 09/2017 – 16:30

HÀ NỘI – Việt Nam will keep attracting investment, expanding export production and watching domestic consumption spread in 2017, according to Forbes’ forecast.Viet Nam News

The country can also meet its economic growth target of 6.8 per cent set by the Government thanks to these advantages, Forbes said.

According to Forbes, US President-elect Donald Trump is expected to scrap Trans-Pacific Partnership (TPP), the 12-nation trade agreement that would particularly help member Việt Nam as an exporter. However, there are some who suspect Trump will somehow salvage it.

If not, according to Forbes, Việt Nam already takes part in 16 free trade agreements (FTAs), including with economic powerhouses China and Japan. It can pursue bilateral agreements with other TPP members if the US Congress declines to ratify the deal signed in 2016.

Việt Nam is also on the list to join a Chinese-championed Regional Comprehensive Economic Partnership trading group that would encompass 30 per cent of the world’s GDP.

Besides this, Việt Nam will also keep giving foreign companies reasons to invest, Forbes said, adding that foreign investors already benefit from lower tariffs under the trade deals. Some also get lavish tax breaks.

In 2015, the country made its rules on foreign investment clearer and sped up permit processing.

Last year was a “transition year” for those changes, and in 2017, Việt Nam will start to “collect the fruits of having a more structured and competitive business legislation, which has had an impact on attracting more FDI and also helped Việt Nam become one of the major manufacturing hubs in the world,” Forbes quoted Oscar Mussons, international business advisory associate with Dezan Shira & Associates consultancy in HCM City, as saying.

In addition, Vietnamese people are getting richer and spending more. The country’s middle class will double by 2020 to 33 million people and that means more consumption, the Boston Consulting Group estimated last year. People in that group earn at least US$714 per month, enough for phones, motorcycles, travel and health products, items that usually make the short list of local consumer preferences.

The middle class has got where it is because wages are rising along with a boom in jobs linked to growth in export manufacturing.

According to Forbes, factory work in Việt Nam is moving up in value from traditional industries. High-tech’s share of total exports from the country reached 25 per cent in 2015 from five per cent in 2010 and kept going last year, with no signs of abating currently.

Investments by electronics giants Hon Hai Precision, Intel and Samsung – worth billions of dollars – have led the shift. Samsung Display is considering a new $2.5 billion investment in a project already worth about $4 billion, according to a stock market research firm in Hà Nội.

Electronics are replacing traditional industries, such as garments and shoes, production of which is slowly moving to other Asian countries.

Policymakers in Việt Nam aim to increase annual export value by 8-10 per cent this year, Louie Nguyen, editor and founder of the news website Vietnam Advisors, said. The trend will bring new skills, higher wages and more revenue for those companies making high-value products.

Private business is, meanwhile, expanding and doing more kinds of work in Việt Nam. – VNS

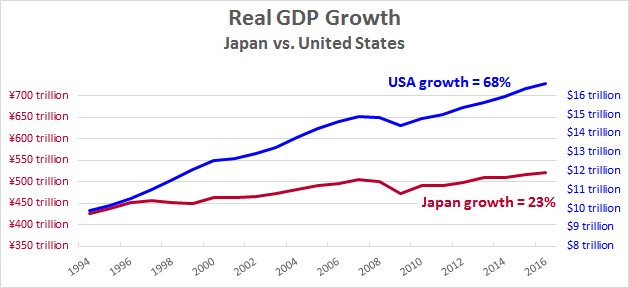

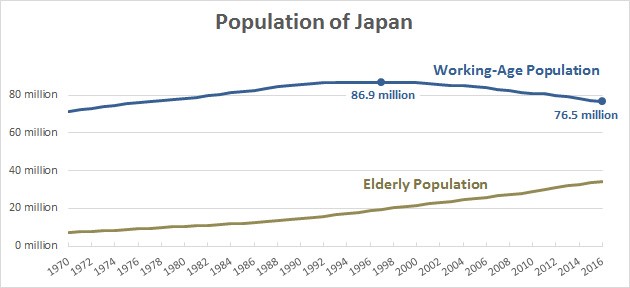

The Enduring Mystery of Japan’s Economy

KEVIN DRUMFEB. 27, 2017 9:50 AM

The Wall Street Journal writes today about Japan’s stagnant economy and persistent deflation:

During Japan’s go-go 1980s, Hiromi Shibata once blew a month’s salary on a cashmere coat, wore it a few times, then retired it. Today, her daughter’s idea of a shopping spree is scrounging through her mom’s closet in Shizuoka, a provincial capital.

….The U.S. appears to be leading other parts of the globe out of an extended era where central banks relied heavily on low and negative interest rates and stimulus to jump-start growth and keep prices from falling….Japan remains definitively stuck, despite a long and aggressive experiment with ultra-low rates. A quarter-century after its property bubble burst, a penny-pinching generation has come of age knowing only economic malaise, stagnant wages and deflation—a condition where prices fall instead of rise.

….Since then, annual growth has averaged less than 1% amid periodic recessions. Prices began falling in the late 1990s….Many economists believed the Bank of Japan’s 2013 stimulus would be enough to jolt the nation out of its downward spiral of weak growth and falling prices….Some economists contend the government should try even more fiscal stimulus and monetary easing. Others argue the stimulus has already saddled Japan with so much debt—now 230% of gross domestic product—that it could end in an economic collapse.

It’s true that Japan has suffered through two decades of low growth:

But there’s way more to this story. Obviously, the bigger your population, the bigger your GDP. The fact that the Russia has a bigger GDP than Switzerland doesn’t mean it has a better economy. It just means it’s bigger. The key metric to judge whether an economy is in good shape is GDP per working-age adult, since that tells you how productive your workers are. So let’s look at that:

Despite its persistently low inflation, Japan’s economy is doing fine. Their GDP per working-age adult is actually higher than ours. So why are they growing so much more slowly than us? It’s just simple demographics:

Japan is aging fast. Its working-age population peaked in 1997 and has been declining ever since. Fewer workers means a lower GDP even if those workers are as productive as anyone in the world. Now put all this together, and here’s what you get:

This is GDP per capita. That is, the amount of stuff that Japan produces for each person in the country. Over the past two decades it’s grown 20 percent. And aside from the Great Recession, that growth has been pretty steady. It’s not declining. It’s not stagnating.

Under the circumstances, Japan is doing fine. Each of their workers is as productive as ours, and their productivity has actually grown a little faster than ours. But there’s only so much you can do when your population is declining. Given the demographic realities, Japan is probably doing about as well as they could.

There are two things I take away from this. First, there’s not much the Bank of Japan can do to stimulate their economy. It’s already running pretty well. Second, despite this, Japan is suffering from persistent deflation. Why? If their economy is productive and growing, deflation shouldn’t be any more of a problem for them than it is for us. Somehow, though, the very fact of a declining working-age population—and, since 2011, a declining overall population—seems to be driving deflation. This is very mysterious, especially since Japan’s deflation has persisted even in the face of massive BOJ efforts that, according to conventional economics, should have restored normal levels of inflation.

So why didn’t it? Is it really a consequence of demographic decline? Or is it something else?

December Japan Housing Starts Summary

December housing starts increased 3.9% to 78,406 units. For the first time in several months owner occupied single family housing led the gains with a 6.5% increase compared a 2.2% rise in rental units. The mansion condominium market gained 10.7%.

December total wooden starts improved 6.6% to 45,974 units. Post and beam housing increased 4.9% to 34,572 units. Pre-fab wooden starts fell 4.5% to 1,109 units and total pre-fab fell 4.1% to 12,179 units. Platform frame construction gained 13.9% to 10,293 units. Two by four starts broke down as follows: custom ordered single family units rose 11.9% to 2,716 units; rentals gained 16.8% to 6,422 units and built for sale speculative housing increased 1.6% to 1,122 units.

2 Japan Economy, Housing Starts & Lumber Shipments | Canada Wood Group

http://canadawood.org/wp-content/themes/canadawood/js/html5.js

Japan Economy & Housing Starts

Posted in: Japan

Japan Q1 GDP grew at an annualized 1.2% rate. February industrial production posted a solid growth of 4.7%. February unemployment held at 2.8%, its lowest level since the early 1990s. The consumer price index edged up 0.2% in February. Japan posted a large current account surplus of US $187 billion in February. Japan’s GDP growth forecast for 2017 is at 1.2%.

Japan Housing Starts Summary

Japanese Monthly Housing Starts Summary for January 2017

January total housing starts increased 12.8% to 76,491 units thanks primarily to a jump in rental housing. Rental housing saw growth of 12% compared to a decline of 0.2% in owner occupied housing. January results were boosted by a 38% surge in non-wood housing. Wooden housing gained 4.2% to 39,079 units. Of wooden housing, post and beam starts increased 4.9% to 29,714 units; wooden pre-fab declined 12.8% to 1,057 units, and 2×4 starts gained 4.0% to 8,308 units. Two by four owner occupied custom homes advanced 6.6% to 2,260 units, multi-family apartments increased 2.0% to 4,901 units and built for sale spec homes grew 6.6% to 1,129 units.

Japanese Monthly Housing Starts Summary for February 2017

February housing starts trailed 2.6% to finish at 70,912 units. Total wooden starts edged up 2.5% to 39,587 units, however the non-wood “mansion” condominium market fell 35.7% after experiencing a surge the month prior. Post and beam starts improved 3.4% to 30,023 units. Wooden pre-fab starts were flat at 1,057 units. Two by four starts declined 0.3% and broke down as follows: custom owner occupied declined 4.2% to 2,220 units, built for sale spec homes dropped 10.4% to 970 units and rentals improved 4.3% to 5,303 units.

Japanese Monthly Housing Starts Summary for March 2017

March total housing starts registered a faint increase of 0.2%, finishing at 75,887 units. Although owner occupied housing starts fell 3.6%, rentals posted an 11% gain. Rental housing recorded a 17th consecutive monthly gain. Total wood starts posted a small 0.9% gain thanks to strength in the post and beam segment. Post and beam starts increased 2.9% to 31,471 units. Wooden pre-fab starts slid 7.4% to 949 units. Two by four starts declined 4.6% to 9,116 units broken down as follows: custom built owner occupied fell 8.0% to 2,161 units; rentals gained 0.5% to 5,921 units and built for sale spec homes declined 5.0% to 1,011 units.

Vietnam’s economic challenges in 2017

VietNamNet Bridge – Vietnam economy will encounter more difficulties in 2017 than in 2016 amid global geopolitical changes and financial uncertainties, experts say.

Many economists have said that the 6.7 percent GDP growth rate target set by the government for 2017 was too ambitious as Vietnam only obtained 6.21 percent growth in 2016.

In the context of the increased budget deficit, fiscal policy would not help support growth. Therefore, it is highly possible that monetary policy loosening will be maintained.

However, some forecasts say it would be difficult to maintain the current stable interest rates. Some commercial banks have raised interest rates again, while bad debt, the exchange rate and higher requirements on capital adequacy ratio will affect the interest rate.

If interest rates go up, this will affect businesses’ demand for lending. This means the credit growth plan may be unattainable and loose monetary policy will not bring desired effects, affecting the GDP growth plan.

| Some forecasts say it would be difficult to maintain the current stable interest rates. Some commercial banks have raised interest rates again, while bad debt, the exchange rate and higher requirements on capital adequacy ratio will affect the interest rate. |