Courtesy BMI Research

Key Themes For 2017: Populism, Nationalism And Reflation

Global | Economy | Country Risk | Fri Dec 09, 2016

BMI View: 2017 is set to be another tumultuous year for the global economy, with the rise of populism and nationalism potentially triggering fundamental changes in the dynamics of trade, labour markets and ultimately, economic growth. Systemic risks abound amid a busy election calendar in Europe and the increasing fragility of the Chinese economy.

BMI expect the following key themes to play out globally in 2017:

- Economic Policy To Turn Inward

- Global Trade Framework Under Scrutiny

- End Of Austerity

- From Deflation To Reflation

- Commodity Exporters Struggle To Recover

- Eurosceptics Entrench Further, Keeping Systemic Risks High

- China’s Policy Constraints Tighten Rapidly – CNY At Risk Economic policy in developed states will be increasingly shaped by populist pressure and we expect a reorientation of economic policy towards promoting the interests of domestic labour. The result of this will be less free trade and increased restrictions on immigration. 2016 has laid the foundations for this trend change as the UK’s decision to leave the European Union and Donald Trump’s victory in the US presidential election have been interpreted as highlighting severe voter dissatisfaction with the economic status quo. The policy shift will be particularly acute in the US and UK, but we expect elements to be replicated in parts of Europe and to a lesser extent in Japan.

- Less Free Trade – The US will be the main driver of this trend. While we do not expect Trump to pursue some of his more extreme threats such as ramping up tariffs on all Chinese imports, we do expect a renegotiation of existing US trade deals including with China and the World Trade Organization (WTO). Meanwhile, Europe looks set to become more assertive in international trade relations by preventing a ‘soft Brexit’ and with German Chancellor Angela Merkel looking to take a harder line towards alleged dumping of cheap Chinese steel in Europe during her country’s presidency of the G20 in 2017.

- Economic Policy to Turn Inward Protectionism On The Rise -Largest Five Developed Markets – Number Of Protectionist Measures

| Note: Protectionist measures are those deemed ‘almost certainly discriminatory towards foreign commercial interests’. Largest five DM markets are: US, Japan, EU, Australia and Canada. Source: Global Trade Alert, BMI |

Immigration Rules To Tighten – In the US, Trump has promised much stronger border enforcement and tougher immigration policy, which we expect a Republican dominated Congress will help him at least partially deliver. In the UK, BMI expect that UK immigration policy will become more restrictive as the country prepares to leave the EU. In Europe, the ongoing migrant crisis means that the Schengen zone is at critical risk of collapse.

Global Trade Framework Under Scrutiny

In 2016, the outlook for the global trade framework took a turn toward the more insular. Donald Trump’s election as US president, following a campaign that bombastically criticised the US’s ‘disastrous’ trade deals, confirmed a sea-change in the outlook for global free trade. In 2017, this trend toward delaying and even potentially dismantling trade deals will continue. The first signs of this may emerge early in the year, as Trump’s inauguration on January 20 could be swiftly followed by the new administration confirming that it will not approve the ratification of TPP, and stating its intention to renegotiate the North American Free Trade Agreement (NAFTA). BMI also expect harsh words for China’s trade practices from the US Treasury, although an all-out trade war with harsh across-the-board tariffs is unlikely.

BMI expect the WTO to face its biggest challenge since at least the turn of the 21 st century, when China acceded to the group. Trump’s economic advisors have sharply criticised the WTO for failing to effectively arbitrate trade disputes, and for allowing members to engage in unfair activities such as bankrolling their export industries via state banks (e.g. Chinese steelmakers). While previous presidents have taken trade disputes with China to the WTO, Trump would have the deal renegotiated, under threat of having the US leave altogether. They could even see other large economies, such as Japan and the EU, join in with the US in complaints about Chinese trade practices. A global trade war is suddenly not a far-fetched possibility, though again, this is not our base case.

As much as these developments will pose threats, the global trade framework is far from dead, and there are also opportunities to be seized should political circumstances allow. NAFTA is arguably overdue a renegotiation, having been conceived in the early 1990s, with dated provisions regarding technology and the internet, agriculture, and energy. China is taking advantage of the lapse in US trade leadership by promoting its TPP rival in Asia, the Regional Comprehensive Economic Partnership (RCEP). While the US-EU TTIP trade deal appears to be dead after three years of talks, the EU and Japan are due to sign a major bilateral trade deal, which has gained urgency on the part of Japan due to the collapse of TPP. It is even conceivable that the TPP gets revived in some renegotiated form. Trump, for his part, even while denigrating multilateral trade deals, has favoured making bilateral pacts, suggesting that the US retains the potential to expand its trading horizons even if it holds back on the likes of TPP.

End Of Austerity

An ongoing trend, particularly among developed markets, is a shift away from reliance on monetary policy and toward fiscal policy when seeking to boost growth. Reasons include accommodative monetary policy having reached the limits of its effectiveness, austere fiscal policy having failed to reduce debt burdens relative to GDP and an element of ‘austerity fatigue’ among electorates. As a result, governments have begun loosening the fiscal reins and BMI believe that ‘peak austerity’ has been reached. While they do not expect outright fiscal expansion, several key developed states are using targeted tax cuts to boost growth, and are moving away from previous targets for fiscal consolidation. A common theme is infrastructure being seen as an attractive sector to focus on, given that it boosts short- and arguably long-term growth and creates many jobs. However, they have not fully incorporated proposed infrastructure programs in China, the EU, Japan, the UK and the US into our forecasts given our skepticism that they will be fully implemented.

Fiscal Austerity Has Peaked -Government Final Consumption, pp Contribution To Real GDP Growth

f = BMI forecast. Source: National Sources/BMI

United States – Most significantly, there has been a major shift in the policy outlook in the US following the election of Donald Trump to the presidency along with full Republican control of Congress. BMI expect corporate and income tax cuts to be complemented by fiscal stimulus centred on infrastructure. However, opposition from fiscal conservatives in Congress will prevent a surge in deficit spending.

EU – Political pressures are a key driving force behind the move away from fiscal austerity in the EU given that there are many key elections approaching. Meanwhile the European Commission has already adopted a more lenient stance, highlighted by its decision not to sanction either Spain or Portugal in 2016 for failing to meet budget targets. All that said, they do not expect outright fiscal expansion in the EU as more fiscally hawkish northern European countries hold significant sway over policy at the EU level, including Germany, Denmark, Sweden and the Netherlands.

Japan – Policymakers are increasingly looking to fiscal policy to boost growth, following many years of stagnant economic activity despite ultra-low interest rates. Since July 2016, the finance ministry has shelved a proposed consumption tax hike until 2019, hinted at cutting the corporate tax rate, and also announced a JPY4.5trn (USD40bn, or roughly 1% of GDP) stimulus package aimed largely at boosting infrastructure and social welfare.

From Deflation To Reflation

Their global inflation forecast for 2017 is 2.9%, which would be the highest since 2013 and a major rise from a six-year low of 2.1% in 2016, and the risks lie to the upside. This ‘deflation to reflation’ shift can be observed through a variety of important metrics. Inflation ‘surprises’ have risen to four-year highs across both developed and emerging markets. US wages and core inflation are picking up alongside a tightening labour market, and even eurozone headline (though not core) prices have begun to pick up after a prolonged deflation scare. Chinese producer prices rose year-on-year in September to November, following contractions that began in March 2012. And bond yield curves are steepening across much of the world, in expectation that stronger growth and higher inflation lie ahead.

Commodity prices, particularly oil, will be an increasingly positive driver of global inflation in 2017. The severity of the declines in oil and grain prices over late 2015 means that both commodity groups will post consistently positive y-o-y price increases in the coming months. Additionally, the ‘end of austerity’ theme implies that fiscal policy will expand and take some of the pressure off of central banks, and in the process, help fuel reflationary expectations in 2017 (witness the rise in inflation expectations following the US elections, on the back of Trump-backed infrastructure stimulus hopes).

f = BMI forecast. Source: BMI

The transition from deflationary pressures in 2016 is likely to be seen as a positive, as outright deflation will have been avoided. But this transition also carries risks of not coming off quite as smoothly as many might hope. In the latter months of 2016, inflation expectations rose significantly, but in some cases may still be too low, for instance in the eurozone and Japan, and a further rise could complicate monetary policymaking. Reflation could also come about via negative supply-side shocks, for instance a disruption in global oil output, or a trade war, either of which would bring higher prices and damage the economic growth outlook.

Commodity Exporters Struggle To Recover

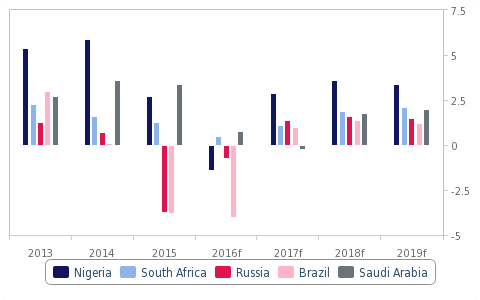

Several large commodity exporting economies will struggle to recover in 2017. Although BMI expect commodity prices to be higher on average in 2017 than in 2016, the gains will be fairly marginal, given that the stimulus effect stemming from China will wane, and metals in particular have already rallied significantly on the back of anticipated US infrastructure developments. This being the case, commodity exporters will gain only limited tailwinds from rising prices.

Bouncing Back, But Not To Previous Growth Levels- Select Commodity Exporters – Real GDP Growth, %

Meanwhile, various idiosyncratic challenges will weigh on growth in the commodity exporters. Brazil will struggle to cope with a large output gap and high levels of debt. In South Africa, high structural unemployment, weak mining sector activity and heightened political risk will stymie economic activity. Nigeria faces delays to government-supported infrastructure and will continue to suffer from negative investor sentiment given sluggish reform momentum and shortages of foreign exchange liquidity. Saudi Arabia faces an outright recession in 2017 as non-oil sector growth continues to slow amid fiscal consolidation, and oil production declines to meet OPEC targets.

Investor sentiment towards Russia is improving given a brightening outlook for foreign relations. The election of Donald Trump as US president, as well as the probable election of Francois Fillon as French president in 2017, will usher in a much more amicable stance towards Russia among key NATO members. This will in turn diminish the political cohesion necessary to maintain sanctions. However, BMI do not believe sanctions have acted as a major drag on growth, and as such the lifting of sanctions will not be a major boon. Growth will remain subdued in 2017, weighed down primarily by a lack of reform and the overbearing role of the state in the economy.

Euro sceptics Entrench Further, Keeping Systemic Risks High

The trend of falling support for pro-EU, mainstream political parties across the union will become even more firmly entrenched in 2017 as eurosceptic, populist and anti-establishment parties continue to make gains in terms of popular support and actual seats in national legislatures. This will be evident in France, where the Front National’s Marine Le Pen is poised to secure the party’s largest ever vote share in the April presidential election, in the Netherlands, where the far-right Freedom Party will likely emerge with the first or second most seats in parliament following the March general election, and in Germany, where Alternative for Germany will enter parliament for the first time and likely emerge as the main opposition party after the October (at the latest) general election. Italy is also likely to have another general election at some stage in 2017 with the eurosceptic 5-Star Movement polling neck and neck with the centre-left Democratic Party.

While it is unlikely that any of these parties will enter government or take executive power, their entrenchment into the political landscape will have crucial implications for reforms and EU integration, and by extension, potential growth and systemic risks across the bloc. This is especially the case for the eurozone. Deeper integration, particularly in the areas of banking and fiscal policy, is crucial in making the eurozone a properly functioning currency union. However, the ability of mainstream parties to pursue such integration will be significantly diminished by the need to counter the rising popularity of eurosceptic and anti-establishment forces. Furthermore, rising anti-EU sentiment is also evident in the governments of EU economies such as Poland and Hungary, who would be unlikely to sign off on major integration initiatives. Growth-stifling debt burdens and large variations in economic outcomes across the bloc will thus remain prominent, keeping breakup risks at the forefront and the burden of keeping the eurozone together remaining firmly on the ECB’s shoulders. Fiscal constraints and a lack of reform momentum are key reasons why they expect the ECB to keep monetary policy ultra-loose for an extended period.

Note: France refers to the 2012 and 2017 presidential elections; Germany refers to the 2013 and 2017 federal elections; Netherlands refers to the 2012 and 2017 general elections; Italy refers to the 2013 and 2018 (at the latest) general elections. Source: China’s Policy Constraints Tighten Rapidly – CNY At Risk

BMI expect constraints on policymakers to tighten in China, as the economic balancing act will be increasingly tested as free market forces play a larger role in the economy. The suppression of market forces with respect to currency, interest rates, and default risk has allowed policymakers to enact stimulus policies with few obstacles. However, the ability to manage the currency and domestic interest rates simultaneously amid an increasingly open financial account is now waning.

Rising Debt A Concern- China – Non Financial Corporate Debt, % of GDP

| BMI, BIS |

In particular, ongoing currency weakness and the threat posed by US trade protection could unravel the country’s increasingly fragile credit boom. For instance, a cooling residential property market will put the People’s Bank of China (PBoC) in the difficult position of having to lower interest rates to prop up the credit bubble at a time of intensifying capital outflows in 2017. If the Chinese yuan depreciation starts to become disorderly, currency intervention by the PBoC would weigh on domestic money supply and hence economic growth. This is particularly relevant given US President-elect Trump’s protectionist rhetoric and the resulting renegotiation of the US’s trade relationship with China that will begin in 2017.

While BMIs core view is that a trade war will be avoided, we expect headwinds to China’s export sector and an associated drag on economic growth and the currency. Pressure on the CNY will be particularly acute as the currency remains fundamentally overvalued in real effective exchange rate (REER) terms and it will remain vulnerable to capital outflows as real interest rate differentials move against the currency amid a slowing economy and rising US bond yields. they see the yuan ending 2017 at CNY7.10/USD with risks skewed towards greater depreciation.

China’s renminbi hits 8-year low

From Trump win to capital outflows — factors behind currency’s moves in charts

by: Gabriel Wildau in Shanghai and Jennifer Hughes in Hong Kong Financial Times

China’s renminbi traded near an eight-year low against the US dollar on Thursday, as the election of Donald Trump intensified longstanding depreciation pressure.

The Chinese currency has weakened for seven of the eight trading days to Wednesday and is down 5.5 per cent in 2016 — on pace for its worst year since authorities depegged it from the dollar in 2005.

Mr Trump slammed China during the campaign for artificially weakening its exchange rate to boost Chinese exports, blaming currency “manipulation” for the US trade deficit with China. But experts say that while China actively weakened the renminbi in years past, the recent decline is driven by market forces — and government intervention is focused on curbing depreciation rather than encouraging it.

Analysts have gradually downgraded their forecasts for the dollar’s value against the renminbi this year. Median forecasts for year-end stand at Rmb6.8 compared with Rmb6.68 six months ago. Australia and New Zealand Banking Group (ANZ) on Tuesday revised its forecast to 6.9 by year end and 7.1 by the end of 2017. The renminbi was trading at 6.87 at midday on Thursday.

So what are the factors pressuring the renminbi and how is the Chinese government responding?

Strong dollar

Expectations of an interest-rate rise by the Federal Reserve in December and, more recently, the election of Donald Trump, pushed a popular measure of the dollar to a 13-year high on Wednesday. Investors expect Mr Trump to usher in tighter monetary policy, bigger fiscal deficits and higher inflation. The renminbi has closely tracked the dollar index in recent months.

Capital outflows

Capital outflows surged last August year when China unexpectedly changed the way it guides the renminbi’s value, allowing the currency greater freedom to depreciate. But outflows moderated in the middle of 2016 as the economy stabilised and the timing of the Fed’s next rate rise was pushed back. Now outflows are picking up again.

Amid a flurry of Chinese outbound investment deals, net outflows from foreign direct investment hit an all-time high of $31bn in the third quarter, according to balance of payments data.

In addition, “hot money” — financial capital flows not linked to trade or FDI — hit $176bn in the third quarter, the most since the fourth quarter of 2015. Hot money includes portfolio investments in stocks, bonds and insurance as well as trade credit and other cross-border lending.

Government intervention

Despite rhetoric during the US presidential campaign accusing China of deliberately weakening its currency, the People’s Bank of China has done exactly the opposite over the past two years. The PBoC has sold dollars from its foreign exchange in order to push back against market forces putting pressure on the renminbi and to prevent excessive depreciation.

As downward pressure has increased in recent weeks, China has stepped up intervention to support the renminbi. The PBoC spent about Rmb605bn ($88bn) in September and October to prop up the redback, according to Financial Times estimates based on central bank data. That is the biggest two-month intervention since the Rmb1.4tn spent in December and January, at the height of global concern about China’s economic slowdown. The country’s foreign exchange reserves fell to $3.12tn at the end of October, their lowest level since March 2011.

Intervention explains why, despite losses, the renminbi has held up better than other emerging market currencies since Mr Trump’s election. The renminbi is down 1.2 per cent, compared with losses of 4 per cent for the Malaysian ringgit and 3.3 per cent for the Korean won. The worst-hit by Mr Trump’s victory are the Mexican peso and the South African rand, off 9 per cent and 7.7 per cent against the dollar, respectively.

Home economics: China’s growth

Homes are where the economy’s heart is. Much of the recent gloom about China was based on the view that the property market, which accounts for about a quarter of GDP, was past its peak. But 2016 has brought a big revival. Third-quarter data today showed 6.7% year-on-year growth. A big jump in property sales has fed through to strong industrial output and consumption (all the furniture and gadgets needed to fill homes). This should be good news for the global economy, giving a much-needed boost to beleaguered commodity exporters. But can the rebound last? With housing prices in major cities up more than 30% over the past year, the market is looking frothy; dozens of local governments have enacted measures this month to cool demand. Before long, property will go back to being a drag on Chinese growth. Fordaq

Chinese city bans property developers from borrowing to buy land

Nanjing first to cut of access to banking system to temper overheating property market

Nanjing, where housing prices in September were up 40% over the past year

by: Yuan Yang and Tom Mitchell in Beijing

Officials in one of China’s hottest property markets have banned developers from borrowing money to buy land, as local governments embrace increasingly drastic measures to curb soaring home prices.

Prices of new residential properties in Nanjing were up 40 per cent year on year in September, in line with increases in other big cities such as Beijing and Shanghai.

Over recent months, local governments have tried to cool residential property prices by making it more difficult for people to buy homes. The unprecedented decision by officials in Nanjing to cut off developers’ access to the banking system for land purchases highlights how local governments’ policy focus is shifting to real estate companies and their often murky funding sources.

Highly leveraged developers, colloquially known as “land kings”, have driven land prices to record levels in many Chinese cities over the past year. Local governments were initially reluctant to rein in the land kings, as land auctions are an important part of their revenue base.

In September, however, the Chinese government and central bank ordered local governments to cool overheated property markets.

“Bidders must use their own funds [at auctions],” Nanjing’s land bureau said in a notice. The notice specifically banned developers from bidding with funds from banks, trust companies and insurers. They were also banned from using money raised either on capital markets or through the issuance of wealth management products and “other unregulated funds”.

Nanjing was due on Thursday to hold its first land auction since late September, when central government directives to cool overheated markets began to take effect.

Last month China’s securities and banking regulators began to restrict real estate developers’ ability to issue new shares and bonds.

“All the relevant [national] regulators and government departments have intervened to curb developers’ financing,” said Jonas Short at NSBO, a policy research group. “It’s an example of the concerted action that you get when [Beijing] is convinced something must be done.”

Corporate bond sales by real estate developers have come to a complete halt this month while their issuance of trust products fell by a quarter in October compared with September. Trust products bundle corporate loans and other assets that are sold on to a variety of investors including bank depositors.

Thomas Gatley at Gavekal Dragonomics said the immediate impact on many developers would be limited. “Property developers are cash-rich right now from excellent sales this year,” said Mr. Gatley. “Only the smaller ones will be affected. More broadly, it is high demand for housing in China’s top cities that drives both land and house price growth.”

According to the Centre for Finance and Policy at the Massachusetts Institute of Technology, roughly 40 per cent of all provincial government debt in China is backed by funds from land sales. But Nanjing’s economy is doing well, allowing its government to forgo some lost revenue from land sales.

Russia close to issuing first renminbi bond Premium

Beijing backs deal that helps to tighten relations and bypass western sanctions

© Bloomberg

December 7, 2016

Russia and China are close to another milestone of co-operation with the placement of an offshore renminbi bond in Russia by the Russian finance ministry that would open new funding options for the country’s issuers and bring Chinese investors one step closer to Russia’s equity market.

People involved say preparations for the issue are nearing completion and it should happen early next year — despite volatility in global bond and equity markets after the UK’s vote to leave the EU in June and Donald Trump’s victory in the US presidential election last month.

Under the proposal, first floated in December last year, the Russian finance ministry would issue Rmb6bn ($1bn equivalent) of bonds with multiple maturities to be listed on the Moscow Exchange (MOEX). This would establish benchmarks for a new funding option for large parts of Russia’s economy shut out of foreign-currency bond markets by western sanctions and give China a central role in making this possible.

“Despite the uptick in global interest rate levels since the US elections and the looming US Fed funds rate hike in December, the interest for this deal from the Chinese mainland investment banks is still very high,” said Andrei Akopian, managing partner at Russian-Chinese advisory business Caderus Capital. Caderus was appointed MOEX’s official representative for China in February 2016.

In a joint statement following a meeting of Russia’s prime minister Dmitry Medvedev and his Chinese counterpart Li Keqiang in early November, Beijing underlined its support for the issue.

Mr. Akopian said this was “the last missing piece of the puzzle” to obtain the necessary regulatory clearance for the issue and towards making Moscow an offshore centre for the renminbi.

The Chinese-language statement said the aim of the initiative was “to increase co-operation between the [two countries’] banks and between financial institutions in trade finance, in capital raising for projects between the two countries, in insurance and in other areas, and to . . . promote the use of the countries’ domestic currencies in settlement of bilateral trade and investment”.

Mr. Akopian said a number of Russian companies were lining up to issue renminbi bonds in Russia and help establish what he called a “Baikal bond” market.

This would not be the first offshore renminbi issuance by a foreign government, which was led by the UK in 2014 but — if sold as planned — it would be the largest to date (see table) and would mark a significant step in Chinese-Russian relations at a time when the US appears ready to give up some of its postwar lead in international affairs.

| Non-Chinese sovereign and local authority renminbi issuance | ||||

| Date | Issuer | Value, Rmb | Coupon, % | Yrs to maturity |

| Oct 14, 2014 | United Kingdom | 3bn | 2.7 | 3 |

| Oct 28, 2014 | British Columbia | 3bn | 2.9 | 2 |

| Jun 24, 205 | Mongolia | 1bn | 7.5 | 3 |

| Dec 15, 2015 | Republic of Korea | 3bn | 3.0 | 3 |

| Jan 21, 2016 | British Columbia | 3bn | 3.0 | 3 |

| Apr 14, 2016 | Hungary | 1bn | 6.3 | 3 |

| Aug 25, 2016 | Republic of Poland | 3bn | 3.4 | 3 |

| Source: Dealogic | ||||

Significantly, the communiqué talks of a need to “reform the international financial system” and “raise the representation and the right to a voice of emerging and developing countries in the global system of economic governance”.

For Russia, the bond could also help attract much sought-after Chinese investors to Russian equities and, ultimately, achieve the goal of listing equities of Chinese companies in Moscow.

In September, Caderus reached agreement with BCS Global Markets, the largest securities broker on the MOEX, in a bid to bolster cross-border investment by attracting Chinese private and institutional money to the Russian market through BCS’s investment platform.

Today, private Chinese investors with money outside China typically invest through Russian brokers, while institutional investors typically prefer Russian global depositary receipts (GDRs) and American depositary receipts (ADRs) listed in London or New York.

Rmb6bn ($1bn equivalent) of bonds with multiple maturities to be listed on the Moscow Exchange

At the end of September, only seven Chinese asset managers held Russian blue-chip equities, with a combined value of just $8.78m, according to Thomson Reuters data compiled by Caderus. This makes up a mere 0.017 per cent of the seven managers’ combined assets under management of $50.6bn — suggesting significant room for further investment.

Of the few such Chinese investments to date, most are in Russia’s oil and gas majors, with some stakes in metals and mining businesses, retailer Magnit and the country’s largest banks Sberbank and VTB, according to data from March 2016.

China Investment Corporation (CIC), China’s biggest sovereign wealth fund, has led some strategic investments in Russia’s equity markets, including equity issuance in VTB and MOEX, although CIC sold its stake in MOEX in January this year.

Vladimir Potapov, chief executive at VTB Capital Investment Management, Russia’s largest asset manager, said he was keen to attract further Chinese investors to Russian equity markets.

“The China story is now coming together both from the top down and the bottom up,” he said, suggesting that co-operation between Russia and China is happening at government and business level.

Stefanie Linhardt is Europe editor at The Banker.

© Bloomberg

Abe calls for wage rises to boost Japanese economy

Prime minister’s demand on incomes is attempt to lift consumption and boost inflation

by: Robin Harding in Tokyo Financial Times

Shinzo Abe has demanded that companies raise wages next year by at least as much in 2016, despite a fall in profits, as he tries to keep Japan’s economy on track.

In a meeting on Wednesday of the prime minister’s labour reform working group, Mr Abe told business leaders that he “expects wage rises of at least the level of this spring”, according to his office.

The prime minister’s demand signals that he still hopes to influence next year’s private sector wage negotiations as part of an effort to boost worker incomes, their consumption and thus inflation.

In a sign he may achieve this goal, Sadayuki Sakakibara, chairman of the Keidanren business group, replied: “We want to maintain the momentum of wage rises.”

Efforts to push up pay in the annual “spring offensive” negotiations between management and unions have become a big part of the prime minister’s “Abenomics” stimulus over the past three years.

In Japan’s system, a national negotiation — which Mr Abe has tried hard to influence — sets an overall goal for wage rises. Companies are free to ignore it, but large corporations in particular often try to respect the results.

Sluggish wage growth, and the resulting hit to consumption, is regarded as one of the main reasons Japan has remained mired in deflation for a generation. Mr Abe has therefore worked at persuading companies to raise pay.

In 2014 and 2015 his efforts succeeded, but this year the pace of wage hikes slowed for the first time since Mr Abe came to power, with an average rise of 2.14 per cent compared with 2.38 per cent a year earlier.

During 2015, companies were hit by a strengthening of the yen, which went from ¥120 to ¥100 against the US dollar — hitting their profits. According to the Bank of Japan’s latest Tankan survey of business sentiment, they expect current profits to fall 11.8 per cent this fiscal year.

Along with a dip back into deflation for consumer prices — dragged down by the stronger yen and the weakness of commodities such as oil — weaker profits mean Mr Abe is fighting a rearguard action to keep wages and incomes moving upwards.

The prime minister pointed out that oil prices are now above their trough early in 2016. “By next spring, I expect the rise in oil prices to be pushing up consumer prices. I’d like a debate on wage rises that considers the expected rate of inflation,” he said.

He also called on large companies to improve terms for their subcontractors. Previous attempts to push up wages have not spread beyond a small number of large corporations, one of the main reasons for their limited effect.

“To prepare an environment for wage hikes at smaller companies, I’d like you to tackle properly improvement of trading conditions for subcontractors and SMEs,” he said.

Japan economy beats forecasts with 2.2% GDP growth

Third-quarter data suggest renewed momentum and ease pressure on BoJ to boost stimulus

A rollercoaster beside Yokohama’s Landmark Tower. Japan’s exports have overcome the surging yen to help GDP growth soar © Bloomberg

November 14, 2016

by: Robin Harding in Tokyo Financial Times

Japan’s economy grew by more than 2 per cent in the third quarter, much faster than expected, as the country’s exporters overcame the strength of the yen.

Although Japan’s initial gross domestic product data are notoriously unreliable, the figure of 2.2 per cent was much stronger than analyst forecasts of a 0.8 per cent rise, suggesting the economy has regained some momentum after a long lull.

The stronger growth is a boost to Shinzo Abe, prime minister, and reduces pressure on the Bank of Japan to launch further monetary easing.

“The bigger picture is that spare capacity is shrinking gradually: gross domestic product expanded by 0.9 per cent over the past 12 months, which is above potential growth,” said Marcel Thieliant, analyst at Capital Economics in Singapore.

“We estimate that the output gap was the smallest last quarter since 2014’s sales tax hike and consistent with consumer prices rising by around 1 per cent per annum.”

Almost all of the surge in growth was down to trade, which contributed 1.8 percentage points to the total. Exports rose and imports fell. “Strong exports are consistent with better external demand, especially in Asia,” said Masamichi Adachi, economist at JPMorgan in Tokyo. “Weaker imports is consistent with sluggish domestic demand.”

The picture at home was subdued, with consumption adding only 0.1 percentage points to growth. Business investment was flat.

That adds to recent evidence that Japanese industry is picking up as the US recovers and China goes through another round of credit growth. But it suggests Japan is still failing to create a self-sustaining cycle of stronger growth leading to higher profits, higher wages and thus more demand at home.

Although boosting consumption remains a problem, the outlook for 2017 is fairly positive. The Bank of Japan added to its economic stimulus in September by capping 10-year bond yields at 0 per cent and promising to overshoot its inflation target of 2 per cent. Mr Abe’s government is also launching a fresh fiscal stimulus.

“Extremely powerful economic stimulus measures are being implemented, both on the monetary and fiscal side,” said Haruhiko Kuroda, BoJ governor, in a speech on Monday.

The yen gained against the US dollar in the third quarter, but has lost ground recently as markets anticipate a US rate rise following the election of Donald Trump in the US.

But while real growth was robust, nominal growth — which does not adjust for price changes — was significantly weaker at 0.8 per cent, reflecting Japan’s renewed dip into deflation. That in turn has led to weak wage demands, removing the spending power needed for higher consumption.

Japan is in the process of revamping its GDP data because of doubts about its accuracy, partly due to falling response rates to surveys. The initial estimate is particularly imprecise because it relies on limited data.

The Topix stock index closed up 22 points at 1,400, and the yen was 1.2 per cent weaker at ¥107.9 against the dollar.

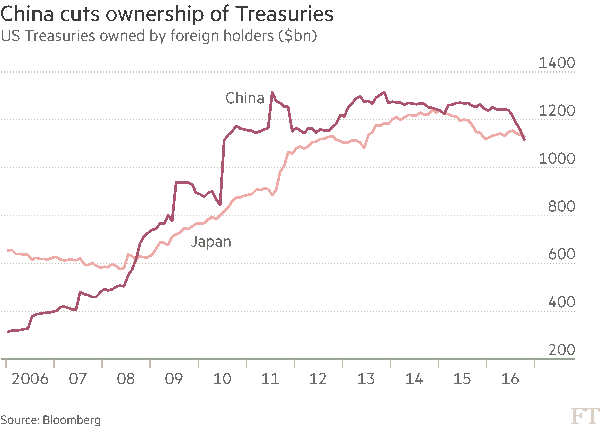

China cedes status as largest US creditor to Japan

Tokyo top US Treasuries holder as Beijing depletes forex reserves to support renminbi

Read next

US adds new front in trade battle with China

© Bloomberg

by: Tom Mitchell, Joe Rennison and Eric Platt

China has ceded its status as America’s largest creditor nation to Japan after spending a large portion of its foreign exchange reserves to defend the renminbi.

Beijing’s ownership of US Treasuries fell by $41.3bn to $1.12tn in October, according to data from the US Treasury released on Thursday — the sixth straight month of decline. Japan’s holdings fell by $4.5bn to $1.13tn for the same period.

Thomas Simons, a money market economist with Jefferies who characterised the Chinese selling as “stunning”, noted that data suggested Beijing’s holdings fell by an even larger $67.1bn if Belgian sales were included in the numbers. “This is significant because it is widely speculated that China executes trades with Treasuries held in custody in Belgium,” he said.

China’s foreign exchange holdings, much of which are invested in US Treasuries, have fallen about a quarter since early 2014 to just over $3tn. The decline has been driven partly by central bank selling of dollars to support the renminbi, which has fallen more than 15 per cent against the US currency over the same period.

The fall in Treasuries holdings is part of a larger campaign by Beijing to stem capital outflows. China has also recently introduced curbs on Chinese companies’ overseas acquisitions and dividend remittances by foreign investors.

The holdings data predate the US presidential election result and subsequent sell-off in Treasury markets as investors braced for faster US growth under president-elect Donald Trump. His surprise victory has sent the US dollar soaring, adding to the challenges faced by emerging market economies.

“This pattern is unlikely to be reversed in the near future, especially with US and Chinese economic fortunes and monetary policy stances continuing to diverge,” said Eswar Prasad, economics professor at Cornell University and former IMF director for China. “The days of China providing abundant and cheap financing for US budget and current account deficits through the purchases of Treasury securities may have come to an end.”

China and Japan account for 37 per cent of the total $6tn of holdings tracked by the Treasury and Federal Reserve.

Total major foreign holdings of Treasuries fell by $116bn to $6tn in October, which accompanied a steep sell-off in US sovereign bonds at the time. Yields on the benchmark 10-year Treasury climbed 23 basis points in October and hit a high of 1.877 per cent.

Trump and China: the year of the chicken Premium

Any spat risks hurting Taiwan businesses — and US interests as badly

© AFP

Bottom of Form

December 12, 2016

Donald Trump reckons himself a master of the high-stakes gamble. Over the weekend, the US president-elect questioned whether his administration would respect the “One China” policy, by which the US acknowledges just one legitimate Chinese government. This prompted a robust response from Beijing. Any spat risks hurting Taiwan businesses — and US interests as badly.

Until Mr Trump’s victory in November, China’s government was accepted as the one that rules on the mainland. Earlier this month the president-elect broke with protocol by accepting a phone call from Tsai Ing-wen, the president of Taiwan. On that occasion, China reacted with restraint, protesting directly to Washington. Like Mr Trump’s posturing, Beijing’s reaction has escalated. On Monday, China hit back, its foreign ministry denouncing Trump’s comments.

US dependence on Taiwanese manufacturing runs deep. Over the years, as technology companies such as Intel and Dell have invested less in production, they have outsourced to Taiwanese manufacturers. Nor does their dependence stop at Taiwan’s shores. As relations between China and its “renegade province” have thawed, Taiwanese companies’ mainland-based facilities have grown. As a result Apple, dependent on the semiconductor maker TSMC and manufacturer Foxconn (listed in Taiwan as Hon Hai), relies on mainland China too. At end of 2015 three quarters of Foxconn’s fixed assets were across the straits.

Disrupting these operations would not be hard for China. Failing that, its government is a past master at mobilising public opinion against foreign companies, for misdeeds real or perceived. It is an unwise man who provokes such mobilisation.

Perhaps Mr Trump believes Taiwan is expendable in his get-tough stance on China. Alternatively, he may think disrupting companies such as Foxconn will bring manufacturing home. In this game of chicken between China and Mr Trump, it is US companies that risk being run over.

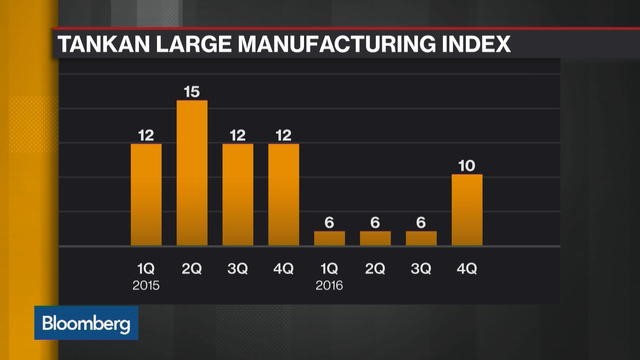

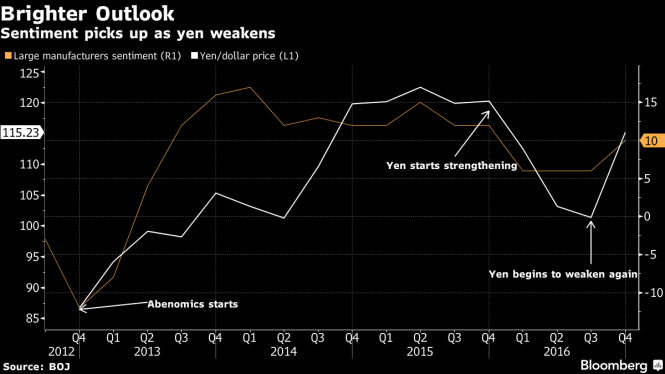

Japan Corporate Sentiment Rises for 1st Time in Six Quarters

by Toru Fujioka More stories by Toru Fujioka

December 13, 2016 5:01 PM December 13, 2016 5:49 PM

What Tankan Survey Signals About Japan’s Economy

Confidence among Japan’s large manufacturers improved for the first time since June last year as the fall in the yen improved prospects for company earnings.

Key Points

Sentiment among large manufacturers rose to 10 from 6 three months ago (est. 10), according to the Tankan survey released by the Bank of Japan Wednesday.

The outlook among the manufacturers increased to 8 from 6 (est. 9).

Sentiment among large non-manufacturers was unchanged at 18 (est 19).

Large companies across all industries plan to raise business investment by 5.5 percent for the year ending in March (est. 6.1%).

Big Picture

Improving sentiment among big Japanese manufacturers strengthens the view that the Bank of Japan will be in no rush to add stimulus. The yen weakened against the dollar last month by the most since 1995. A moderate recovery is underway, with the economy growing for the first nine months of the year. However, weak wage gains have capped inflationary pressures.

Economist Takeaways

“The improvement in confidence reflect a recovery in overseas demand, which bodes well for Japan’s economy. Demand in Asia, including China, is rebounding,” said Kohei Okazaki, an economist at Nomura Securities Co. in Tokyo.

“The recent weakening yen may be reflected in companies’ forecast in the next survey and they may upgrade their capital spending plans next time,” Okazaki said.

There is “plenty of room for upside surprises” as the forecast for the currency didn’t reflect the recent weaker yen, said Marcel Thieliant at Capital Economics in Hong Kong.

Details

Large manufacturers expect the yen to be at 104.90 per dollar for the year ending in March, stronger than the 107.92 forecast three months ago. The currency was at 115.08 at 9:26 a.m. in Tokyo, having lost almost 11 percent in the past three months.

The BOJ surveyed 10,791 companies from Nov. 14 to Dec. 13.

Modi seeks to rally public behind India’s currency crackdown

PM urges citizens to withstand hardships to create ‘corruption-free’ country

Read next

India: Narendra Modi’s bonfire of the rupees

© Reuters

November 14, 2016

by: Amy Kazmin in New Delhi Financial Times

Indian Prime Minister Narendra Modi sought on Monday to rally public support for his draconian decision to scrap most of the country’s existing banknotes, while the government urged citizens struggling to obtain cash not to panic.

Speaking at large political rally, Mr Modi said his decision to scrap Rs500 and Rs1,000 notes was a decisive blow against hoarders of illicit cash. He urged citizens to withstand their temporary hardships with grace in order to help create a “corruption-free India”.

“Poor people are sleeping peacefully; it is the rich who are running pillar to post to buy sleeping pills,” he told the crowd in Uttar Pradesh, which is heading for critical state legislative assembly elections in the next few months.

“I had no other option to crack down on black money,” Mr Modi said. “I want to assure you that your inconveniences will not go in vain.”

The move — which affects about $223bn worth of notes, nearly 86 per cent of the rupees in circulation — has shaken India’s cash-driven economy, damping retail sales and causing mayhem at banks, where old notes are being exchanged for limited supplies of new currency.

Cash crisis for Delhi traders

Opposition parties have fiercely criticised Mr. Modi’s administration for the difficulties facing the public, with long queues forming at banks and automated teller machines, and some people camping out overnight near cashpoints hoping to secure money once they are refilled.

India’s banknotes withdrawal

The government has called for calm amid major bottlenecks that have impeded its effort to distribute the new currency rapidly.

The new banknotes are slightly smaller in size than the old notes and the nation’s roughly 200,000 ATMs need replacement parts in order to handle them. The government set up a task force on Monday to supervise the process of recalibrating the machines.

“Enough cash is available and there is absolutely no reason for the public to feel any kind of panic,” Shaktikanta Das, secretary of economic affairs in the finance ministry, told reporters on Monday. “In the days to come, the supply of money through various channels will be improved.”

New Delhi has extended the period during which old notes can be used at petrol stations, government hospitals and to pay taxes and utility bills until November 24. Limits on withdrawals from banks or ATMs have also been raised slightly.

But Mr Modi’s surprise move — which came at the peak of India’s wedding season, normally a period of frenetic spending — is seen as a major blow to consumption, which has been a primary driver of the country’s economic growth.

Sales of consumer durables, for example, grew 17 per cent year on year in September and 7.6 per cent in the first half of the current financial year, according to recent data. But consumption, along with the property and construction sectors, are expected to be major casualties of the squeeze on cash.

“It’s clearly going to be a big impact in the short term, and it’s going to be particularly big in the property market,” said Chris Wood, managing director and equity strategist at CLSA. “The key question is how long does it last, and that’s going to be very much caught up in the technical issue of can they replace this currency quickly.”

He added: “If it’s just a two week glitch, it’s not a disaster. But if it’s a two-month glitch, it is.”

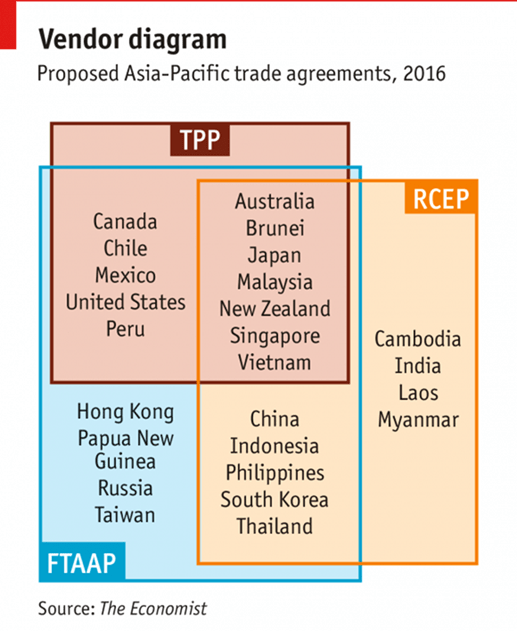

TPP vs. RCEP: Trade and the tussle for regional influence in Asia

21 Aug. 2015 /

After the United States’ recent diplomatic disaster of trying to prevent general adherence to China’s Asian Infrastructure Investment Bank (AIIB), US policy makers have been under pressure to strengthen their presence in Asia on the trade front: By concluding the Trans-Pacific Partnership (TPP), a potentially historic trade agreement linking the US, Japan and ten other countries, China would see its goal of reducing Washington’s presence in its neighborhood severely thwarted. Furthermore, the TPP would connect the United States to the economic center of the 21st century, one of the fastest-growing regions of the world, and cement its relationship to Japan, its key ally. It would be the first real manifestation of Obama’s pivot to Asia, which so far consisted of mere rhetoric.

China, which is excluded from the countries negotiating the TPP, has responded by promoting the Regional Comprehensive Economic Partnership (RCEP), which excludes the United States, and which would promote rapprochement between Beijing and Tokyo. The tussle for regional influence between the United States and China has thus also taken hold of the debate about trade agreements. Just like the TTP, the RCEP, whose negotiations were launched at the ASEAN Summit in Phnom Penh in November 2012, would connect a large chunk of the global economy, placing China and Japan at the center, and harmonize trade-related rules, investment and competition regimes. The RCEP includes a vast array of rules about investment, economic and technical cooperation, intellectual property, competition, dispute settlement and government regulation. Notably, India, set to play key economic role in Asia in the coming decades, is also part of the grouping.

Bipul Chatterjee and Surendar Singh argue that the RCEP presents a “decisive platform which could influence India’s strategic and economic status” in the Asia-Pacific region and bring to fruition its “Act East Policy.” Jeng Niamwhan, on the other hand, worries about the downsides for India’s poor:

India (…) does not grant patents for new forms or new uses of a known substance. This has prevented unnecessary extensions of patent monopolies on some cancer drugs – a move praised by health advocacy groups such as Médecins Sans Frontières as a major victory for access to affordable medicines. These safeguards would be lost if India and RCEP countries agree to Japan’s proposal.

Earlier this month, senior officials of the 16-member RCEP met in Myanmar to provide impetus to the negotiations on the trade deal. Ministers are set to meet in Kuala Lumpur on August 24 to finalize the modalities of the pact. Finalization of modalities include exchange of offers in goods, services and investments, and the member countries are expected to disclose the number of products whose duties would be reduced to zero and goods which would not have any duty cut under the pact. While RCEP was expected to be agreed upon by the end of the year, negotiations are likely to take more time, given the great number of interests involved.

The Trans-Pacific Partnership (TPP) and the Regional Comprehensive Economic Partnership (RCEP) can be understood in the context of a growing number of Chinese-led initiatives that, in their entirety, create a “parallel order” to complement and possibly some day rival existing US-led structures. In the end, the prevailing deal will allow either Washington or Beijing to act as a regional agenda-setter, shaping the architecture of economic cooperation in the Southeast and East Asian regions, and helping secure economic interests.

Still, in the realm of trade agreements, zero-sum thinking may not prevail. There are substantial differences between the two: The RCEP is an exercise in harmonizing and integrating existing FTAs between ASEAN and its individual partners, while the latter is an attempt by the United States and others to create a new, more ambitious 21st century trade agreement with much higher standards. As The Economist points out,

Ultimately, for TPP to really make a mark, it has to be bigger. Leaving out China is an expedient to get the deal done but, if kept that way, it would be a huge gap. China is the world’s biggest manufacturer. Any Asian trade zone without it faces one of two sorry fates. Either, because of China’s centrality to Asian supply chains, the deal is so riddled with exemptions that it becomes worthless. Or, if the zone gains traction, the effect is to divert trade away from the most efficient Chinese companies and hurt the global economy.

One day, the two agreements, if ever agreed on, could even merge, in what would have dramatic implications for the global economy. While the TPP has generated ample debates even in region that are not part of the negotiations, the RCEP is generally absent from the public debates around the world. That is a mistake. The European Union, Brazil and others will be directly affected by the trade creation and trade diversion produced by the agreement (or lack of it) over the coming months or years.

Photographer: Luong Thai Linh/Bloomberg

Vietnam Forecasts Record 2016 $15 Billion Foreign Investment

by

Nguyen Dieu Tu Uyen

December 9, 2016 — 3:07 AM EST December 9, 2016 — 4:20 AM EST

- Government is in talks with ADB to sell a Vietnamese bank

- Vietnam expects $2 billion to $3 billion 2016 trade surplus

Vietnam forecasts disbursed foreign direct investment to rise to a record this year with companies such as South Korea’s Samsung Electronics Co. and LG Electronics Inc. shifting factories to the Southeast Asian nation.

Bottom of Form

Disbursed foreign investment may reach $15 billion in 2016, Prime Minister Nguyen Xuan Phuc told donors, including the World Bank and the International Monetary Fund, at a Hanoi conference Friday. The country may have a trade surplus of $2 billion to $3 billion, with exports likely rising 8 percent this year, Phuc said. Disbursed FDI rose 17.4 percent to $14.5 billion last year, according to government data.

Vietnam “will redouble efforts to improve its investment environment” while also speeding up overhaul of regulations to make it easier for investors as the government boosts businesses for a faster and sustainable growth, Phuc told donors.

Rising foreign direct investment and thriving exports are helping to shield the economy from global risks. The World Bank forecasts Vietnam’s economy will expand at least 6 percent this year through 2018, among the fastest in the world. The prime minister on Thursday estimated economic growth may reach 6.3 percent in 2016.

The government, which plans to form an agency to fast-track stake sales in state companies, is in talks with the Asian Development Bank for the acquisition of a “weak Vietnamese bank,” said the prime minister, who did not provide details. The government is also working with the International Finance Corp. to speed up the resolution of bad-debt in Vietnamese banks, according to Phuc.

Vietnam needs to ensure efforts to invigorate the economy “can be achieved without raising debt to unsustainable levels,” Ousmane Dione, World Bank Country Director for Vietnam, told government officials at the conference.

Moody’s: Korea and Taiwan face similar headwinds, but policy responses diverge

Thursday, December 1, 2016 1:37 AM UTC

Moody’s Investors Service says that Korea’s (Aa2 stable) and Taiwan’s (Aa3 stable) credit profiles share robust fiscal metrics and strong governance indicators, combined with a moderate degree of geopolitical risk.

Both sovereigns also face similar headwinds from weak global demand and their strong economic ties with a slowing China (Aa3 negative).

How they address these challenges will be an important factor determining their sovereign credit trajectories, says Moody’s.

And while Taiwan’s high rating reflects the sovereign’s strong shock absorption capacity, Korea’s economic, institutional and fiscal relative strengths drive the one notch difference between their ratings.

Moody’s conclusions are contained in its just-released report “Governments of Korea and Taiwan: Peer Comparison — Similar Structural Headwinds, Divergence in Policy Response”.

Weak global growth is challenging both export-reliant economies, while ageing populations will weigh on long-term growth. However, Korea’s government has implemented some targeted fiscal stimulus measures. Moreover, business investment has remained more resilient in Korea, an indication that business conditions and prospects are better. Both fiscal stimulus and robust investment will contribute to higher growth in Korea than in Taiwan in the near term.

Korea also benefits from a more diversified export product mix and numerous trade agreements, although some of its key industries — notably shipbuilding, shipping, petrochemicals, steel and construction — face challenges.

Institutions are very strong in both countries, with somewhat higher government and policy effectiveness in Korea.

Specifically, Korea’s government has shown greater willingness to implement policy in a flexible way. It has also taken a number of steps demonstrating government and policy effectiveness, including reforms of state-owned enterprises that have contributed to reducing leverage in the sector.

In Taiwan, the use of fiscal and monetary policy stimulus has been less extensive, while the effectiveness of policy reforms aimed at diversifying the territory’s economic, financial and cultural relationships remains uncertain.

Korea and Taiwan have moderate debt-to-GDP ratios and large domestic investors bases, making borrowing highly affordable. However, in both cases the government’s revenue base is relatively narrow, potentially restricting revenue-generation capacity.

Moreover, strict fiscal and debt ceiling rules could hinder either government’s ability to implement fiscal stimulus measures if needed in the future.

Geopolitical risks constrain both ratings, says Moody’s. In Taiwan’s case, political tensions with China could constrain its ability to forge economic ties with other countries. For Korea, the risks of either a regime collapse in the North or an outbreak of war on the peninsula are low, but weigh more heavily on the rating should either take place.

In both countries, polarized politics can delay the implementation of policy measures. We do not expect such delays to have a material impact on the economy, fiscal metrics or policy implementation. The current scandal involving Korea’s President Park Geun-hye poses risks to this expectation.

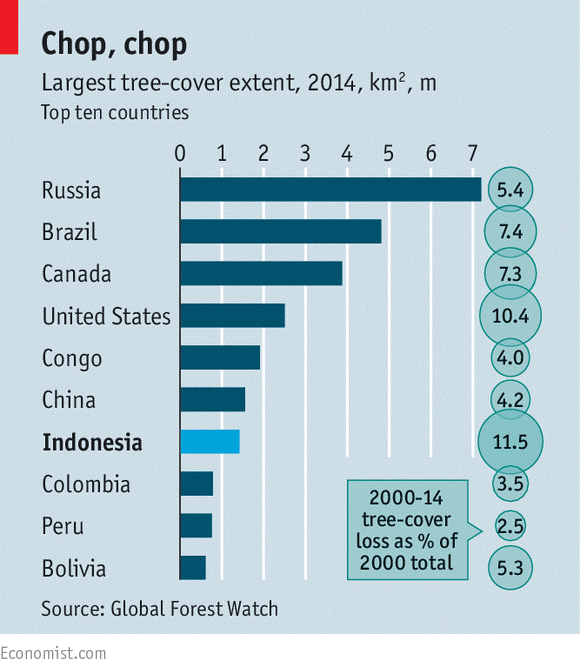

For peat’s sake -Despite tough talk, Indonesia’s government is struggling to stem deforestation

But the weather is helping a little

Nov 26th 2016, 00:00

TEGUH, chief of the village of Henda, in the Indonesian portion of Borneo, enters his office brimming with apologies for being late. The acrid scent of smoke wafts from his clothes. He explains that he was guiding police and firefighters to a fire just outside the village. A farmer had decided to clear his land by burning it. Henda sits amid Borneo’s vast peatlands; the fire had set the fertile soil smouldering for nearly 24 hours. It was a small fire, he says—perhaps a couple of hectares—but Mr Teguh still struggled to contain his exasperation, given the destruction wrought by fires set for land-clearance just a year ago.

Last year, in the autumn for the most part, at least 2.6m hectares of Indonesia’s forests burned—an area the size of Sicily. The fires blanketed much of South-East Asia in a noxious haze and released a vast plume of greenhouse gases. Much of the island’s interior was reduced to sickly scrub; along its roads stand skeletal trees, reproachful witnesses to the ravages they endured. Indonesia’s forest fires alone emitted more greenhouse gases in just three weeks last year than Germany did over the whole year. The World Bank estimates that they cost Indonesia $16bn in losses to forestry, agriculture, tourism and other industries. The haze sickened hundreds of thousands across the region, and according to one study, hastened over 100,000 deaths.

This year, happily, has seen no repeat of last year’s conflagration. Indonesia’s government would say that is because it took resolute action. Having entered office seemingly indifferent to conservation, Joko Widodo, the president, universally known as Jokowi, created a government agency charged with restoring peatlands, the site of around half of last year’s devastation. He issued a presidential moratorium on new palm-oil plantations and ratified the Paris agreement on climate change, committing Indonesia to cut greenhouse-gas emissions by 29% by 2030.

Downpours or directives?

But many environmentalists attribute the diminished burning this year to steady autumn rain rather than official resolve. After all, Susilo Bambang Yudhoyono, Jokowi’s predecessor, also promised to halt deforestation, to little avail. He launched a showy crackdown on illegal logging when he took office in 2004. In 2009 he pledged to reduce Indonesia’s greenhouse-gas emissions by 26% below the level they were then expected to reach by 2020. A year later Norway promised Indonesia $1bn if it managed to stop cutting down its forests; Mr. Yudhoyono declared a two-year moratorium on forest-clearing concessions and renewed it in 2013. But by March of this year Norway had delivered just $60m of the promised billion. “We haven’t seen actual progress in reducing deforestation” in Indonesia, Norway’s environment minister admitted.

In recent years no country has lost forest at a faster rate than Indonesia (see chart). Between 2000 and 2012 around 6m hectares of primary (meaning virgin) forest disappeared, mainly on the islands of Borneo (Kalimantan to Indonesians) and Sumatra. Roughly 40% of the deforestation took place in nominally protected areas. First come the loggers; clear-cutting and burning follow, to make way for palm-oil or timber plantations. Kalimantan’s lowland forests are almost entirely gone, and as better roads make the highlands of the interior more accessible, forests there are vanishing too. Virtually all of the haze last year came from fires on those two islands.

Indonesia contains around 14.9m hectares of peat land—most of the world’s tropical peat forests. Fires there are uniquely harmful, for several reasons. Peat is soggy and acidic, which prevents organic matter from decaying fully. That makes it a wonderful store of carbon—until it dries out, at which point it becomes flammable. Indonesia’s peat forests were unusually vulnerable last year, due both to efforts to drain peatlands to grow crops (in their natural state they are too waterlogged for agriculture) and to drought. The haze came not just from burning tree stumps, but from the smouldering soil, too.

Peat forests can be as much as 200 times more damaging to the atmosphere when burnt than other types of vegetation, both because they store more carbon and because more of it is released as

methane, an especially harmful greenhouse gas. The average incinerated hectare emits the equivalent of 55 metric tonnes of carbon. Peat forests also take far longer to regenerate than forests on mineral soils. The canals that now ribbon Kalimantan’s forests remove water from peatlands, impeding restoration and leaving them more fire-prone. Between 2000 and 2010, peatland cover declined by 41% on Sumatra, 25% on Borneo and 9% on Western New Guinea.

Sinan Abood, a geospatial analyst with America’s Forest Service, calculates that more than one-quarter of pulpwood concessions and more than one-fifth of palm-oil concessions are located on peat land. Companies grab this land not for its productivity—mineral soil is far better suited to agriculture—but because locals own or work more productive land. Bribing an official and getting immediate access to thousands of hectares of nominally protected land is easier, quicker and cheaper than negotiating with those communities.

But Indonesian politicians friendly to big palm-oil or pulp-and-paper companies like to pretend they have community interests at heart. They fret that conservation measures would harm smallholders—individual farmers with just a few acres. Faced with evidence of illegal deforestation, politicians shrug: Indonesia is a big country, they say, and policing every two-hectare plot across 13,000 islands is impossible. In fact, a paper published in 2013 found that almost 90% of deforestation in Sumatra between 2000 and 2010 was done by big palm-oil firms. Similarly, most of the deforestation in Kalimantan results from large-scale conversion to agriculture or timber plantations.

Humala Pontas, the head of environmental rehabilitation for the provincial government of Central Kalimantan, works in the department that reviews applications for forest concessions. Almost all of them are approved. But it is nearly impossible to tell, he says, whether companies stick to the terms of their concessions. Central Kalimantan is immense, and its provincial government small and poor. “We have no monitoring system,” says Mr Humala. “Last year we gave 40,000 hectares for cutting—but we have no way of knowing if they used 40,000 or 400,000.”

That is a familiar story across Indonesia, where decentralisation has saddled local governments with more responsibility than they can handle. Most are simply unable to stop powerful interests bent on deforestation. Many do not want to: the financial and political benefits from allowing business to proceed as usual often exceed those from following national policy decided thousands of miles away in Jakarta. Sometimes the incentives are terrifyingly blunt: activists tell tales of attempts to enforce forestry laws being met by men with machine-guns.

Added to a lack of capacity is a woolly governmental structure that makes it difficult to know just where the buck stops, and easy for officials to pass it. WALHI, an environmental pressure group, has filed a lawsuit over deforestation in Central Kalimantan. Among the defendants are the provincial governor and parliament, as well as Jokowi and the national ministries of health, environment and agriculture—all of which have some role in forest policy. Mr Yudhoyono’s moratorium came from the forestry ministry (now merged with the environment ministry), but the agriculture ministry handles licensing for palm-oil concessions. Such divisions are replicated at the local level, and the various entities rarely co-ordinate with each other.

This lack of enforcement makes it difficult for multinational firms that buy Indonesian paper and palm oil to adhere to their own policies against deforestation. A study published earlier this year by Greenpeace, another environmental pressure group, found that only one of 14 multinationals surveyed could trace its palm oil back to the plantation where it was grown. None could say with certainty that they did not use palm oil from recently deforested land; most could not say how much of their palm oil comes from suppliers that meet their standards and how much comes from third parties that do not.

This is not entirely due to sloth or negligence. Although satellites now enable real-time monitoring of Indonesian forests, overlapping land claims make it impossible to use those data to determine responsibility for deforestation, according to a recent paper by David Gaveau, a remote- sensing specialist with the Centre for International Forestry Research, which is based near Jakarta. Farmers often plant on companies’ concessions, and firms often clear land outside their allocated areas. The satellites can detect forests going up in flames, but only observers on the ground can determine who set them alight.

There are a few modest reasons for hope. The bureaucracy is showing marginally more resolve: arrests for starting fires are up, and several companies have been fined or otherwise sanctioned for their role in last year’s conflagration. Jokowi has continued to push Indonesia’s OneMap initiative http://blog.cifor.org/22534/new-tech-better-map-on-tap-to-protect-indonesian-forests?fnl=en , which would gather all land-use data in one place. Nazir Foead, the head of Indonesia’s new Peatland Restoration Agency, has a conservation rather than an industry background, and seems to have the president’s ear. Indonesia’s highest Muslim authority has issued a fatwa condemning intentional forest burning.

Individual Indonesians are doing their part, too. In a churchyard near Henda, Mr. Teguh pushes aside some plastic sheeting on a crude bamboo greenhouse, and proudly displays rows of native hardwood saplings. He grows hundreds of thousands each year to help reforest peatlands in Kalimantan and Sumatra. He plucks a wrapped sapling, twig-thin but crowned with a spray of healthy, spiky leaves. “This is the best we can do to help God,” he says. It will take far more than that, alas, to return Indonesia’s forests to health.

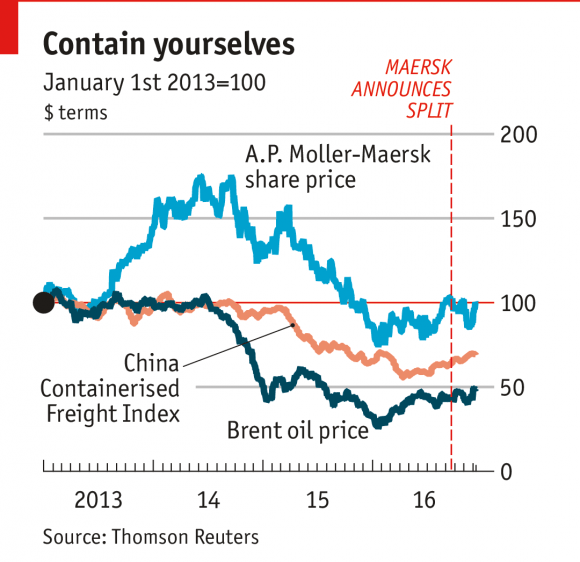

Sunk capital: Maersk and shipping

The world’s largest container-shipping firm, a Danish conglomerate with interests in energy and logistics, shocked financial markets earlier this year when it suddenly sacked its CEO and announced it would break itself up. Today at Maersk’s Capital Markets Day its new boss, Soren Skou, will outline to investors how it will split off its oil-and-gas assets from its shipping division. Investing in both was meant to be a counter-cyclical hedge, but since 2014 oil prices and freight rates have both tumbled, throwing all parts of the business into a sea of red ink. A split will help its executives focus (investors will hope) on cutting costs in its container-shipping division. But the firm’s merger with Hamburg Süd, a rival line, and a co-operation deal announced earlier this month with Hyundai Merchant Marine of South Korea, may make some shareholders worry that Maersk is expanding too fast. More stormy seas lie ahead.

Surprise, surprise: the world economy

Where to look for nice economic surprises in 2017? America, perhaps? Economists are busy revising upwards their forecasts for GDP growth on the prospect of a fiscal stimulus. But it is unclear how much, how soon and to what effect taxes will be cut. A strong dollar may stir Donald Trump’s protectionist instincts, to no one’s benefit. Emerging markets? A year ago, South Africa, Turkey and Malaysia were potential trouble spots. They still are. People have stopped worrying about China’s economy but the problems of high debt and industrial overcapacity remain. The best hope for good news is in places that have seemed hopeless, such as Russia and Brazil. Or perhaps Japan, whose central bank is committed to reflating the economy; its efforts might just bear fruit in 2017. And the euro-zone economy might do fine, if only because German politicians, with elections looming, turn a blind eye to fiscal laxity elsewhere.

Triple whammy: corporate deal making

The past six years have seen one of the largest booms ever in mergers and acquisitions. But the pace of dealmaking is likely to slow in 2017, for three reasons. First, rising protectionism will make cross-border deals harder to pull off; Germany and Australia have recently blocked proposed acquisitions by Chinese groups, for instance. Second, the largest multinationals have seen their returns on equity slump to around 10%, from a peak of 18%, and investors may be reluctant to create more sprawling leviathans. Lastly, consolidation in America has left a majority of industries more concentrated than in the past, prompting antitrust concerns. During the election campaign Donald Trump signalled that he was hostile to oligopolies, complaining about Amazon’s muscle and criticising AT&T’s proposed takeover of Time Warner. Dealmakers will be watching closely to see whether his trust-busting instincts make it to the White House.

Happy New Year! |

|