Second Quarter 2016 Economic and Wood Product News (Part 1)

A special report from the Economist and sponsored by PIMCO http://pimcoforum.economist.com/calmer-cs-ahead-china-commodities-and-central-banks-dominate-the-global-outlook/

https://www.pimco.com/our-firm

The world economy

System says slow

The IMF sees political danger in the economic doldrums

Apr 16th 2016 | From the print edition

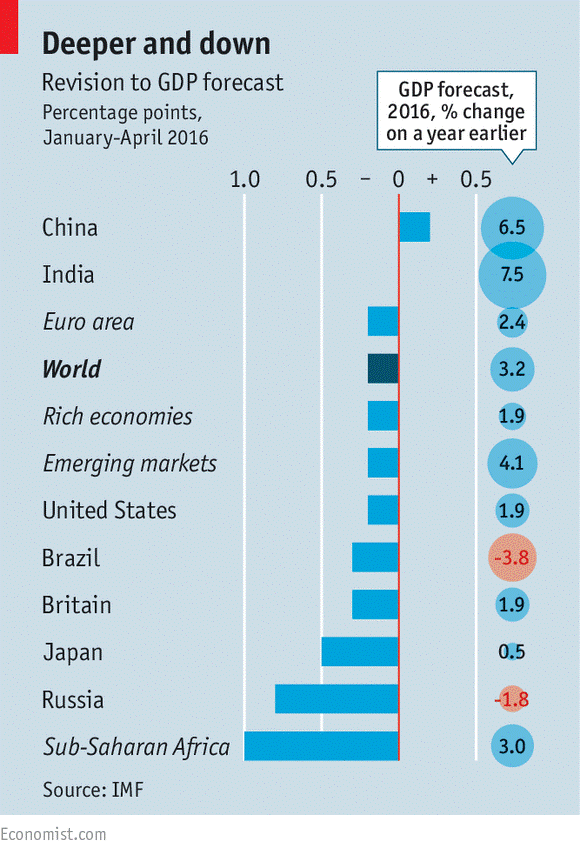

IS THERE a global economic crisis on the horizon? Probably not. Is the world in danger of falling into recession? Not soon. Yet the IMF’s latest update of its forecasts is nevertheless resolutely downbeat. Speaking this week in Washington, DC, its chief economist, Maurice Obstfeld, outlined yet another downward revision to its prediction for global GDP growth. It is likely that the next revision will again be down. One of the big threats to the world economy, he said, is from “non-economic risks”—fund-speak for grubby politics. A world economy stuck in the doldrums, he cautioned, may be a perilous place politically.

The actual forecasts are far from horrible. The fund nudged down its estimate of global growth for 2016 from 3.4% to 3.2%. That is still a shade faster than in 2015. The revisions are broad-based: America, Europe and the emerging world as a bloc all saw similar downgrades (see chart). The forecast for sub-Saharan Africa was pared back the most, in large part because of a gloomier outlook for oil-rich Nigeria, the continent’s largest economy. The recent recovery in crude prices will take some pressure off oil producers, but “we won’t be seeing prices at the $100 a barrel level for some time, if ever,” said Mr. Obstfeld. Of biggish economies, only China escaped a downgrade. The fund is more confident than it was in January that stimulus measures there will work. But there is a concern about the quality of China’s growth, said Mr. Obstfeld, as fresh credit is directed towards sputtering industries.

The scenario the fund seems most concerned about is a steady slide in global GDP growth that feeds on itself by discouraging investment, thereby exacerbating political tensions, which in turn make fixing the economy even harder. Brazil shows how a bad economy can be made worse by political paralysis. Low growth might add to the “rising tide of inward-looking nationalism” in the rich world, said Mr. Obstfeld. Politics in America is moving against free trade. And there are various threats to Europe beyond the perennial problem of Greece. The refugee crisis has already put pressure on the European Union’s open-borders policy and there is a “real possibility” that Britain might leave the EU.

The IMF has some familiar remedies for the global economy: keep monetary policy loose, augment it with fiscal stimulus where possible and add some pro-growth reforms to the mix. Such action is needed to insure against the risks the fund identifies. But the world should also be making contingency plans for a coordinated response if a financial shock hits. “There is no longer much room for error,” said Mr. Obstfeld, with a certain weariness.

Trends in Japanese wooden furniture imports

March 01, 2016

Source:

ITTO

Wooden furniture imports continue to gain market share; it has been estimated that imports of bedroom, kitchen and dining-room furniture accounted for around 60% of the market in 2015. The growth in imports from China and Southeast Asian countries continues to hollow out domestic wooden furniture manufacturing.

The figure shows trends in housing starts and imports of wooden office, kitchen and bedroom furniture. At first sight there appears to be a contradictory inverse relationship between trends in housing (falling) and imports (rising). Rather than a statistical anomaly, however, this reflects the rapid growth in the market share captured by imports.

The Japanese furniture market was worth around yen 900 billion in 2005, and imports of wooden office, kitchen and bedroom furniture accounted for about 16% of all domestic sales. By 2015, the size of the market had fallen to around yen 700 billion, and imports accounted for over 25% of the market.

Data from Japan’s Ministry of Internal Affairs and Communications show that purchases of wooden chests of drawers, a main item in the traditional “bridal furniture set”, have dropped dramatically over the past 15 years. On the other hand, household spending on dining-room furniture has been fairly stable—although relatively small compared with spending on bedroom items.

In the past, the bridal market was a main driver of growth in Japan’s furniture sector. It was usual for the bride’s family to buy a three-piece furniture set consisting of a wardrobe, a Japanese-style chest of drawers, and a dressing table.

Today, the traditional dressing-table has been replaced by western-style chests of drawers and, because many newly built houses and apartment have built-in closets, demand for free-standing wardrobes has faded. This, combined with the decline in the number of marriages, has upended the established demand patterns for wooden furniture in Japan.

Bedroom furniture

China’s exports of bedroom furniture to Japan accounted for 57% (by value) of all wooden bedroom furniture imports in 2015. The second- ranked supplier last year was Viet Nam, with 28% of all imports, and other Southeast Asian countries made up around 8%. The combined market share of these three suppliers in 2015 was over 90%, the balance coming mainly from Europe and North America.

Kitchen furniture

Fitted kitchens are now a standard feature of newly constructed houses and apartments, and the replacement kitchen market is growing strongly as owners of existing homes embrace renovation to avoid the cost of demolition and rebuilding (once a feature of the Japanese housing sector).

In the early days of kitchen modernization, European and North American makers of kitchen units and cabinets found a ready market in Japan. It took suppliers in Asia only a short time to grasp the opportunity, however, and they began growing their market share.

Manufacturers of kitchen furniture in Viet Nam have secured a significant part of the market (41% in 2015), as have shippers in Indonesia, Malaysia and Thailand. Demand for European kitchen furniture tends to focus on German and Italian lines in the up-market housing sector.

Hollowing out the furniture manufacturing base Japan’s domestic furniture manufacturing sector has declined as Japanese companies—even small and medium-sized companies—have shifted production outside Japan to countries where production costs are lower, populations are growing and there is good infrastructure and communications. In Japan’s wooden furniture market, relocated Japanese companies are responsible for much of the export trade from China and Southeast Asia to Japan.

China was once the preferred destination for relocating Japanese companies—it is close to Japan and has good shipping connections. Moreover, wages and energy costs have been much lower than in Japan, and domestic demand has grown rapidly. This has now changed, however: rising wages, labour disputes, and the reemergence of bitter historical issues are causing many Japanese companies to look elsewhere for their investments.

Viet Nam has attracted Japanese companies, and the trade relationship between the two countries is very close. Viet Nam’s overall exports to Japan are now almost 10% of all its exports, ranking second after North America. The main products exported to Japan are garments, seafood, wood products and electronics. In 2015, around 1000 Japanese companies had production capacity in Viet Nam.

Yen surges and stocks sink after Bank of Japan keeps policy on hold

Decision comes despite return to annual deflation for first time since 2013

Read latest:

The Bank of Japan risks a reputation for caprice

Haruhiko Kuroda at a news conference following a monetary policy meeting at the BoJ headquarters in Tokyo in January © EPA

by: Robin Harding in Tokyo

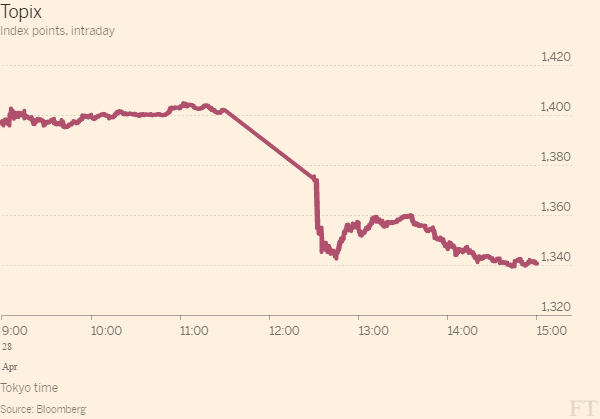

The yen surged by 3 per cent and equities slumped after the Bank of Japan dashed market hopes of stimulus despite data showing the country had fallen back into deflation for the first time since 2013.

It means that Haruhiko Kuroda, the BoJ governor, confronts the most perilous moment of his three-year battle against deflation as a rising yen threatens to undermine the confidence of Japanese companies.

Mr. Kuroda insisted he is simply waiting to judge the effects of January’s shock move to interest rates of minus 0.1 per cent, but his inaction highlights the BoJ’s increasingly passive and after-the-fact responses to weak data.

“We have kept monetary policy on hold this time while the effects of quantitative easing with a minus interest rate sink in,” Mr. Kuroda said. “Those effects don’t appear in a month or two but I don’t think it’ll take as long as six months or a year.”

That timescale suggests the BoJ could ease policy again over the summer. Mr. Kuroda, who has shown a preference for large, surprise actions rather than incremental easing, said the central bank will act “without hesitation” if further loosening is needed to reach 2 per cent inflation.

The broad Topix stock index closed down 3.2 per cent at 1,341 with banking shares especially hard hit. The yen was up 3 per cent at ¥108.2 against the dollar, close to its high for the year.

Mr. Kuroda’s decision to keep rates on hold, when more than half of market analysts expected an easing, is partly a bet that a recovering US economy will come to the rescue. A neutral statement from the US Federal Reserve the previous night held open the possibility of a US rate rise in June.

Masaaki Kanno, chief economist at JPMorgan in Tokyo, said there were two ways to look at the BoJ’s decision. One is the central bank’s own explanation that negative rates are working but “it will take time for the results to come through”.

The other is less benign. “What is left in their toolbox is limited and Mr. Kuroda has two more years. If the BoJ eases too soon … the toolbox might not be empty, but there wouldn’t be much left in it,” Mr. Kanno said.

Despite no change to policy, the BoJ took a knife to its economic forecasts, predicting growth of 1.2 per cent instead of 1.5 per cent for the fiscal year to March 2017. It cut its inflation forecast, excluding fresh food, from 0.8 to 0.5 per cent.

The BoJ also changed its guess of when inflation will reach 2 per cent from the “first half of fiscal 2017” to “fiscal 2017”. Any further delay would mean admitting Mr. Kuroda will not reach the target during his term in office.

The BoJ also changed its guess of when inflation will reach 2 per cent from the “first half of fiscal 2017” to “fiscal 2017”. Any further delay would mean admitting Mr. Kuroda will not reach the target during his term in office.

Earlier in the day, data showed the headline consumer price index down 0.1 per cent on a year ago, compared with analyst expectations of no change, as weak commodity prices weigh on Mr. Kuroda’s efforts to drive up inflation.

But while prices continue to stagnate, there was better news from Japan’s labour market, with the unemployment rate down from 3.3 per cent to 3.2 per cent and the ratio of job openings to applicants up 0.02 points to a new 25-year high of 1.3 times.

A tightening labour market will eventually push up wages and lead to higher inflation, the BoJ hopes.

The central bank voted to keep rates on hold by a majority of 7-2. The only change was a minor subsidy to earthquake-hit banks on the southern island of Kyushu, providing them with zero-interest loans and exempting more of their balances from negative interest rates.

With funds for reconstruction already pouring into Kyushu, local banks have seen a rise in deposits, forcing them to bear a greater burden of negative rates. The changes offset that.

Copyright The Financial Times Limited 2016.

China aims to lay off up to 6 million workers, earmarks about $23-billion

Benjamin Kang Lim, Matthew Miller and David Stanway

BEIJING — Reuters

Published Tuesday, Mar. 01, 2016 5:28AM EST

Last updated Tuesday, Mar. 01, 2016 1:31PM EST

China aims to lay off 5 million to 6 million state workers over the next two to three years as part of efforts to curb industrial overcapacity and pollution, two reliable sources said, Beijing’s boldest retrenchment program in almost two decades.

China’s leadership, obsessed with maintaining stability and making sure redundancies do not lead to unrest, will spend nearly 150 billion yuan ($23-billion) to cover layoffs in just the coal and steel sectors in the next 2-3 years.

The overall figure is likely to rise as closures spread to other industries and even more funding will be required to handle the debt left behind by “zombie” state firms.

The term refers to companies that have shut down some of their operations but keep staff on their rolls since local governments are worried about the social and economic impact of bankruptcies and unemployment.

Shutting down “zombie firms” has been identified as one of the government’s priorities this year, with China’s Premier Li Keqiang promising in December that they would soon “go under the knife”..

The government plans to lay off five million workers in industries suffering from a supply glut, one source with ties to the leadership said.

A second source with leadership ties put the number of layoffs at six million. Both sources requested anonymity because they were not authorized to speak to media about the politically sensitive subject for fear of sparking social unrest.

The ministry of industry did not immediately respond when asked for comment on the reports.

The hugely inefficient state sector employed around 37 million people in 2013 and accounts for about 40 per cent of the country’s industrial output and nearly half of its bank lending.

It is China’s most significant nationwide retrenchment since the restructuring of state-owned enterprises from 1998 to 2003 led to around 28 million redundancies and cost the central government about 73.1 billion yuan ($11.2-billion) in resettlement funds.

On Monday, Yin Weimin, the minister for human resources and social security, said China expects to lay off 1.8 million workers in the coal and steel industries, but he did not give a time-frame.

China aims to cut capacity gluts in as many as seven sectors, including cement, glassmaking and shipbuilding, but the oversupplied solar power industry is likely to be spared any large-scale restructuring because it still has growth potential, the first source said.

DEBT OVERHANG

The government has already drawn up plans to cut as much as 150 million tonnes of crude steel capacity and 500 million tonnes of surplus coal production in the next three to five years.

It has earmarked 100 billion yuan in central government funds to deal directly with the layoffs from steel and coal over the next two years, vice-industry minister Feng Fei said last week.

The Ministry of Finance said in January it would also collect 46 billion yuan from surcharges on coal-fired power over the coming three years in order to resettle workers. In addition, an assortment of local government matching funds will also be made available.

However, the funds currently being offered will do little to resolve the problems of debts held by zombie firms, which could overwhelm local banks if they are not handled correctly.

“They have proposed this dedicated fund only to pay the workers, but there is no money for the bad debts, and if the bad debts are too big the banks will have problems and there will be panic,” said Xu Zhongbo, head of Beijing Metal Consulting, who advises Chinese steel mills.

Factories shut down would have to repay bank loans to avoid saddling state banks with a mountain of non-performing loans, the sources said. “Triangular debt”, or money owed by firms to other enterprises, would also have to be resolved, they added.

Although China has promised to help local banks transfer the bad debts of zombie steel mills to asset management firms, local governments are not expected to gain access to the worker lay-off funds until

April 13, 2016 4:51 am

China export surge points to improving economic outlook

Tom Mitchell and Yuan Yang in Beijing

@Bloomburg

China reported stronger than expected trade data on Wednesday, the latest sign of a tentative revival in fortunes that paves the way for Friday’s release of first-quarter economic growth.

Exports surged 18.7 per cent in renminbi terms in March over the same month last year, after declines in both January and February. Imports also stabilized, dropping just 1.7 per cent compared with an 8 per cent fall in February.

In dollar terms, exports rose 11.5 per cent while imports fell 7.6 per cent for the period, reflecting the renminbi’s recent rise. The currency has gained 1.9 per cent against the dollar over the past two months.

China’s export sector has been buffeted by the slowdown in global trade, the dollar value of which has been shrinking since 2012 largely because of the slump in international commodities prices.

The International Monetary Fund this week warned that the world risked a “synchronized slowdown” but highlighted China as a rare bright spot among major economies. Chinese officials have been working to counter international investors’ increasingly negative outlook for the country’s economy.

Their cause has been boosted by a slew of better than expected data releases, including March inflation figures that showed producer price deflation had moderated.

This contributed to the IMF’s decision to revise upwards its forecast for Chinese economic growth this year, to 6.5 per cent from 6.3 per cent. At last month’s meeting of China’s parliament, Premier Li Keqiang projected economic growth of 6.5-7 per cent for 2016.

“China’s commodity imports should see further improvement soon,” said Zhou Hao at Commerzbank. A recent increase in iron ore inventories tallies with improving industrial production although Chinese steel exports have been the subject of an increasingly contentious international debate after mill closures across Europe and the US.

Chinese steel exports surged by 30 per cent in March compared with the year before, to 9.98m tonnes. First-quarter exports of 27.83m tonnes of the metal put the county on track to match a record 112m tonnes in 2015.

“China’s trade data for March point to healthy growth in import volumes and add to growing evidence that the extreme gloom of a few weeks ago about the domestic economy was misplaced,” said Marcel Thieliant and Mark Williams at Capital Economics.

Shanghai-traded stocks rose almost 2 per cent on the trade data, extending a strong two-month rally.

China’s foreign exchange reserves rose $10.3bn in March to $3.2tn, the first increase in five months, helped in part by large trade surpluses.

Wednesday’s trade data included a Rmb194bn trade surplus for March. Large net export statistics have helped bolster China’s economic growth figure over the past year.

China is trying to rebalance its economy from export-oriented manufacturing and heavy industry to domestic consumption and services. However, many analysts believe this transformation could be undermined by overly generous credit support to state-owned enterprises, especially “zombie” companies in sunset sectors such as cement, coal and steel.

The IMF said on Tuesday it was concerned the recent improvement in China’s economic outlook was driven by short-term stimulus measures that could exacerbate the country’s already large debt pile.

Copyright The Financial Times Limited 2016

Surprising recovery of the Chinese housing market in the first two months

April 14, 2016

Source:

Activity in China’s real estate sector in the first two months of 2016 has been reported by the Chinese National Bureau of Statistics (NBS). China releases combined data for January and February to smooth out the effect of the slowdown in construction over the Lunar New Year holiday period.

The press release from the NBS says total investment in the first two months of 2016 was up 3% year-on-year.

Investment in residential buildings was up by 1.8% and accounted for two thirds of total investment in the sector.

Sales of residential buildings in the first two months of this year rose as the Chinese authorities eased credit requirements to encourage consumers to buy homes.

New home sales rose almost 50% year on year during the January-February period. For 2015 home sales nationwide rose almost 17% after the decline in 2014.

But, looking ahead, in the first two months of this year land purchases by real estate development enterprises fell 19.4% year on year however, the January and February performance was a considerable improvement on the steep declines recorded at the end of last year.

In the first two months of this year sales of commercial buildings increased 28%, a sharp rise on the pace of growth last year.

New fronts open up in rekindled currency wars

From Sweden to China, central banks are undermining their money for global advantage

The renminbi is one combatant in the currency wars © Bloomberg

April 3, 2016

by: Madison Marriage

In 2010 Guido Mantega, then Brazil’s finance minister, accused the United States and fellow powerful economies of deliberately weakening their currencies in order to take a greater slice of global trade — what he called a “currency war”.

His comments sparked calls from officials at the World Bank and the International Monetary Fund for the world’s leading economies to do more to avoid inflaming tensions by pursuing protectionist monetary policies. The issue dominated the agenda of both the IMF meeting in Washington and the G20 meeting of world leaders in Seoul that year.

The idea that central banks in China, Japan, the US and the eurozone have deliberately attempted to devalue their currencies to improve competitiveness has since taken hold.

But investors and economists remain sharply divided on whether currency wars are still taking place as a phenomenon — if they ever did.

Some accept the arguments made by central bankers that monetary policy changes — such as pushing interest rates down or increasing the supply of money in circulation through quantitative easing — were intended to tackle other serious problems, such as low inflation.

“It is difficult to find significant examples of genuine mercantilist economic policy based on competitive devaluation,” says Alexis de Mones, head of fixed income at Ashmore, the emerging markets-focused asset manager.

Javier Corominas, head of economic research at Record Currency Management, the UK fund house, adds that even if Mr. Mantega’s 2010 proclamation may have been justified at the time, it now seems out of date. “I am not sure we are in a currency war at the moment — we seem to be in an era of currency peace,” he says, and policymakers know the risks of such a war.

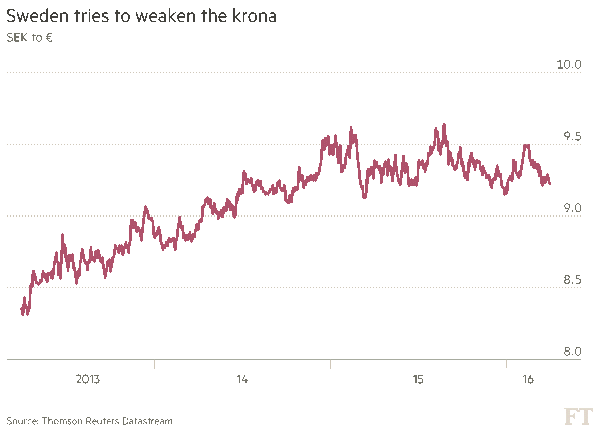

Many others, however, insist currency wars remain very much alive and thriving, to the detriment of investors and savers in emerging and developed markets. “I would argue that a number of central banks are engaged in currency wars — the most obvious example is the Riksbank in Sweden,” says Adrian Owens, currency fund manager at Swiss investment house GAM.

Sweden has a healthy annual credit growth rate of 8.8 per cent, house prices are growing at 18 per cent and GDP growth was 4.1 per cent last year. The country has a current account surplus of around 6 per cent of GDP.

Despite these reassuring economic signals, the Riksbank took market participants by surprise in February by pushing Swedish interest rates further into negative territory, to minus 0.5 per cent from minus 0.35 per cent, and said rates could fall further if needed. The Swedish krona weakened against the euro in the aftermath of the decision, rising to SKr9.59, from SKr9.47.

“On every metric, other than headline inflation, that’s a really strong economy. Yet [Sweden’s central bank has] said if their currency appreciates too quickly, they will intervene and [blame] headline inflation,” says Mr Owens. “But on every other metric what they are doing is completely inappropriate. That is as close to a currency war as you can get.”

Investors are bracing for further surprising, unwanted monetary policy shifts in the belief that volatile markets since the start of the year are likely to encourage central bankers to employ protectionist tactics.

This is despite global leaders at a G20 meeting in Shanghai in February agreeing to refrain from currency competition in what some perceived to be a currency truce.

Mr. de Mones believes the meeting was reassuring for investors, triggering a strong rally in credit markets and emerging market currencies. “Since then, both the European Central Bank and the Bank of Japan have passed on opportunities to push their currencies lower, and the US Federal Reserve has played its part in this joint effort to reduce [forex] volatility by delivering a very dovish message,” he says.

Others are sceptical about whether the ceasefire will last. David Riley, head of credit strategy at Blue Bay Asset Management, the London-based hedge fund company, says: “Markets have decided that, by accident or design, there is a ceasefire in the global currency war. If there was a ‘truce’, it is fragile.”

Mr. Riley believes conflicting monetary policies are likely to become a reality once again as soon as the US Federal Reserve raises interest rates — as it is expected to do later this year — and if the ECB and the BoJ continue to pursue quantitative easing policies “in a desperate attempt to raise growth and inflation expectations”.

“The danger is that the extraordinary monetary policies that helped prevent a global depression in the aftermath of the 2008 financial crisis [will] descend into a race to the bottom, with China as the principal causality,” he says.

Indeed, China is one of the biggest concerns for forex strategists. At the end of March, China’s central bank weakened the renminbi significantly against the dollar, and several fund managers interviewed said that the currency could fall further. Some fund houses, including Amundi, Europe’s largest listed investment company, recommend shorting the renminbi as a result.

Investors are also closely watching Korea’s central bank for signs that it might weaken the won, in turn, to remain competitive against Japan and China.

Mr. Owens says that while inflation is below target, this sort of aggression can be tolerated, but ultimately “there are lots of second-round effects that [central banks] do not fully appreciate”.

These effects include “protectionism and trade barriers which will be detrimental to global trade and economic activity”, says Abi Oladimeji, head of investment at Thomas Miller Investment, the London-based wealth manager. “[This in turn] will undermine investor confidence and result in higher volatility.

“So long as the global economy remains moribund, the temptation to adopt ‘beggar-thy-neighbour’ policies will persist.”

China: six new large forest reserves will be created

May 09, 2016

Source:

ITTO/Fordaq

As a part of China’s National Forest Reserve Construction Planning for 2016 to 2050, six new large forest reserves will be created, reports ITTO with the reference to the State Forestry Administration (SFA).

Reserves will be created in the southeast coastal regions, in the middle and lower reaches of the Yangtze River, on the Huang Huai Hai plain and in the southwest, Beijing, Tianjin and Hebei Provinces.

Another reserve will be set up in the Northeast. When completed, the area of national reserves will extend to 14 million hectares. According to forecasts, around 95 million cubic metres of logs can be sourced from national forests gradually rebalancing domestic supply and demand.

Metropolitan Hardwood Floors

China’s wood flooring production registers a drop of 2.2%

May 12, 2016

Source:

Fordaq

According to the statistics from China National Forest Products Industry Association, China’s wood flooring production volume was 384.2 million m2 in 2015, a drop of 2.2% from 2014.

Laminated flooring has the largest market share in total flooring production volumes, representing 55% of total flooring production and sales volumes.

Even though the rate of housing starts in China is slower, there will still be a large market potential for flooring products given the growth in the renovation market.

Now China has around 2,300 of wood flooring producing companies, including 800 solid wood flooring manufacturers, 900 of laminated flooring manufacturers, 500 of engineered flooring manufacturers, and 150 of bamboo flooring manufacturers. However, of all production manufacturers, 90% are small sized companies.

April 28, 2016 12:06 pm

China’s robot revolution

Ben Bland

The Ying Ao sink foundry in southern China’s Guangdong province does not look like a factory of the future. The sign over the entrance is faded; inside, the floor is greasy with patches of mud, and a thick metal dust — the by-product of the stainless-steel polishing process — clogs the air. As workers haul trolleys across the factory floor, the cavernous, shed-like building reverberates with a loud clanging.

Guangdong is the growth engine of China’s manufacturing industry, generating $615bn in exports last year — more than a quarter of the country’s total. In this part of the province, the standard wage for workers is about Rmb4,000 ($600) per month. Ying Ao, which manufactures sinks destined for the kitchens of Europe and the US, has to pay double that, according to deputy manager Chen Conghan, because conditions in the factory are so unpleasant. So, four years ago, the company started buying machines to replace the ever more costly humans.

Nine robots now do the job of 140 full-time workers. Robotic arms pick up sinks from a pile, buff them until they gleam and then deposit them on a self-driving trolley that takes them to a computer-linked camera for a final quality check.

The company, which exports 1,500 sinks a day, spent more than $3m on the robots. “These machines are cheaper, more precise and more reliable than people,” says Chen. “I’ve never had a whole batch ruined by robots. I look forward to replacing more humans in future,” he adds, with a wry smile.

Across the manufacturing belt that hugs China’s southern coastline, thousands of factories like Chen’s are turning to automation in a government-backed, robot-driven industrial revolution the likes of which the world has never seen. Since 2013, China has bought more industrial robots each year than any other country, including high-tech manufacturing giants such as Germany, Japan and South Korea. By the end of this year, China will overtake Japan to be the world’s biggest operator of industrial robots, according to the International Federation of Robotics (IFR), an industry lobby group. The pace of disruption in China is “unique in the history of robots,” says Gudrun Litzenberger, general secretary of the IFR, which is based in Germany, home to some of the world’s leading industrial-robot makers.

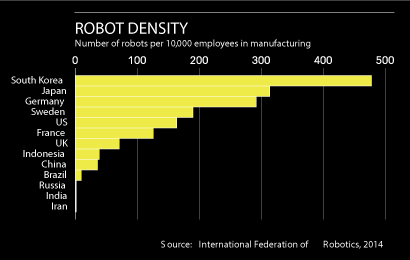

China’s technological transformation still has far to go — the country has just 36 robots per 10,000 manufacturing workers, compared with 292 in Germany, 314 in Japan and 478 in South Korea. But it is already changing the face of the global manufacturing industry. In the process, it is raising broader questions: can emerging economies still hope to follow the traditional route to prosperity that the developed world has relied upon since Britain’s industrial revolution in the 18th century? Or will robots assume many of the jobs that once pulled hundreds of millions out of poverty?

Chen Conghan, deputy manager at Ying Ao: ‘These machines are cheaper, more precise and more reliable than people’

China’s spending splurge on industrial robots has its roots in a pressing economic problem. From the 1980s onwards, as Beijing’s Communist rulers opened up to global trade, the country’s huge, cheap workforce helped make it the world’s biggest exporter of manufactured goods. Breakneck economic growth lifted hundreds of millions of Chinese out of poverty and transformed swaths of the country, as workers migrated from the countryside to the city. But a growing middle class and an ageing population have led to rising wages, eroding China’s competitive advantage. Partly because of the one-child policy, formally phased out in 2015, China’s working-age population is expected to fall from one billion people last year to 960 million in 2030, and 800 million by 2050.

In recent years, China’s central planners have been promoting automation as a way to fill the labour gap. They have promised generous subsidies — to be doled out by local governments — to smooth the way for Chinese companies both to use and build robots. In 2014, President Xi Jinping called for a “robot revolution” that would transform first China, and then the world. “Our country will be the biggest market for robots,” he said in a speech to the Chinese Academy of Sciences, “but can our technology and manufacturing capacity cope with the competition? Not only do we need to upgrade our robots, we also need to capture markets in many places.”

The march of the machines, not just in China but around the world, has been accelerated by sharp falls in the price of industrial robots and a steady increase in their capabilities. Boston Consulting Group, a management consultancy, predicts that the price of industrial robots and their enabling software will drop by 20 per cent over the next decade, while their performance will improve by 5 per cent each year.

Liu Hui, an entrepreneur in his forties, is making the most of China’s robot boom. In 2001, when he opened his first factory in Foshan, an industrial city of seven million people in Guangdong, he started out making knock-offs of electric fans. As his business grew, he moved to bona fide manufacturing, producing components for Chinese home appliance brands. Then, in 2012, spotting an opportunity in a growing market, he jumped into the emerging world of robotics. Liu now imports robotic arms from suppliers such as the Swedish-Swiss conglomerate ABB, and sells them on to Chinese manufacturers, helping them integrate the machines into their production lines. It is a highly specialized business. Most of his customers are component-makers who supply motors and other parts to large Chinese home-appliance brands such as Midea and Galanz, which produce air conditioners, refrigerators and more.

E-Deodar: Robot arms are programmed to complete repetitive tasks

Business has expanded so quickly in the past year that Liu does not have enough space in his factory for all the machinery he is assembling. He has to store parts designed to support a $23,000 ABB robot under a makeshift lean-to outside. “Things are changing rapidly,” he says. “The cost of labour is rising every year, and young people don’t want to work on the production line like their parents did, so we need machines to replace them.”

The stereotypical image of China’s factories can still be found in many places: tens of thousands of people in long lines hunched over sewing machines or slotting components into a printed circuit board. But that mode of manufacturing is starting to be replaced by a more mixed picture: partially automated production lines, with human workers interspersed at a few key points.

Meanwhile, China is developing its own robot makers. In September last year, Ningbo Techmation, a Shanghai-listed producer of machinery for the plastics industry, launched a subsidiary, E-Deodar, making robots that are 20-30 per cent cheaper than those produced by international companies such as ABB, Germany’s Kuka or Japan’s Kawasaki. The E-Deodar factory in Foshan, with its café, chill-out zone and open-plan production line, looks more like the offices of a Silicon Valley tech start-up than a Chinese industrial workhorse. “Our global rivals are very good at making robots but their costs are higher and they are not so good at understanding the needs of local customers,” says Zhang Honglei, the company’s 35-year-old, spiky-haired technical director.

The cost of labour is rising and young people don’t want to work on the production line like their parents did

– Liu Hui, Chinese entrepreneur

This year, Zhang plans to produce 350 distinctively green-colored robots, which are designed for use in plastic factories and sell for between $14,000 and $18,000 each; in three years’ time he hopes to produce 3,000 a year. “We have to move fast because automation is a scale business,” he says. “The bigger the better.”

Chinese manufacturers, which bought 66,000 of the 240,000 industrial robots sold globally last year, still largely prefer to buy international brands, according to Litzenberger of the IFR. But she expects that to change, particularly in the wake of the Beijing government throwing its full support behind the domestic robot industry in recent years. “They are developing very fast,” she says.

Zhang Peng, vice-director of the economy and technology bureau, Shunde, Foshan

At an imposing, colonnade-fronted government building — known locally as the “White House” — in the Shunde district of Foshan, officials are trying to put President Xi’s call for a robot revolution into practice. The province of Guangdong has vowed to invest $8bn between 2015 and 2017 on automation. Zhang Peng, vice-director of Shunde’s economy and technology bureau, recently had his office in the building reduced in size, in line with the Communist party’s call for bureaucratic austerity. But the budget for industrial automation was unaffected. Zhang says robots are vital to overcome labour shortages and help Chinese companies make better quality, more competitive products. Unusually straight-talking for a Chinese official, he warns: “If manufacturing companies don’t improve, they won’t be able to survive.”

Government support for the integration of ever cheaper and more efficient industrial robots is good news for factory owners in China, who are facing a weak global economy and a slowdown in domestic demand. But the benefits of the robot revolution will not be shared equally across the world. Developing countries from India to Indonesia and Egypt to Ethiopia have long hoped to follow the example of China, as well as Japan, South Korea and Taiwan before them: stimulating job creation and economic growth by moving agricultural workers into low-cost factories to make goods for export. Yet the rise of automation means that industrialisation is likely to generate significantly fewer jobs for the next generation of emerging economies. “Today’s low-income countries will not have the same possibility of achieving rapid growth by shifting workers from farms to higher-paying factory jobs,” researchers from the US investment bank Citi and the University of Oxford concluded in a recent report, The Future Is Not What It Used to Be, on the impact of technological change.

They argue that China’s rising labour costs are a “silver lining” for the country because they are driving technological advancement, in much the same way that an increase in wages in 18th-century Britain provided impetus to the world’s first industrial revolution. At the same time, according to Johanna Chua, an economist at Citi in Hong Kong, industrial laggards in parts of Asia and Africa face a “race against the machines” as they struggle to create sufficient manufacturing jobs before they are wiped out by the gathering robot army in China and beyond.

Tom Lembong, Indonesia’s 45-year-old trade minister, and a leading voice for liberalization and reform within the government of Southeast Asia’s biggest economy, is aware of the risks. “Many people don’t realize we’re seeing a quantum leap in robotics,” he says. “It’s a huge concern and we need to acknowledge the looming threat of this new industrial revolution. But as a political and business elite, we’re still stuck on debates about industrialization that were settled in the 20th and even 19th centuries.”

Countries such as Indonesia are already suffering from something that the Harvard economist Dani Rodrik has dubbed “premature de-industrialization”. This describes a trend where emerging economies see their manufacturing sector begin to shrink long before the countries have reached income levels comparable to the developed world. Despite rapid economic growth over the past 15 years, Indonesia saw its manufacturing industry’s share of the economy peak in 2002. Analysts believe this is partly because of a failure to invest in infrastructure, and the country’s uncompetitive trade and investment policy, and partly due to globalization.

Rodrik believes the country will never be able to grow at the kind of rapid rate experienced by China or South Korea. “Traditionally, manufacturing required very few skills and employed a lot of people,” he says. “Because of automation, the skills required have increased significantly and many fewer people are employed to run factories. What do you do with these extra workers? They won’t turn into IT entrepreneurs or entertainers; and, if they become restaurant workers, they will be paid much less than in a factory.”

Five factories a year have left the industrial park on the Indonesian island of Batam

The spread of robots makes it much harder for developing countries to get on the “escalator” of economic growth, he argues. That is bad news for the estimated two million young people who enter the workforce every year in Indonesia, a nation of 255 million, where 40 per cent live on $3 a day or less. Mahami Jaya Lumbanraja, a 22-year-old job-seeker on the Indonesian industrial island of Batam, is feeling the effects of the premature de-industrialization phenomenon. For seven months he has been looking for a factory job in Batam, which sits just 20 miles from prosperous Singapore, but he has had no luck. Wearing faded jeans, a grey hoodie and an endearing smile, Lumbanraja says that although he has one year of experience working for Shimano, the Japanese manufacturer of bicycle gears and fishing tackle, he is not experienced enough to secure anything more than an entry-level position, and that there are many more job hunters than openings. “I can survive on the little money I get from busking and helping friends with construction work but I must get a proper factory job to save enough money so I can set up my own small shop later,” he says. Wages in Batam — around $230 per month — are double what Lumbanraja could earn in his home city of Medan, on the island of Sumatra. So he feels he must stay until he finds work.

Lumbanraja is one of about 700 Indonesians in their late teens and early twenties who visit the community centre at the Batamindo industrial park every day looking for work. In February, 3,000 people applied in person for just 80 positions at a Japanese-owned wiring factory there, a gathering so large that executives initially feared it was a labour protest.

Mahami Jaya Lumbanraja is one of 700 Indonesians who visit Batamindo every day looking for work

Batamindo is a joint venture between Singaporean and Indonesian investors that was backed by Presidents Lee Kuan Yew and Suharto — the two nations’ respective rulers — when it opened in 1990. Intended as the showpiece of Indonesia’s industrialization strategy, it has become a symbol of everything that is wrong with it. In recent times, an average of five factories a year have left the industrial park for other countries and the number of people employed there has dropped to just 46,000, from a peak of 80,000 in 2000. That is despite the fact that wages today are between one-third and one-half of the level paid in China’s Guangdong province.

Lembong, a Harvard graduate who ran his own Singapore-based private equity firm before he was appointed trade minister in August, says the government is determined to tackle the twin problems at the heart of Indonesia’s economic malaise: weak infrastructure and over-regulation.

But some argue that reform will come too late. During its period of rapid industrialization, China invested in the modern highways, railways and ports necessary to support its manufacturing sector. In contrast, the physical infrastructure in Batam and much of Indonesia has “not changed much since the 1970s,” says Mook Sooi Wah, general manager of Batamindo.

Indonesia actually had a slightly higher “robot density” than China when the latest figures were collated by the International Federation of Robotics in 2014, although the situation is likely to have changed dramatically since then given the pace of Beijing’s automation push. This anomaly was largely the result of China’s manufacturing workforce being so much bigger than that of Indonesia, which still has no government plan or backing for industrial automation.

Many people don’t realise we’re seeing a quantum leap in robotics

– Tom Lembong, Indonesia’s trade minister

Indonesia’s regulatory process is as fusty as its infrastructure. Recently, legitimate shipments from a paper factory were held by customs at the Batam port because of a rule meant to stop the export of illegally sourced wood. These problems leave even Batam’s boosters exasperated.

Stefan Roll, a German manufacturing veteran who worked in China during its industrial take-off in the 1990s, enjoys living and working in Indonesia. But he worries that the country is missing its “golden opportunity” to become efficient enough to compete on a global scale. “When you are dealing with multinationals, time is money,” Roll says as he shows off his new factory in Batam, which assembles coffee machines for Nestlé. “But you can only do just-in-time manufacturing if you have good roads and infrastructure.”

While few doubt the depth of the challenges facing developing countries, not everyone sees the dilemma in such bleak terms. With wages in countries such as Indonesia and India much lower than in China and their populations still relatively young, some analysts believe they can attract more labour-intensive industries, such as garment-making, widespread automation is not yet suitable.

“As China moves up the industrial chain, it’s actually freeing up a lot of opportunities for Southeast Asia and India,” says Anderson Chow, a robotics industry analyst at the investment bank HSBC, in Hong Kong.

Hal Sirkin, an expert on manufacturing at Boston Consulting Group, says that from the perspective of an economy such as India’s, it does not make sense to automate now because it would drive up the price of goods — “when they have one billion people who can make things cheaply”. He is among the tech optimists who believe that, in the medium term, automation will also create new business niches for emerging economies, mitigating the damage from the jobs that will be eradicated here widespread automation is not yet suitable.

“We think you’re going to see more localization rather than more scale,” says Sirkin. “I can put up a plant, change the software and manufacture all sorts of things, not in the hundreds of millions but runs of five million or 10 million units.”

But Carl Frey, an expert on employment and technology at the University of Oxford, warns that without better education and more skills, developing countries will struggle to take advantage of advancements in manufacturing.

“Technology is becoming increasingly skill-based,” he says. “Many of these countries don’t have a skilled workforce so they’re not very good at adopting these technologies.”

The Shangpin Home Collection factory where the use of robots to cut and drill wooden planks improved productivity by 40 per cent

China itself is not immune from the negative consequences of automation. More than 40 per cent of its 1.4 billion population still live in the countryside, many in poverty, having benefited only marginally from the urban economic miracle.

But the government is betting that the benefits of promoting cutting-edge manufacturing will outweigh the damage from the potential jobs lost. The industrial strategy announced by Beijing last year — known as Made in China 2025 — is designed not only to improve the technological capability of its factories but also to support the development of Chinese brands internationally.

Chow, the HSBC analyst, says that as Chinese companies try to increase their exports to alleviate the impact of the domestic slowdown, they are likely to focus more on the quality of their products: “Quite often part of that development is a better production process, involving robotics.”

Every year, the amount of time it takes for a company’s investment in a robot to pay off — known as the “payback period” — is narrowing sharply, making it more attractive for small Chinese companies and workshops to invest in automation. The payback period for a welding robot in the Chinese automotive industry, for instance, dropped from 5.3 years to 1.7 years between 2010 and 2015, according to calculations by analysts at Citi. By 2017, the payback period is forecast to shrink to just 1.3 years.

Li Gan, general manager of Shangpin Home Collection, Foshan

Automation is not just about putting cheaper and more efficient robot arms on the production line. Li Gan, the general manager of Shangpin Home Collection, which makes and sells customized home furniture, says the greater opportunity is to integrate robots on the factory floor with real-time data from customers and automated logistics systems.

Thanks to the use of robots, the factory that Shangpin opened in Foshan in 2014 was 40 per cent more productive than its previous plant, even though it employs 20 per cent fewer people. Later this year, it will start up the machines at its newest and biggest production base, where it hopes to improve productivity fourfold with just double the number of staff, by using more robots to move supplies around the factory floor and help pack outbound shipping containers.

Drilling wooden slats for the company’s diverse range of beds, wardrobes and other bespoke furniture used to be a painstaking and sometimes dangerous process. Now a worker simply picks up each piece of wood, scans a barcode and puts the wood on a conveyor belt that takes it to the robot arm. The finished product returns on another belt. The process in between is strikingly complicated: Shangpin had to design a device to make sure that each slat would be aligned in the right way for it to be grasped by the robot arm, and the drilling specifications for the slats have to be pre-programmed and recorded in a barcode, because the robots do not yet have any artificial intelligence capability. Li Gan points out that human oversight and decision-making is still crucial. “Automation is just a technical process but what is more important is our thinking about how best to do this,” he says. “Every time we change something, we ask: is it more effective to do this using humans or robots?”

Every time we change something, we ask: is it more effective to do this using humans or robots?

– Li Gan, general manager of Shangpin Home Collection, Foshan

Boston Consulting Group forecasts that the percentage of tasks handled by advanced robots will rise from 8 per cent today to 26 per cent by the end of the decade, driven by China, Germany, Japan, South Korea and the US, which together will account for 80 per cent of robot purchases. Sirkin at BCG says that the rapid expansion of automation could be compared to the difference between the “human learning curve” and Moore’s Law, which posited that computing power could double every 18 months to two years. “Even if you’re very good, humans can only double their productivity at best every 10 years,” he says. In contrast, researchers can push robots to double their productivity every four years, he estimates. “Compounded over time, that makes a big difference.”

As China and other industrial leaders build more and better robots, the tasks they can take on will expand. Butchery, for example, was long considered the sort of skill that machines would struggle to develop, because of the need for careful hand-eye co-ordination and the manipulation of non-uniform slabs of meat. But Sirkin has watched robots cut the fat off meat much more efficiently than humans, thanks to the use of cheaper and more responsive sensors. “It’s becoming economically feasible to use machines to do this because you save another 3 or 4 per cent of the meat — and that’s worth a lot on a production line, where you can move quickly.

“There are things that humans can do better than robots,” he adds. “But they are getting less and less.”

Ben Bland is the FT’s South China correspondent and a former Indonesia correspondent

Photographs by Zeng Han and Muhammad Fadli

May 9, 2016 10:00 pm

Map: Connecting central Asia

Jack Farchy and James Kynge

New Silk Road will transport laptops and frozen chicken

Suppliers looking for ways around Russian restrictions

China’s “One Belt, One Road” project aims to make central Asia more connected to the world, yet even before the initiative was formally announced China had helped to redraw the energy map of the region. It had built an oil pipeline from Kazakhstan, a gas pipeline that allowed Turkmenistan to break its dependence on dealings with Russia and another pipeline that has increased the flow of Russian oil to China.

Chinese companies have funded and built roads, bridges and tunnels across the region. A ribbon of fresh projects, such as the Khorgos “dry port” on the Kazakh-Chinese border and a railway link connecting Kazakhstan with Iran, is helping increase trade across central Asia.

China is not the only investor in central Asian connectivity. Multilateral financial institutions, such as the Asian Development Bank, the European Bank for Reconstruction and Development and the World Bank have long been investing in the region’s infrastructure. The Kazakh government has its own $9bn stimulus plan, directing money from its sovereign wealth fund to infrastructure investment. Other countries, including Turkey, the US, and the EU have also made improving Eurasian connectivity a part of their foreign policy.

1) Moscow-Kazan high-speed railway A China-led consortium last year won a $375m contract to build a 770km high-speed railway line between Moscow and Kazan. Total investment in the project — set to cut journey time between the cities from 12 hours to 3.5 hours — is some $16.7bn.

2) Khorgos-Aktau railway In May last year, Kazakhstan’s President Nursultan Nazarbayev announced a plan to build — with China — a railway from Khorgos on the Chinese border to the Caspian Sea port of Aktau. The scheme dovetails with a $2.7bn Kazakh project to modernize its locomotives and freight and passenger cars and repair 450 miles of rail.

A $46bn economic corridor through disputed territories in Kashmir is causing most concern for India

3) Central Asia-China gas pipeline The 3,666km Central Asia-China gas pipeline predated the new Silk Road but forms the backbone of infrastructure connections between Turkmenistan and China. Chinese-built, it runs from the Turkmenistan/Uzbekistan border to Jingbian in China and cost $7.3bn.

4) Central Asia-China gas pipeline, line D China signed agreements with Uzbekistan, Tajikistan and Kyrgyzstan to build a fourth line of the central Asia-China gas pipeline in September 2013. Line D is expected to raise Turkmenistan’s gas export capacity to China from 55bn cu m per year to 85bn cu m.

5) China-Kyrgyzstan-Uzbekistan railway Kyrgyzstan’s prime minister Temir Sariev said in December that the construction of the delayed Kyrgyz leg of the China-Kyrgyzstan-Uzbekistan railway would start this year. In September, Uzbekistan said it had finished 104km of the 129km Uzbek stretch of the railway.

First freight trains from China arrive in Tehran

Land route takes 14 days compared with 45 by sea

6) Khorgos Gateway

Khorgos Gateway, a dry port on the China-Kazakh border that is seen as a key cargo hub on the new Silk Road, began operations in August. China’s Jiangsu province has agreed to invest more than $600m over five years to build logistics and industrial zones around Khorgos.

China steps up war on banks’ bad debt

Don Weinland in Hong Kong

Beijing has stepped up its battle against bad debt in China’s banking system, with a state-led debt-for-equity scheme surging in value by about $100bn in the past two months alone.

The government-led program, which forces banks to write off bad debt in exchange for equity in ailing companies, soared in value to hit more than $220bn by the end of April, up from about $120bn at the start of March, according to data from Wind Information.

Industry watchers have fiercely debated how far Beijing will go to recapitalize the financial system, with bad loans taking up an ever higher percentage of banks’ balance sheets — as much as 19 per cent by some estimates. The latest figures for the debt-to-equity swap, and a debt-to-bonds swap initiated last year, show a subtle bailout is already under way.

“One can argue the government-led recapitalization is already happening in an atypical way and thus reducing the need for recapitalization in its written sense,” said Liao Qiang, director of financial institutions at S&P Global Ratings in Beijing.

Chinese media reported that up to Rmb4tn ($612bn) had been approved in 2015 for the debt-to-bonds swap, which has seen state-controlled banks trade short-term loans to companies connected to local governments in exchange for bonds with much longer maturities.

That program has been hailed a success in that it relieved the pressure on local governments that were forced to take out bank loans to proceed with public works projects in the absence of municipal bond markets.

The debt-to-equity project has received far less enthusiasm from analysts, who say that coercing banks to become stakeholders in companies that could not pay back loans will further weigh down profits this year. Instead of underpinning stability at banks, Mr Liao says the efforts undermine it.

The programs are just two fronts in Beijing’s battle against bad debt.

The state-controlled asset management companies that bailed out the country’s four national commercial banks 15 years ago have become increasingly active over the past two years in buying up portfolios of bad debt. Regional asset managers run by provincial governments are doing the same business on a local level.

One can argue the government-led recapitalization is already happening in an atypical way and thus reducing the need for recapitalization in its written sense

– Liao Qiang, S&P Global Ratings

The government is also reopening the market for securitizing bad debt with two deals worth Rmb534m due this month. The efforts have even gone online, with debt managers hawking off bad loans on China’s biggest online retail site.

The average rate of non-performing loans at China’s commercial banks hit an official 1.75 per cent at the end of March, according to the banking regulator. That marks the 11th straight quarter that the government-approved figures have risen.

But the official data does not include a much larger stockpile of so-called zombie loans that some analysts say could in future require a more formal bailout for the banks.

Francis Cheung, analyst at CLSA, estimates that bad debt accounted for 15-19 per cent of banks’ loan books at the end of last year and that the government may have to add Rmb10.6tn of new capital to the banking system, or 15.6 per cent of gross domestic product.

David Mann, Standard Chartered’s chief Asia economist, has noted that the problem has been exacerbated by “shadow financing”, an all-encompassing term for banks’ off balance-sheet lending that skirts regulations. However, Mr. Mann argued in a recent report that the many program China has deployed to fight bad debt would reduce the need for a direct bailout of the system.

Shadow lending hit about Rmb40tn at the end of last year, or about 59 per cent of GDP, according to CLSA. While much of that is not distressed, its opacity makes it difficult to assess its risk or to regulate it.

US: Anti-dumping duty on Chinese wooden bedroom furniture

May 20, 2016

Source:

ITTO/Fordaq

The U.S. Department of Commerce has made a final determination of the antidumping duty to be applied to Chinese wooden bedroom furniture imports.

The US will introduce a general duty of over 200% on Chinese wooden bedroom furniture from a number of named companies.

On 14 December 2015, the United States conducted its 10th preliminary anti-dumping review on Chinese wooden bedroom furniture imports.

The latest administrative review involves 18 Chinese manufacturers. The HS code of the products involved is HS 9403.50.9042, 9403.50.9045, 9403.50.9080, 9403.50.9041, 9403.60.8081, 9403.20.0018, 9403.90.8041, 7009.92.1000 and 7009.92.5000.

South Korea’s deepening economic slowdown deals fresh blow to Park

Weak data will disappoint president and add to pressure for rate cut

Fishermen unload anchovies at Mijo in South Korea, where weak exports helped push down first-quarter GDP © Bloomberg

Bottom of Form

April 25, 2016

by: Song Jung-a in Seoul

South Korea’s economic slowdown deepened in the first quarter, with sluggish exports and domestic consumption weighing on growth and adding to pressure on the Bank of Korea to cut interest rates.

The data mark another blow for the administration of Park Geun-hye, which is already reeling from a shock loss of its parliamentary majority this month that has clouded the prospects for its economic reform drive.

Gross domestic product expanded 0.4 per cent quarter-on-quarter in the first three months of the year, after growth of 1.2 per cent and 0.7 per cent in the third and fourth quarters of last year. The annual growth rate was 2.7 per cent.

The weak performance, broadly in line with expectations, came as Asia’s fourth-largest economy suffers a fall in exports amid waning global demand. Exports fell 1.7 per cent in the first quarter, hit by China’s slowing economy.

Weak domestic spending was also a factor, despite a boost in fiscal spending and the reintroduction of consumption tax breaks on cars. Capital investment dropped 5.9 per cent from the previous quarter as global uncertainties deterred Korean companies from investing in new facilities. Consumption fell 0.3 per cent, held back by high household debt.

“The sliding exports are having a negative impact on domestic consumption and corporate investment,” said Ju Won, an analyst at Hyundai Research Institute. “Stimulus measures both on the monetary and fiscal fronts are urgently needed to pull the economy out of the current slump.”

While Lee Ju-yeol, BoK governor, last week expressed optimism over the economy, calls for monetary easing are growing following the ruling party’s defeat in parliamentary elections this month.

“A more fractious parliament is only likely to add to consumer and business uncertainties, further undermining growth prospects,” BNP Paribas said in a recent report.

Last week the BoK left interest rates unchanged at a record low of 1.5 per cent for a 10th straight month, amid concerns about high household debt. But economists expect the bank to cut interest rates at least once this year after it lowered this year’s growth forecast to 2.8 per cent from 3.0 per cent. The economy grew 2.6 per cent last year.

The government is also under pressure to increase public spending. It has allocated more than 40 per cent of this year’s budget to the first quarter but finance minister Yoo Il-ho said the government had no immediate plan for a supplementary budget to stimulate the economy.

However, Kwon Young-sun at Nomura expects a stimulus package including a supplementary budget to be announced as early as June after the new national assembly opens on May 30.

“The election [result] means that President Park’s labour market reforms should lose momentum,” he said. “As a result, the government will probably depend more on macro stimulus to support job markets, rather than politically controversial structural reform, ahead of the 2017 presidential election.”

India’s GDP data

The elephant in the stats

Few economists wholeheartedly believe India’s stellar growth rate

Apr 9th 2016 | From the print edition

GOVERNMENT statisticians shun the limelight, which only ever finds them when things go awry. So it is with India’s national bean counters, who are struggling to convince the world that an economy with idle factories, sagging exports and ailing banks grew by 7.5% in 2015, as their models purport to show. Ever since a new methodology for calculating GDP was adopted last year, India has appeared to be the world’s fastest-growing big economy, outpacing China. But skepticism about the data is growing even faster.

Growth figures are calculated by first arriving at the value of economic output over a given period and then comparing it with the prior period. The difference between the two gives a nominal rate of growth (i.e., without any adjustment for inflation). Most observers agree that India’s egg-heads perform these tasks well. The problem seems to be the “GDP deflator”, a gauge of inflation by which the data are adjusted to derive the “real” growth rate. The higher inflation is assumed to be, the bigger the slice of nominal growth that is attributed to price rises rather than genuine increases in output.

Mercifully enough, GDP deflators do not normally attract much attention. Typically, different bits of the economy are deflated by whichever inflation series is most apposite. India compiles two measures: a wholesale price index (WPI), measured at the factory gate, and a consumer price index (CPI), which tracks how much consumers pay. Changes in the two usually move in tandem, so it doesn’t much matter which is used.

All that has changed since prices of oil and other commodities tumbled last year, causing wholesale prices to decline. Despite this, deflation remains a distant dream for shoppers: the price of consumer staples is still rising by over 5% a year. The gap between the changes in the two indices swelled from nothing to nine percentage points in September, before falling back to six percentage points. The statisticians use WPI to deflate the nominal growth of service output, which accounts for roughly half the economy, even though most services have not benefited much from low commodity prices. The blended inflation figure used to deflate the nominal data may therefore be too low, making real GDP growth come out too high (see chart).

Investors, at any rate, roundly disbelieve India’s growth figures. Nevsky Capital, a hedge fund, cited dodgy data from India, among other places, as a reason to shut up shop at the start of the year. Even the government’s own chief economic adviser has admitted he is sometimes flummoxed by the data. A cottage industry has sprung up to cater to the sceptics, blending various indicators of economic activity to produce new gauges of growth.

Such home-brewed statistics have been common in China for some time: Li Keqiang, now the country’s premier, admitted as a provincial governor that he all but ignored “man-made” economic statistics in favor of hard-to-fiddle data such as railway-cargo volumes, electricity consumption and loans made by banks. The Economist began publishing a “Keqiang Index” when his habits became known in 2010.

Ambit Capital, a broker based in Mumbai, now computes its own “Keqiang Index” for India, which implies a real growth rate of 5.4%. Economists at HSBC, a bank, think 5.9-6% is closer to the truth.

If the divergence between WPI and CPI is indeed distorting the data, its nefarious impact should soon disappear as year-on-year readings of commodity prices stabilize and so reunite the two series. Statistical improvements are also promised by India’s boffins. But measuring fast-evolving economies is tricky: Nigeria two years ago announced its GDP was almost twice as big as official statistics had previously indicated. It does not help that 90% of India’s workers toil in the informal sector.

“The debate will reduce but not go away,” predicts Pronab Sen of the National Statistical Commission, an advisory body. Though they have flaws, India’s official statistics are pretty good by emerging-market standards, he argues. But in a global economy with few bright spots, where only America and China are adding a bigger amount to global GDP, it would be comforting to be more certain.

South-East Asian economies

Okay, for now

The region is looking perkier than most, but its growth potential is waning

Apr 16th 2016 | SINGAPORE | From the print edition

WHEN you consider the backdrop of weak global demand, a faltering Chinese economy and uncertainty over American monetary policy, then the predictions for South-East Asian economies appear quite upbeat. Of the ten countries in the region, only tiny Brunei is close to recession. Indeed the Asian Development Bank (ADB) forecasts that growth in regional GDP will climb from 4.4% last year to 4.5% this year and 4.8% in 2017. But hold that backdrop in mind: such forecasts may prove too optimistic, especially if global financial markets get another bout of jitters like those earlier this year, and foreign capital is pulled out in a hurry.

The region’s healthiest economies are those of Vietnam and the Philippines: both have young populations and rely less than most in South-East Asia on either China or exports of commodities, whose prices are currently depressed. Growth in Vietnam was 6.7% last year, driven by competitively priced exports. It was only a tad less in the Philippines, thanks to strong services, particularly call centres. Fresh investment in infrastructure in both countries is also driving growth. But the going will not be so easy in the future. Vietnamese manufacturing would be hurt by weaker global trade; meanwhile the government has many galumphing state-owned enterprises to wrestle with. And Philippine call centres face competition from automation software.

A slowdown in China, with its reduced demand for commodities, is hitting Indonesia and Malaysia particularly hard. Commodities (including coal, palm oil and nickel ore) account for three-fifths of Indonesian exports. But tax collection is too weak for the government to do much to soften any slowing of growth. Hoping to spur further investment, the government said this week that it would cut corporate tax from 25% to 20%. But it will probably be years before this stimulates enough investment to translate into more tax receipts. President Joko Widodo entered office in 2014 promising to return the country to 7% growth; today that looks somewhere between fanciful and impossible, despite ambitious plans to ramp up spending on much-needed infrastructure.

Malaysia, Asia’s biggest oil exporter, suffers not just from low commodity prices but from its prime minister’s increasingly surreal hold on power, a combination that has put downward pressure on the currency, the ringgit. Najib Razak has spent months giving unsatisfactory answers to questions about how hundreds of millions of dollars passed through his personal bank accounts. He has cracked down on political opponents and engaged in racial politics—while the price of oil, which makes up a fifth of Malaysian exports, has fallen by over 60% from its peak two years ago. Strong exports of electronics give Malaysia a cushion that other oil producers lack. Yet that sector is more exposed than many to global demand. Malaysia’s annual GDP growth is forecast to average below 5% to the end of 2018. But that assumes questions over Mr. Najib do not paralyze government or spill onto the streets.

Poor governance also afflicts Thailand. Last year it grew at a sluggish 2.8%, following dismal growth of under 1% in 2014, after General Prayuth Chan-ocha led a coup and then installed himself as prime minister. Domestic demand has since recovered, and tourists are coming back to the beaches. But uncertainty about the country’s political direction is surely a dampener on foreign and domestic investment. Should infrastructure projects, some backed by China, proceed as planned, and political calm prevail, then growth may pick up. Yet Mr. Prayuth’s team has yet to evince a flair for economic management.

Beyond these economies’ immediate prospects, however, longer-term issues are more important, as the ADB’s latest outlook highlights. Among the most serious are shrinking workforces and declining birth rates, especially for Thailand and rich Singapore. Another is lower productivity growth in the future. Easy gains were made when tens of millions of poor South-East Asians moved from the countryside to work in new factories or burgeoning service sectors. But the next leap will be much harder, and will depend on more young people getting a college education, more flexible labor markets, constant upgrading of technologies and smarter, more responsive governments.

It is all a tall order. In fact, the ADB concludes that South-East Asia, along with most of the rest of Asia, has seen its potential growth flag by over two percentage points since 2006-10: the sizzling rates of a decade ago will not return without that next leap.

Global biomass pellet market expected to rise sharply by 2020

April 14, 2016

Source:

P&S/Fordaq

The global biomass pellet market was valued at $6.9 billion (€6.17bn) in 2014 and it is expected to grow with a CAGR (Compound annual growth rate) of 11.1% during the 2015-2020 period, a study published by P&S Market Research says.

The increased level of investments in the biomass industry has propelled the technological advancement, and there has been a recent upsurge worldwide in co-firing of biomass with coal, since it is a carbon neutral fuel, which helps to reduce emissions from thermal power plants.

The increased demand for the adoption of biomass-based power generation, along with traditional methods of power generation using fossil fuels is responsible for fuelling the growth of the global biomass pellets market.

Europe accounted for the largest share of the global biomass pellet market with 18.14 billion tonnes consumed in 2014.

The major reasons behind growth of the market in the region were low greenhouse gas emission from biomass and increased government initiatives for renewable technologies.

The market in Europe is expected to maintain its growth rate, mainly driven by various subsidies and legislation.

The power sector application segment is expected to witness the fastest growth (12.4% CAGR) during 2015-2020 in the global market.

Based on application, the heat sector segment held the largest market size, with approximately 14.5 billion tonnes volume in 2014, and it is expected to reach 27.5 million tonnes by 2020, growing with a CAGR of 8.7% during the period 2015-2020.

In 2014, North America accounted for the second largest share in the global biomass pellet market, in terms of value and volume.

The major reasons behind growth of the market in the region were increasing demand of biomass pellets in industrial sector, strict environmental regulations, and increasing concern for global warming.

Therefore, the high rate of depletion of fossil fuels and increasing demand for the reduction of greenhouse gases are indirectly creating ample opportunities for the growth of the North American market.

April 28, 2016 7:59 pm

India’s central bank considers peer-to-peer lending rules

Simon Mundy in Mumbai

India’s central bank has unveiled an outline for proposed regulation of peer-to-peer lending, a move that leaders in the nascent industry said could accelerate its adoption, helping to meet gaps in the market left by struggling state-owned banks.

The peer-to-peer model — under which borrowers and lenders deal directly with each other through an online platform — has grown rapidly in countries such as the US and the UK, which have introduced regulation for the sector. Cumulative global lending amounted to over $6bn by the end of last year, 10 times the figure at the end of 2012, according to the UK’s Peer-to-Peer Finance Association.

But the model remains unregulated in India and retains a marginal role in financial activity: the biggest platforms in the market were founded only within the past two years, and the vast majority of loans are no larger than a few thousand dollars.

In a consultation document published on Wednesday, the Reserve Bank of India said that it was necessary to regulate an industry that “has the potential to disrupt the financial sector and throw surprises”.

It noted that regulation could be taken as a stamp of approval for the model, potentially attracting investors who do not understand the risks. But it decided against following Israel and Japan in banning it, noting that peer to peer could extend services “where formal finance is unable to reach”, while reducing market lending rates through increased competition and lower costs.

Three quarters of banking assets in India are held by state-owned banks, which are struggling to cope with a wave of non-performing loans to companies in sectors including infrastructure and steel. The RBI has put pressure on the banks to write down such assets — a move that is broadly seen in the financial sector as necessary, but which has still sparked concerns about a negative impact on credit supply.

Bhuvan Rustagi, co-founder of the Indian peer-to-peer platform Lendbox, said regulation would “increase confidence among investors, borrowers and the [venture capital] community”. But he raised concern about the RBI’s proposed requirement that all platforms should be companies with at least Rs20m ($300,000) in capital, arguing that this is unnecessary because the companies do not lend from their own balance sheets, and that most are small start-ups that could not raise so much money.

BlackRock backs P2P with £12.7m investment

Simon Mundy in Mumbai

Funding Circle stake lends credibility to fledgling sector

Mr. Rustagi said he believed that the Rs35m lent to date on Lendbox, since its launch in November, made it the country’s second biggest peer-to-peer platform by this measure.